Alphabet: Alpha-Bet?

The God of information in the internet age.

What Is Alphabet?

Created in 2015, Alphabet is a collection of companies; essentially a holding company for Google—The God of information in the internet age. The company offers a variety of software and Internet-related services and solutions, including web browsing and searching, cloud computing, streaming entertainment, mobile operating systems and applications, and more. Google has always invested in many far-reaching areas of technology — such as internet search, mobile phones, artificial intelligence, self-driving cars, and health technology. Although the various “moon shots”, like driverless cars, Google Glass, the health initiative Verily, and drones that emerged from the “X” division are engrossing, the company does one thing incredibly well: sell advertising. And the vast majority of that advertising is sold in connection with the core Google search capability. Throw in not just the moon shots, but also purchases made through the Google Play app store, various hardware devices like Nest home products and Pixelbooks and phones, YouTube subscription products, and even Google Cloud, and roughly 80 percent of Google’s over $250 billion in revenues still persistently comes from advertising.

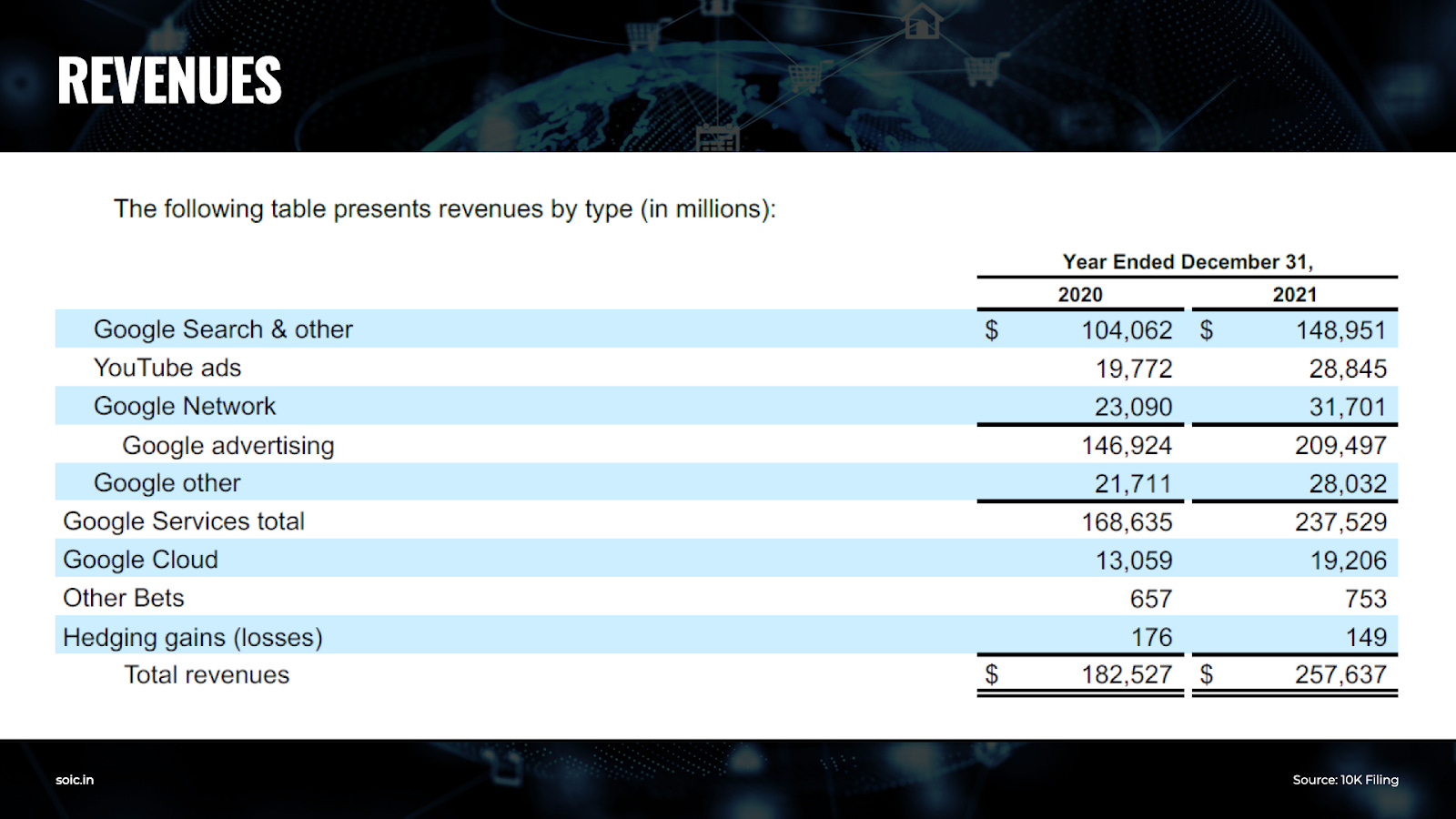

As of 2021, Alphabet generated over $257 billion in revenues, for the first time in its history. Over $209 billion (over 81% of the total revenues) came from Google Advertising products (Google Search, YouTube Ads, and Network Members sites). They were followed by over $28 billion in other revenues (comprising Google Play, Pixel phones, and YouTube Premium), and by Google Cloud, which generated over $19 billion in 2021.

For some context, in 2004 Google generated almost a billion dollars in revenues, and it was worth about $23 billion as it IPOed. In 2021, Alphabet become a two trillion-dollar company. Back in the early 2000s, the company had started to build its advertising machine. This journey culminated in 2004 when the company had managed to put together the various pieces (Google AdWords and Google AdSense) of its advertising machine, thus scaling up its revenues on top of a growing search platform. At the time the advertising machine was primarily based on Internet traffic from desktop devices. Today most traffic comes from mobile.

Take One Idea, And Take It Seriously

The Internet is one of the world’s most powerful equalizers; it propels ideas, people, and businesses large and small.

Sergey and I (Larry) founded Google because we believed we could provide an important service to the world-instantly delivering relevant information on virtually any topic. Serving our end users is at the heart of what we do and remains our number one priority.

Our goal is to develop services that significantly improve the lives of as many people as possible. In pursuing this goal, we may do things that we believe have a positive impact on the world, even if the near-term financial returns are not obvious. For example, we make our services as widely available as we can by supporting over 90 languages and by providing most services for free. Advertising is our principal source of revenue, and the ads we provide are relevant and useful rather than intrusive and annoying. We strive to provide users with great commercial information.

Google started life as a pure aggregator—its corporate mission “to organize the world’s information and make it universally accessible and useful” makes that clear. Google has undertaken one of the most ambitious strategies in business history: to organize all the world’s information. In particular, to capture and control every cache of productive information that currently existed on, or could be ported to, the web. And with absolute single-mindedness, the company has done just that. It began with the stuff already on the web—it couldn’t own that, but it could become the gatekeeper to it. After that, it went after every location (Google Maps), astronomical information (Google Sky), and geography (Google Earth and Google Ocean). Then it set out to capture the contents of every out-of-print book (the Google Library Project) and work of journalism (Google News).

The Last Will Be First

It doesn’t matter if you are the first one in the arena, what matters is that you are the last one standing. Before the invention of Archie, a simple yet effective web-based search engine, by Alan Emtage in 1990, finding anything online was less than pleasant. This was a turning point for internet users as it was closely followed by the launch of many other bigger and better search engines, including Excite, Yahoo, Infoseek, AltaVista, Ask Jeeves, and of course the now ever-popular Google. Google is the most powerful search engine in the world. However, it was not the first. Quite the opposite, it was a latecomer, in a search industry already dominated by several players. However, thanks to a powerful algorithm, called PageRank it soon took off. The reason search engines had never worked very well before PageRank was not that they were broken, but because they were missing the key innovation that Brin and Page had stumbled upon— relevancy. Not only did Google’s search engine continue to be superior to any rival in existence, it slowly but surely widened the gap between its version of search and the competition.

You are the best search engine out there, but how was the search engine supposed to make money?

Back in 1999, it was already clear that Google was the best search engine out there. It wasn’t clear though how it was supposed to make money. In mid-1999 Larry and Sergey met Bill Gross, founder of GoTo.com search engine.

Gross had an idea. Rather than rely on the old advertising model based on cost-per-mille, advertisers would get paid on the number of impressions of an ad. Gross thought of a new model, based on cost-per-click. A company would pay for an advertisement only if a user found it so relevant to click.

At the time, Larry and Sergey were still reluctant about using ads to monetize Google. Yet the company was burning cash, and by the year 2000 investors were getting nervous. When Larry and Sergey were approached again by Gross, which proposed to merge the two companies, Google’s founders declined.

Why? Because they didn’t want their search to be associated with a company that mixed paid advertising with organic results.

“We expect that advertising-funded search engines will be inherently biased towards the advertisers and away from the needs of the consumers.”

Today, Google generates over 80% from advertising, of which cost-per-click is the primary driver.

Google doesn’t monetize the user directly. Google makes money by leveraging users’ data, combined with its algorithms, sold to advertisers for visibility; Google’s users don’t pay for the search engine. Instead, the revenue streams come from advertising money spent by businesses bidding on keywords—This ad network is called AdWords. Whenever a user searches for anything using Google's search engine, an algorithm generates a list of search results. The algorithm attempts to provide the most relevant search result for the query as well as related suggested pages from a Google Ads advertiser. Google generates fees from advertisers when users engage with the ad in some way, such as by clicking on it or by simply seeing the ad. Advertisers also pay Google to have their pages suggested to users and will attempt to outbid each other for the top spot on the search result list. Usually, the more competitive and more expensive an industry is, the more expensive the bid is going to be.

Turning The Web Into A Giant Google Billboard!

Google engineers dreamed up ways to syndicate text ads not just to major search sites and portals, but to the entire web itself. “The idea of putting ads on non-search pages has been floating around here for a long time,” said Google executive Susan Wojcicki. Google already had the entire web in its index, so if it could find a way to match relevant ads to the content on other people’s web pages (just as it had matched relevant ads to search queries), Google could, in Wojcicki’s words, “change the economics of the web. You do the content and leave the selling of the ads to Google.”

In 2003, Google’s employee Paul Bouchet developed a feature that allowed the matching of words sent through Gmail with keywords bidden by advertisers. That generated ads profits with the cost-per-click model. Sergey Brin thought, why not apply this model to websites. That is how they kicked off AdSense. In short, Google for the first time allowed small businesses and blogs to generate ads revenue on their own. In return, Google got one-third of the revenue generated. Any “Web property” was a good candidate to become a Google partner and generate profits for their content independently of advertising middlemen.

Google, developer of the award-winning Google search engine, today announced a new self-service option for Google AdSense, a program that enables website publishers to serve ads precisely targeted to the specific content of their individual web pages. With Google AdSense, publishers serve text-based Google AdWords ads on their site and Google pays them for clicks on these ads – users benefit from more relevant ads and publishers can maximize the revenue potential of their websites. The self-service option augments the existing content targeting services for publishers announced by Google in March 2003, now making this service available to a broader universe of high-quality websites.

There was a whole new world of content being created on the web, and the creators were the web users themselves.

“Google AdSense improves the overall web user experience by bringing relevant, unobtrusive, text ads to web pages rather than disruptive, unrelated ads such as pop-ups and animations… By providing website publishers with an effective way to monetize content pages on their sites, Google AdSense strengthens the long-term business viability of content creation on the web.”

— Sergey Brin

You might think that since Google is the best search engine out there, that is why it makes over 80% of its revenue from advertising. However, for how marvelous the Google search algorithm is, what makes Google the tech giant that it is today; is its asymmetric business model—In an asymmetric business model, the organization doesn’t monetize the user directly, but it leverages the data users provide coupled with technology, thus have a key customer pay to sustain the core asset.

Win-Win-Win

In a complex world with increasing interdependence, the best outcome for all players is to make decisions that create positive Non-Zero Sum scenarios. A Non-Zero Sum interaction leaves all parties better off than if they had not transacted in the first place (i.e., a win-win scenario rather than a win-lose or lose-lose scenario). Google creates value for all participants, including itself, and thus creates large amounts of Non-Zero Sumness.

AdWords and AdSense together create a win-win-win. Companies can sponsor their products for much cheaper, and track their results with no effort. Online publishers can easily monetize – something is better than nothing – their content. Users get relevant answers to any question they might have.

Google offers advertisers a set of tools that help them better attribute and measure their advertising campaigns across screens. It does so by running two main kinds of ads:

Performance Advertising: Google creates and delivers relevant ads that users will click on, leading to direct engagement with advertisers. The performance advertisers pay when a user engages in their ads. AdWords is the primary auction-based advertising program that helps create simple text-based ads that appear on Google properties and the properties of Google Network Members. Also, Google Network Members use the AdSense program to display relevant ads on their web properties, generating revenues when site visitors view or click on the ads.

Brand Advertising: Google helps enhance users’ awareness and affinity with advertisers’ products and services, through videos, text, images, and other interactive ads that run across various devices. Google focuses on creating what they define as “the best advertising experiences” for its users and advertisers in many ways. Google clarifies its efforts as “ ranging from filtering out invalid traffic, removing hundreds of millions of bad ads from the systems every year to closely monitoring the sites, apps, and videos where ads appear and blacklisting them when necessary to ensure that ads do not fund bad content.” This is critical to Google’s success. One of the most compelling reasons for Google to take off the search industry was based on its ability to rank organically content that was qualitatively 10x higher compared to its rivals. Also, even though Google AdWords allows advertisers to bid on keywords, it selected those text-based ads based on the quality, as those text-based ads with more clicks got the highest spot on the search results pages.

How does Google measure its advertising network performance?

When assessing the advertising revenues performance, there are a few critical metrics Google looks at:

The percentage change in the number of paid clicks. Paid clicks represent engagement by users and include clicks on advertisements by end-users on Google search properties and other Google-owned and operated properties including Gmail, Google Maps, and Google Play.

And cost-per-click (defined as the average amount Google charges advertisers for each engagement by users ) for Google properties (AdWords) and Google Network Members’ properties (AdSense)

The percentage change in impressions. This includes impressions displayed to users on Google Network properties participating primarily in AdMob, AdSense, and Google Ad Manager.

And cost-per-impression is defined as impression-based and click-based revenues divided by our total number of impressions and represents the average amount we charge advertisers for each impression displayed to users.

An increase in paid clicks/impressions is a good sign of Google's ability to attract advertisers to its platform. However, it needs to be assessed against Google's cost-per-click/impression change. More advertisers might spend less per click/impression, thus making the average revenues for Google decrease.

In 2020, the pay per click/impressions increased compared to 2019. However, it was offset by a decrease in cost-per-click/impression. Google doesn’t show absolute numbers as this is kept secret.

In 2021, the pay per click increased by 23% compared to 2020; the cost per click increased by 15%. Change in impression increased by 2%, and cost-per-impression increased by 35%.

Google recorded an increase in paid clicks driven by an increase in user adoption and search queries primarily on mobile devices. This also drove more paid clicks in AdMob through the Google Play store. Google is testing various ad formats (we can argue it’s showing more ads) both on Google’s products and YouTube, which slightly improved monetization.

Google’s advertising revenue growth, as well as the change in paid clicks and cost-per-click on Google Search & other properties and the change in impressions and cost-per-impression on Google Network properties and the correlation between these items, can be affected by various factors. Some of those factors are:

advertiser competition for keywords;

changes in advertising quality or formats;

changes in device mix;

changes in foreign currency exchange rates;

fees advertisers are willing to pay based on how they manage their advertising costs;

general economic conditions;

growth rates of revenues from Google properties, including YouTube, compared to growth rates of revenues from Google Network Members’ properties;

seasonality;

a shift in the proportion of non-click based revenues generated on Google properties and Google Network Members’ properties, including an increase in programmatic and reservation-based advertising buying; and

traffic growth in emerging markets compared to more mature markets and across various advertising verticals and channels.

Google “Search & other” generated over $148B in revenues in 2021 on a base of over $104B in 2020. This represents the set of products that Google owns, from the search engines (including revenues from traffic generated by search distribution partners who use Google.com as their default search in browsers, toolbars, etc.) to all the other vertical platforms that the company operates (Google Discover, Google News, Google Travel, Gmail, Google Maps, and more). Google’s search advertising has been driven by growth in search queries. Since the pandemic hit, more and more users started to use Google’s products. This trend has continued. However, most of it was driven by mobile users’ growth. This is an important aspect, as it shows that Google’s main driver of growth is based on mobile traffic. This changes the way the company needs to prioritize its product developments efforts, its ad formats served to users, and also how it experiments.

Google Network Members’ properties— Here Google shows advertising on the network members’ properties, thus splitting the revenues with them. This is the set of publishers that decide to opt into Google’s advertising network (either AdSense for desktop, or AdMob for in-app advertising). In 2021, Google’s network members generated over $31 billion of revenue on a base of over $23B in 2020. Google’s network members’ properties growth was primarily driven by AdMob. In short, the mobile advertising platform, powered up by Android devices through the Google Play store, was the main driver of revenue growth in 2021. This shows how Google has also shifted its focus on the mobile advertising platform.

YouTube Ads

On October 9, 2006, Google announced that it was purchasing YouTube for $1.65 billion in stock. This is of course one of the most successful business acquisitions ever done. Google’s decision to take on YouTube’s burden seemed downright crazy to a lot of people. At the time YouTube was getting sued for various copyright infringements (the platform is comprised of user-generated content, often posting copyrighted materials). Wasn’t Google paying a lot of money to assume a huge liability risk? It turned out that Google made one simple calculation when it purchased YouTube: in the broadband era, the video was likely to become as ubiquitous on the web as text and pictures had always been. YouTube was already, in essence, the world’s largest search engine for video. With its stated mission to organize all the world’s information, Google simply couldn’t let video search fall outside its purview.

Google saw YouTube as an opportunity to diversify its products away from traditional Search while creating a near-monopoly for the growing medium of online video content.

Since then, YouTube has become a primary contributor to the company’s advertising revenue and a successful testing ground for new advertising strategies. It’s just amazing to see how Google has integrated YouTube and scaled it up. By 2021, YouTube has become an advertising machine generating over $28 billion at the base of over $19B in 2020 (this doesn’t count the YouTube memberships, which are reported separately).

“YouTube is one of those products which, you know, is scaling really well globally, just like Search did, and … we are seeing real strong growth on mobile and we’re seeing real strong growth for YouTube on emerging markets as well. And we are seeing real strong growth on television.

So if I look at YouTube on mobile, on emerging markets, on larger screens, they all look like newer opportunities … I think there’s a lot more growth ahead.”

— Sundar Pichai

YouTube growth was driven primarily by improved ad formats. This means that Alphabet (as it’s evident to anyone going on YouTube) has ramped up the advertising operations on YouTube. In short, on YouTube now there are way more ads than before. This “improved ad formats” is the result of YouTube’s extreme stickiness with users, which enables Alphabet to play with its ad formats.

YouTube is also taking on over-the-air TV. It already offers free movies with ads. Now, viewers will be able to stream nearly 4,000 episodes of TV for free, as long as they're also willing to watch ads during the show. Shows available include Hell’s Kitchen, Andromeda, and Heartland, and viewers will be able to watch them in the US on the web, mobile devices, and “most connected TVs via the YouTube TV app”.

It’s Not Just Advertising

Google's other revenues consist primarily of revenues from:

Google Play, which includes sales of apps and in-app purchases and digital content sold in the Google Play store. The model is based on revenues shared with developers or publishers, usually based on an 85/15 split, where the developer keeps 85% of the revenues, while Google retains the 15%.

Devices and Services include sales of hardware, including Fitbit wearable devices, Google Nest home products, and Pixel phones.

YouTube non-advertising, which includes YouTube Premium and YouTube TV subscriptions, and

other products and services

Google's other revenues generated over $28B in 2021 on a base of over $21B in 2020.

All in all—Google Services which includes Google Search & other, Google Network, Youtube Ads, Google's other revenues generates over $237B (93%) of Google’s total revenue of over $257B as of 2021.

Google Cloud

The cloud business unit is extremely important for Google as the whole company was built in the cloud. They see significant opportunity in helping businesses with features like data migration, modern development environments, and machine learning tools to provide enterprise-ready cloud services, including Google Cloud Platform and Google Workspace. Google Cloud Platform enables developers to build, test, and deploy applications on its highly scalable and reliable infrastructure. Google Workspace collaboration tools — which include apps like Gmail, Docs, Drive, Calendar, Meet, and more — are designed with real-time collaboration and machine intelligence to help people work smarter. Because more and more of today’s digital experiences are being built in the cloud, Google Cloud products help businesses of all sizes take advantage of the latest technological advances to operate more efficiently.

Google Cloud revenues consist primarily of revenues from the Google Cloud Platform comprising G Suite productivity tools and other enterprise cloud services provided on either a consumption or subscription basis.

After a dozen years in the market and several shifts in strategy, Google remains a distant third in the cloud infrastructure market, behind AWS and Microsoft Azure. Google is up against a competitor in AWS with 15 years in the cloud and Microsoft with 30 years in the enterprise.

Enterprise IT markets generally follow one of two paths. Either they come to be dominated by a single large player — as is the case in database management, networking, and desktop software — or they fragment among many smaller players that each stake out their niches, as is the case in personal computers and security. The cloud infrastructure market started along the former path, but its more likely trajectory is toward the latter.

Five years from now, the cloud infrastructure market won’t be the same. It’s going to be less important who’s got the infrastructure market share and more important who’s got the application market share.

Enterprises are increasingly choosing cloud providers based on factors other than infrastructure alone. Microsoft derives a lot of cloud infrastructure business from customers of its Microsoft 365 and Dynamics applications. AWS’ sheer weight and success in the government sector is a powerful barrier to competition.

Google Cloud’s ability to leverage the broader assets of Google and Alphabet—from the big data prowess of its search, marketing, and advertising reach to healthcare and life sciences insight—is among its top-selling points over competitors. Google sees several opportunities to leverage its expertise across other verticals (like content and digital commerce) to get its foot in the door with enterprises facing a growing need for cloud services.

Google Cloud $22B (>7% of total revenue) run rate, growing at 44%; AWS $71B run rate, growing at 40%; Azure $45B run rate growing 46%. The cloud market is massive and growing! With cloud adoption still in its relative infancy, the market is wide open for Google Cloud, even as it trails the two public cloud frontrunners.

From 2020 to 2021, there is over 80% growth in total deal volume for Google Cloud Platform, and over 65% growth in the number of deals over a billion dollars. The number of customers spending more than $1 million through the marketplace increased by 6X.

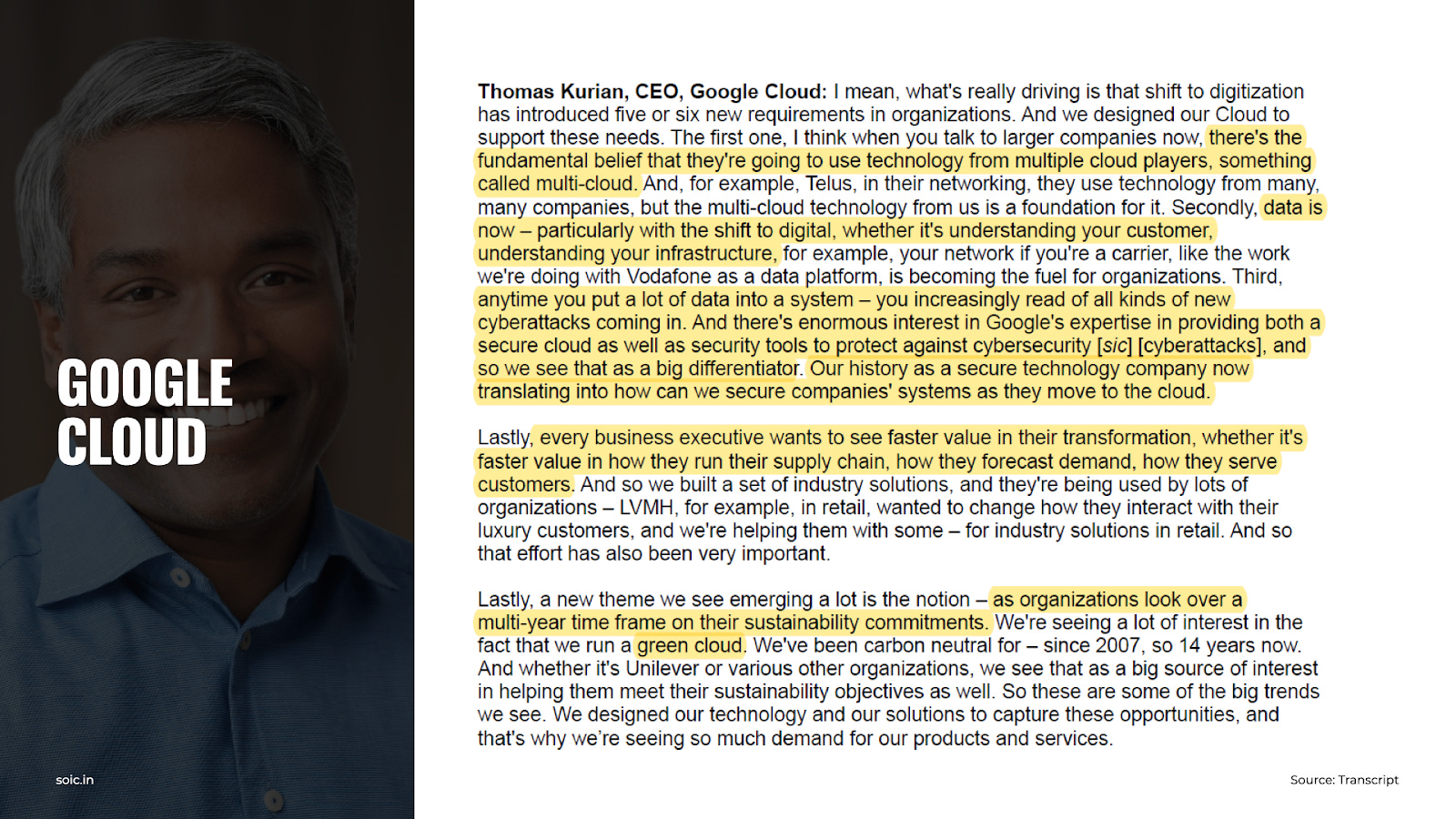

“We don’t spend our day waking up in the morning worrying about who’s first, second or third—partly because it’s important that we focus on the customer, not on competition, and, much more importantly, because it’s also apples to oranges what people are counting in their cloud revenue numbers. So we don’t lose a lot of sleep over keeping score.”

— Thomas Kurian

Thomas Kurian joined Google in November 2018 as the CEO of Google Cloud. Before Google, Thomas spent 22 years at Oracle Corporation, where most recently he was President of Product Development. Kurian has upped Google’s cloud game with hot new technology, a razor-sharp vertical market focus, and big partner investments.

“Our strategy for cloud is quite simple,” In every industry, we see customers wanting to adopt digital technology either to lower cost, grow their top-line revenues or change ... how they bring products in certain markets, and we at Google are using our cloud platform as a vehicle to deliver digital solutions to them.”

— Thomas Kurian

Kurian sees three primary Google Cloud capabilities: allowing customers to use its large-scale infrastructure to modernize their IT abilities; allowing customers to leverage Google Cloud’s data, analytics, machine learning, and application development solutions to understand and use information in new ways; and providing industry-specific solutions in the six target markets of financial services, health care, manufacturing and industrial, the public sector, retail, and media, telecommunications and entertainment.

When asked about the company’s approach to heavily regulated industries, Sundar Pichai said:

“That’s where a lot of our investments have gone, getting certifications needed, depending on the industry and building the features that you need… And that’s clearly starting to have an impact, both on GCP, but as well as G Suite. We definitely are going to continue to build out our capabilities. And we’ll be going after the opportunities in these areas very seriously.”

Cybersecurity, which is critical for the cloud business, has become another area of focus for Google and other tech giants.

One of Alphabet’s first major outings into commercial cybersecurity was Chronicle, a company that emerged from Alphabet’s X Development (formerly known as Google X) R&D division in 2018. Chronicle’s first commercial product offering was Backstory, a system designed to identify potential security risks to enterprise companies in real-time by analyzing security telemetry data with AI and machine learning algorithms. Chronicle and Backstory were incorporated into the core Google Cloud service in June 2019.

Ultimately, the spin-off is intended to create what Google X chief Astro Teller calls a “digital immune system.”

Unlike some cybersecurity products, which charge clients based on the volume of data analyzed, Backstory’s pricing was determined by an organization’s size. This makes Backstory a more realistic proposition for smaller companies and offers clients more stability in terms of billing, given that data volume can fluctuate substantially.

Backstory’s ability to analyze data from multiple cloud sources, including AWS and Microsoft Azure, is another strong commercial advantage Chronicle has over its competition.

Google seeks to boost its cloud computing business and catch Amazon and Microsoft in the battle against digital crime with its recent $5.4B Mandiant deal.

An increasing number of businesses are generating more information, and as a result, need incremental computing and processing power to make sense of it. All of this will require more complex computing and additional computing infrastructure, which Google believes it can handle through its machine learning capabilities. Despite trailing behind Amazon and Microsoft in the cloud space, Google has an opportunity to capture some business from these competitors as customers seek expertise in machine learning, an area where Google remains differentiated.

“Other Bets” — Hidden Gems?

In the founders’ letter, Larry and Sergey wrote, “Google is not a conventional company. We do not intend to become one.” As part of that, they also said that one should expect them to make smaller bets in areas that might seem very speculative or even strange when compared to their current businesses.

“Many companies get comfortable doing what they have always done, making only incremental changes. This incrementalism leads to irrelevance over time, especially in technology, where change tends to be revolutionary, not evolutionary. People thought we were crazy when we acquired YouTube and Android and when we launched Chrome, but those efforts have matured into major platforms for digital video and mobile devices and a safer, popular browser. We continue to look toward the future and continue to invest for the long term.”

Alphabet’s investment in the portfolio of Other Bets includes emerging businesses at various stages of development, ranging from those in the R&D phase to those that are in the beginning stages of commercialization.

Over the past 7 years, Google's "Other Bets" have burned $28 billion. On the other hand, the company made that much in FCF over the past 5 months. Seems like a good asymmetric bet!

While these early-stage businesses naturally come with considerable uncertainty, some of them are already generating revenue. Google’s “other bets” brought in revenue worth over $750 million (>1% of total revenue) in 2021.

“throughout Alphabet, we are also using technology to try and solve big problems across many industries. Alphabet’s Other Bets are early-stage businesses, and our goal is for them to become thriving, successful businesses in the medium to long term. To do this, we make sure we have a strong CEO to run each company while also rigorously handling capital allocation and working to make sure each business is executing well.”

Google’s Other Bets include:

GV and CapitalG, are two of Google’s investment vehicles. GV or Google Ventures is the venture capital arm of Google, which invested in more than 300 companies that push the edge of what’s possible. From fields of life science, healthcare, artificial intelligence, robotics, transportation, cybersecurity, and agriculture. Capital G is the growth equity investment arm of Google that supports an investment portfolio of companies by providing tactical advice across key functional areas such as engineering, product, sales, and marketing. By working closely with growth-stage companies, CapitalG argues that its pattern recognition enables it to draw learnings and help our portfolio scale effectively.

Waymo, Google’s self-driving car initiative. Waymo began as the Google self-driving car project in 2009. Waymo is now an independent self-driving technology company with a mission to make it safe and secure for everyone to get around—without the need for anyone in the driver’s seat.

Verily and Calico, are two healthcare subsidiaries. Verily develops tools to collect and organize health data, then creates interventions and platforms that put insights derived from that health data to use for more holistic care management. With three guiding product design principles: start with the user, simplify care, and lead on security and privacy. The company monetizes by selling its R&D services. Calico is a research and development company whose mission is to harness advanced technologies to increase our understanding of the biology that controls lifespan.

Alphabet Access & Energy, which houses the company’s telecommunications projects and energy initiatives.

Sidewalk Labs, Alphabet’s urban innovation organization. Alphabet’s smart city startup, Sidewalk Labs, began in 2015 with the mandate to come up with new kinds of technologies to improve urban life. In the 6 years since Sidewalk Labs has become a kind of one-stop-shop vendor for smart city technology. Sidewalk Labs is positioning itself to be the dominant smart city vendor in two big ways: by leveraging Alphabet’s resources to make it financially feasible for towns and cities to work with the company, and by using other Alphabet companies to make its smart city offering more comprehensive.

DeepMind, an AI research arm acquired by Google in 2014, develops neural networks. DeepMind aims to solve intelligence, developing more general and capable problem-solving systems, known as artificial general intelligence (AGI). Recently, DeepMind programs have learned to diagnose eye diseases as effectively as the world’s top doctors, save 30% of the energy used to keep data centers cool, and predict the complex 3D shapes of proteins - which could one day transform how drugs are invented.

Cybersecurity spinoff Chronicle, which focuses on security solutions for Google’s cloud business.

Project Loon, is a subsidiary working to bring internet access to rural and remote areas.

Project Wing is developing an autonomous delivery drone service.

Google X, is an R&D facility focused on “moonshot” technologies aimed at improving the world.

Take Crazy Ideas Seriously

X – Google's moonshot factory stated aim is to pursue what it calls “moonshots” – to try to solve humanity’s great problems by inventing radical new technologies. X is not so much a company as a radical way of thinking, a method of pursuing technological breakthroughs by taking crazy ideas seriously. X’s job is not to invent new Google products, but to produce the inventions that might form the next Google.

Google founders Larry Page and Sergey Brin always believed in investing some of the company’s resources in hard, long-term problems. In 2010, “X” — a new division formed to work on moonshots: sci-fi sounding technologies that aim to make the world a radically better place. To that end, besides the self-driving cars (now a standalone company, Waymo) and internet balloons (Loon), X has built delivery drones (Wing), contact lenses that measure glucose in the tears of diabetics (Verily), and technology to store electricity using molten salt (Malta). It has pursued but ultimately abandoned attempts to create carbon-neutral fuel from seawater, and replace ocean freight with cargo blimps. It once earnestly debated laying a giant copper ring around the North Pole to generate electricity from the Earth’s magnetic field.

Google Brain, the deep-learning division that now informs everything from Google Search to Translate, began at X. So did camera software GCam, used in Google Pixel phones; indoor mapping in Google Maps; and Wear OS, Android’s operating system for wearable devices.

But those are beside the point. “Google Brain, the cars, Verily, everything else – those are symptoms. Side effects of trying weird things, things that are unlikely to work.

Alphabet is not the first company to set up a laboratory for chasing moonshot ideas. In 1925, AT&T and Western Electric founded Bell Labs, which assembled scientists and engineers from different disciplines to advance the field of telecommunications. Bell Labs invented the transistor, the first lasers, and photovoltaic cells, winning nine Nobel prizes in the process. Ever since, corporate research labs, from Xerox PARC to Lockheed Martin's Skunk Works and DuPont’s Experimental Station, have played a central role in producing breakthrough inventions. Apple, Facebook, Microsoft, and Amazon all have corporate research labs. Google has several, including Google AI (formerly Google Research), Robotics at Google, and Advanced Technologies and Projects, which works on things like AR and smart fabrics.

For all of X’s rhetoric about changing the world, it ultimately exists to produce new enterprises – and profit – for Alphabet. Google itself, after all, started as a kind of moonshot, to systematically map all of human knowledge. Alphabet is using its dominance in the search and advertising spaces — and its massive size — to find its next billion-dollar business.

Russian roulette is merely random. Although we cannot predict the outcome, we do know what the possible outcomes are, and the probability of each, provided that the rules of the game are obeyed. The future of civilization is unknowable because the knowledge that is going to affect it has yet to be created. Hence, the possible outcomes are not yet known, let alone their probabilities.

Imagine you can’t google the answers because—well, Google hasn’t been invented yet. I’m excited by how Google’s “other bets” will impact our civilization.

“We’re in an era of great inspiration and possibility, but with this opportunity comes the need for tremendous thoughtfulness and responsibility as technology is deeply and irrevocably interwoven into our societies.”

— Sergey Brin

Cost Structure

With over $250 billion in revenues in 2021, Google reported over $76 billion in net profits. This implies a few critical items in its income statements:

TAC

Google's growth is represented by its ability to keep a constant stream of traffic that gets monetized at high margins. Therefore its cost structure – a critical element of any business model – can be understood by looking at this metric — TAC. TAC stands for Traffic Acquisition Cost, and that is the rate at which Google has to spend resources on the percentage of its revenues to acquire traffic.

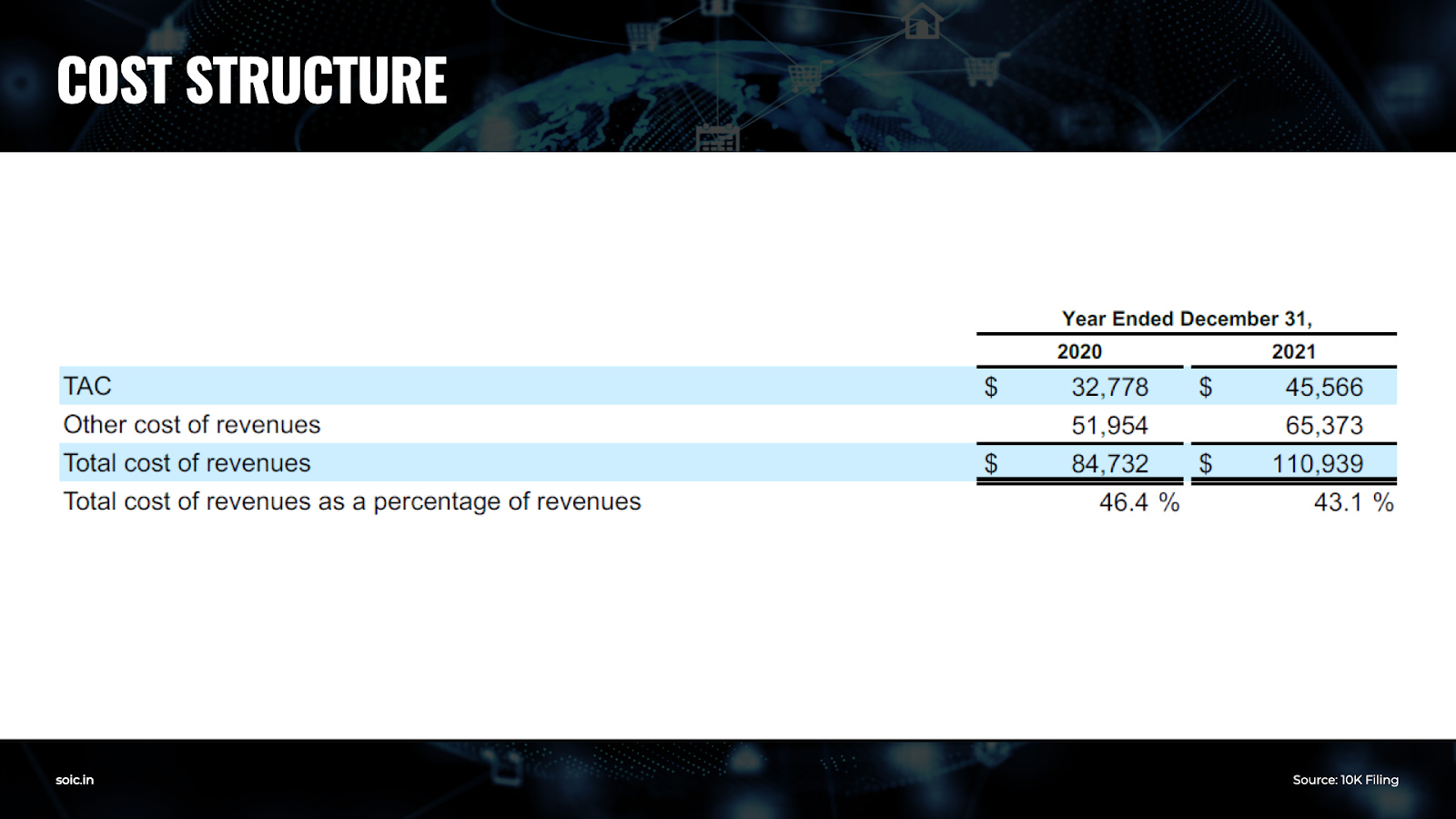

Google uses partnerships and distribution agreements to bring traffic to its properties. Those partnerships and agreements cost Google over $45B in 2021.

Google has two main channels to acquire traffic:

The Google Properties traffic acquisition based on partnerships and distribution deals (like deals with a browser to have Google as a default search engine) focuses on bringing as much traffic to Google‘s properties for monetization.

The Network Members traffic acquisition is based on Google Network Members (part of the AdSense program) to monetize those pages by displaying ads on their properties, generating revenues when site visitors view or click on the ads.

When it comes to Google its cost structure is pretty straightforward. To keep its operations profitable, it needs to be able to generate traffic at much lower costs, than it can monetize it. Hence, the sustainability of TAC Rates becomes important. Throughout the years’ Google has been pretty good in keeping its traffic acquisition costs low compared to its ability to monetize the pages where advertising got sold. The increase in TAC from 2020 to 2021 was due to an increase in TAC paid to distribution partners and Google Network partners, primarily driven by growth in revenues subject to TAC. The TAC rate decreased from 22.3% to 21.8% from 2020 to 2021 primarily due to a revenue mix shift from Google Network properties to Google Search & other properties. This shows that a lot of that adoption was organic, and based on strong deals the company has in place.

The increase in other costs of revenues from almost $52B in 2020 to over $65B in 2021 was driven by increases in content acquisition costs primarily for YouTube, data center and other operations costs, and hardware costs. The increase in data center and other operations costs was partially offset by a reduction in depreciation expense due to the change in the estimated useful life of our servers and certain network equipment beginning in the first quarter of 2021.

All in all — Google’s total cost of revenues as a percentage of revenues has decreased from 46.4% in 2020 to 43.1% in 2021.

In terms of profitability, Google Services has huge margins! Google Services brought in over $91B in 2021 indicating margins expanding to over 38% from 32% in 2020. Google managed to improve monetization for users, it saw mobile users’ growth, while it managed to lower its traffic acquisition costs—This combination led to an improved marginality.

However, it’s also interesting to notice how the Google Advertising machine is the only one running at positive margins. Where instead, both the Google Cloud platform and the other Google Bets run at negative margins. Important to distinguish here.

The Google Cloud platform has shown strong indicators of turning profitable with scale.

When it comes to the other bets those instead are breakthroughs that Alphabet is pursuing with a long-term perspective. Those are money-losing bets for now but might turn into something interesting in the coming decade.

AI for humanity is more important and profound than what fire was!

In October 2016, CEO Sundar Pichai highlighted the importance of artificial intelligence to the tech landscape moving forward, explaining, “It is clear to me we are evolving from a mobile-first to an AI-first world.” Since then, AI has become the company’s focus across its investments, acquisitions, and internal spending.

Google has launched two funds dedicated solely to AI: Gradient Ventures and the Google Assistant Investment Program.

Gradient Ventures was launched in July 2017. Unlike GV and CapitalG, which run separately from Google under the Alphabet corporate framework, Gradient Ventures is accounted for on Google’s balance sheet. That said, the fund plans to break off from the main company once it ramps up its investment pace.

Google has also launched a fund to build out its capabilities for Google Assistant, Google’s virtual assistant that uses natural language processing to take voice commands from users and search the internet, schedule events, and set alarms, among a host of other tasks. Launched in May, the Google Assistant Investment Program is focused specifically on early-stage startups working with Google’s virtual assistant.

In addition to investing through its new investment vehicles and more established funds, Google has also been actively acquiring AI startups for the past few years.

One of the initial forays into AI and machine learning was its $600M acquisition of AI startup DeepMind in January 2014. DeepMind currently operates as a subsidiary of Alphabet, and has been a pioneer in the machine learning space, with its program beating a human world champion in the board game “Go.”

More recently, it has acquired Halli Labs, an India-based AI startup focused on deep learning and machine learning systems, and AIMatter, a computer vision company using a neural network-based AI platform to process images. The company also acquired Banter to build out its natural language processing capabilities for enterprise cloud services like Google Hangouts.

Google is also investing internally in its machine learning capabilities by ramping up its R&D spend, which it largely dedicates to its main areas of strategic focus (such as search and machine learning). Google has invested more than $100 billion in R&D over the last five years.

The main engine for Google’s internal research on AI and machine learning is Google AI. Formerly known as Google Research, the project was recently re-branded to reflect the company’s newfound focus on AI.

Within Google AI sits the Google Brain team, which has led the charge in developing TensorFlow, Google’s open-source software library. The team also improves core capabilities from translation to voice search.

Google Brain works closely with several of Alphabet’s subsidiaries, including autonomous driving division Waymo, where it has helped apply deep neural nets to vehicles’ pedestrian detection systems. The team has also made inroads in the energy space, helping Google realize cost and environmental savings at its power-hungry data centers to improve power usage efficiency by 15%.

Google is also focused on building out its deep learning capabilities, which is more complex than traditional machine learning in that it generates predictions using an artificial neural network inspired by the human brain. Unlike machine learning, deep learning algorithms do not require adjustments from engineers and should be able to determine on their own if predictions are accurate or not.

"AI models are typically trained to do only one thing. With Pathways, a single model can be trained to do thousands, even millions, of things."

Google’s recent investments and activity suggest that the company is prioritizing deep learning and natural language processing so that it can more effectively process and manage growing amounts of information from both consumers and enterprises.

As CEO Sundar Pichai said at the Google conference, Google is rethinking “all” of its products for an AI-driven future.

With AI as the priority, the company is focused on developing sophisticated machine learning capabilities through both outside investments and in-house development.

“Artificial intelligence will prove to be the most important technological development since Gutenberg’s printing press. The printing press made information more widely available; AI is making intelligence more widely available.”

— Brian Arthur

The Fuel That Keeps The AI Fire Going Is Data

A classic supply chain moves from upstream to downstream, where the raw material is transformed into products, moved through logistics and distribution to final customers. A data supply chain moves in the opposite direction. The raw data is “sourced” from the customer/user. As it moves downstream, it gets processed and refined by proprietary algorithms and stored in data centers.

At its core, Google is a data collecting organization. Indeed, in search, Google is the best collector of users’ data to capture commercial intent sold as advertising.

In recent research made by Professor Douglas C. Schmidt, Professor of Computer Science at Vanderbilt University, and his team it is interesting to see how Google collects way more data in the ecosystem created by it, such as the devices using Android.

Google learns a great deal about a user’s personal interests during even a single day of typical internet usage. In an example “day in the life” scenario, where a real user with a new Google account and an Android phone (with a new SIM card) goes through her daily routine, Google collected data at numerous activity touchpoints, such as user location, routes taken, items purchased, and music listened to. Surprisingly, Google collected or inferred over two-thirds of the information through passive means. At the end of the day, Google identified user interests with remarkable accuracy.

This ability to identify users’ interests with “remarkable accuracy” comes from Google's investments over the years in creating the proper infrastructure that could support its supply chain of data.

Often the supply chain of data needs to rely on the physical supply chain and vice versa.

Indeed, when you’re able to get your hardware in the hands of users that is the best it can happen if you run a company that makes money based on data it collects from its users. Google’s move needs to be understood in terms of a supply chain of data.

Can you guess what the enabler of Google data collection is? Android is a key enabler of data collection for Google, with over 3 billion monthly active users worldwide.

Android has been the best-selling mobile OS every year since 2011, and today has about over 70 % market share in the smartphone market.

In 2014, Google launched its plan to expand the Android operating system to a range of other devices, which included a wearables project called Android Wear (which was rebranded as Wear OS in March 2018). Google has consistently invested in developing Wear OS to compete with incumbents such as the Apple Watch. It deepened its presence in the wearables space when it acquired Fitbit in January 2021 after more than a year of talks.

Google made one of the most significant updates to Wear OS in the operating system’s history in March 2021 when it opened Tiles — at-a-glance cards that display weather forecasts, fitness metrics, and other data via swipe gestures — to third-party developers for the first time.

Despite these developments, Wear OS accounted for just 3% of smartwatch shipments in 2020.

Google’s expansion of the Android operating system also included the Android TV. Android TV succeeded the original Google TV, which was discontinued in June 2014.

Google revamped Android TV’s interface in February 2021 to more closely resemble Chromecast’s Google TV. Given the similarities and the potential for confusion among consumers, it seems likely that the two platforms could be merged into a single service at some point.

In 2017, Google released a selection of new “smart” home devices that are not reliant on the Android ecosystem: the Google Home, new Chromecast devices, a new VR headset, and a new Chromebook laptop with a built-in Google Assistant.

Google’s growing range of smart-home products has seen considerable investment and remains one of Alphabet’s strongest potential growth opportunities, reflecting heightened consumer interest in smart-home products. Since acquiring Nest Labs for $3.2B in 2014, Google has developed smart-home products that encompass remote monitoring and climate control via smart thermostats, as well as home security devices like cameras and intruder detection systems.

Google confirmed its plans for a new range of Nest-branded security cameras in January 2021. The company also plans to further integrate its smart-home services with its fitness tracking products by adding sleep tracking functionality to its Nest Hub devices.

As voice search is approaching Google needs to be on top of the data game, and that explains the next run to dominate the voice assistants devices market. Ultimately, Google wants to “help users get things done” through a combination of search and assistant.

“…at a high level the next big evolution we are doing as part of mobile search and Assistant is to actually help users complete actions, to help get things done. And it’s really hard to do at scale, and that’s the work we are doing.”

— Sundar Pichai

Google has outlined a future capability for the Assistant: a voice system that can carry out phone calls on a user’s behalf. Called Duplex, the technology is the first of its kind among even the most advanced digital assistants and ushers in a new stage in the race for voice and AI supremacy.

Since its launch, Google Assistant has been rated far more capable and useful than its main competitors, Microsoft’s Cortana and Apple’s Siri. Driven by Google’s internal deep learning-focused Tensor Processing Unit chips, Google Assistant is available on all Android and Google Home devices and runs on a reported 1B devices. Android itself is running on more than 2.5B devices today, while Wear OS is available on smartwatches from companies like Michael Kors, LG, and more.

Google has invested heavily in its voice recognition technologies to retain its competitive edge. It has focused particularly on the nuances in natural-language processing (NLP) technologies that allow Google devices to learn the idiosyncrasies of users’ speech for challenging words such as certain names and common mispronunciations of everyday words.

Now automakers are coming to Google for help building out software for their in-car infotainment systems. Volvo, General Motors, Fiat Chrysler, and Nissan will all be working with the company to integrate Google Assistant, Google Maps, and Google Play Store into upcoming makes and models.

This approach is Google’s trademark play in consumer electronics: not building its own branded products, but building software that powers compelling consumer electronics products. Consumer demand puts pressure on watchmakers, automakers, and other companies to integrate tools like Google Assistant and Google Maps into their products. Even Microsoft adopted Android in its Surface Duo device, which launched in September 2020.

Google is also building some of its hardware as well though under the Made by Google line — including the Pixel smartphone, the Chromebook, and the Google Home — but the company is doing more important work on hardware-agnostic software products like Google Assistant (which is even available on iOS).

Google’s vision to dominate the smart home market and own the entire stack of hardware devices ties in closely with the digital assistant. The company has focused on its presence in hardware to build out its devices end-to-end, in part to relieve rising costs from third-party hardware manufacturers and also for more seamless integration between its software and hardware.

The decision to bring its Nest business back under Google’s hardware division signals Google’s interest in integrating all its products with a simple assistant, which would provide the company with more channels to advertise and provide information to consumers.

Ultimately, the more Google is able to scale its virtual assistant technology across its suite of products — in everything from mobile devices to the Google Home to other connected personal devices — the better the foothold it will gain in the search and advertising world.

On September 21, 2017, Rick Osterloh, Senior Vice President of Hardware at Google announced a historic agreement between Google and HTC with these words:

With this agreement, a team of HTC talent will join Google as part of the hardware organization. These future fellow Googlers are amazing folks we’ve already been working with closely on the Pixel smartphone line, and we’re excited to see what we can do together as one team. The deal also includes a non-exclusive license for HTC intellectual property.

Another example is how Google invested in KaiOS, an operating system, that transforms feature phones into smartphones, providing them also with a default voice assistant (KaiOS phones use by default the Google Assistant). KaiOS feature phone business model wants to bring connectivity and the digital revolution to those developing countries (like India and Africa) that have missed out on the smartphone wave due to the high costs of those devices. Besides, KaiOS might be well suited for the IoT revolution.

The hardware is a critical access point as people can relate with a brand via hardware and when you can enter the hardware space, you can pretty much control the whole value chain. By trying to scale up the hardware side, Google can finally have access to the data at its source. In the next generation of hardware, AI will be the critical differentiator, not hardware. Alphabet’s hardware strategy is being driven by its work in artificial intelligence. Thus this isn’t a competition with Apple; this is a competition for the next era of AI — where the quality of the data is a critical element.

Building Out A Network Infrastructure For Computing

Google is heavily invested in developing a network infrastructure to handle higher levels of computing. The company has cited that one of the main drivers of its capital expenditures is building out compute capacity, as more complicated machine learning capabilities increasingly require more processing power.

“We’re focused on capex as a lens into the outlook for growth for additional compute capacity, which has a number of growth drivers, including supporting growth in our search and ads business as well as newer businesses.”

— Ruth Porat

Additionally, Google has invested heavily in several subsea cable projects to support its computing capabilities. The cable is intended to increase network capacity across the internet and also support the growth of Google Cloud.

As Google increases its capabilities in machine learning and cloud, it will need to build out the infrastructure to support it, such as fiber-optic cables. According to the company’s SVP for technical infrastructure, Urs Hölzle, Google needs to double its transmission capacity each year to maintain its core businesses.

Fiber-optic cables have traditionally carried telephone traffic, but lately, content and cloud computing flows are dominating traffic flow, making up 77% of data traffic across the Atlantic Ocean and 60% across the Pacific Ocean. As a result, Google is investing in submarine fiber-optic cables, most notably to connect to areas with growing internet usage.

In addition to network infrastructure, the company also must build out the computing capabilities of its hardware so that it can own the computing stack from end to end.

Google aims to pioneer the most advanced computing technology, which at the moment seems to be quantum computing.

Quantum computing provides substantially more processing power than a traditional computer, processing more information at a faster rate. As co-founder Sergey Brin outlined in the company’s 2017 Founder’s Letter:

“For a specialized class of problems, quantum computers can solve them exponentially faster. For instance, if we are successful with our 72 qubit prototype, it would take millions of conventional computers to be able to emulate it.”

As a result, Google is investing substantially in quantum computing and has come to be seen as one of the leaders in the space, along with Intel and IBM.

Google is looking to put its machine learning and engineering expertise to work building the next generation of high-performance computer chips and revolutionizing computing itself with quantum computing developments.

The main issue Alphabet is looking to address is that efficiently solving a certain class of problems with machine learning requires processing power that isn’t available through modern chips.

While there are some physical limitations to contend with in developing chips for AI, Alphabet’s focus on quantum computing could help overcome them.

When it comes to artificial intelligence, Alphabet is working on solving a two-pronged problem. AI applications require hardware with extremely high computation capacity, but they also need to optimize for efficient energy consumption.

Google’s main quantum efforts are branded under Google Quantum AI and the company sees artificial intelligence as a key application of quantum computers — even in the near term with only moderately powerful machines.

Google has also developed an open-source platform for building quantum machine learning models, TensorFlow Quantum.

Alphabet is investing heavily in all sorts of AI tools to integrate into its businesses. Though quantum machine learning is only one aspect of this broader strategy, the company is indicating through its big bets in the space that it is bullish on the tech. If it succeeds, then Alphabet could use quantum computing to eventually boost AI initiatives across its entire business.

“As we are thinking about AI, it all starts with foundational R&D we do. I think we are one of the largest R&D investors in AI in the world. And so thinking ahead and doing that and we are doing it across all the foundational areas and we are taking many diverse approaches.”

— Sundar Pichai

Many of Alphabet’s businesses make use of AI in some capacity. These areas could be given a significant boost by advances in quantum AI, including business lines like:

Search and ads — Quantum computing will allow for better ways to parse through big datasets quickly. Advances in natural language processing (NLP) that stem from quantum machine learning could help deliver more relevant and targeted search results and ads.

Waymo — Quantum machine learning could help AI make faster decisions based on fewer data. Applying this to self-driving car tech could help autonomous vehicles better adapt to dynamic situations on the fly.

Google Assistant — Just as quantum NLP could help Google better understand websites, it could also help its voice assistant better interpret requests. The company may be hoping to gain a quantum edge over rival voice assistants.

Google Cloud — As well as offering cloud-based quantum computing services to enterprises, Google could use quantum algorithms to better manage tasks like cloud data storage.

DeepMind — DeepMind has built a reputation for pushing AI capabilities to the edge, like with its protein folding prediction tool for drug discovery. Quantum machine learning would amplify many of DeepMind’s tools and may eventually help defend against competitors looking to catch up with it.

Recently, Alphabet has announced that it is spinning off the quantum technology unit, Sandbox, into an independent company.

Capturing Digital Commerce

When it comes to digital commerce, Google’s main objective is to protect its advertising business from all angles. Product search is a critical component of Google’s business, and the company cannot afford to lose more of that business to e-commerce giant Amazon.

With Amazon’s recent rise to the top of e-commerce, Google has lost a substantial amount of its product advertising volume, which makes up roughly 60% of the company’s ad clicks. Additionally, both Amazon and Apple have spent billions on content and music services to make their media/app platforms stickier, posing a direct threat to Google’s ability to dominate its advertising business across platforms.

Now, Google is fighting back, making a notable push in digital commerce.

Google’s recent attempts to reclaim its territory in product search include its March 2018 launch of Shopping Actions, a tool that integrates the retail experience across Google’s platforms (including mobile, desktop, and voice-powered devices). Early tests suggest that the project is increasing online shopping cart sizes by as much as 30%.

In 2017, Google partnered with some major retailers, including Walmart, Target, and Costco, to bolster its delivery platform, Google Express. The platform allows users to shop across several retailers with free delivery over a certain threshold.

Capturing digital commerce is critical to Google’s strategy moving forward, as it allows the company to recapture a portion of the product searches it has lost to Amazon while also providing another valuable avenue for collecting consumer data.

“E-commerce is evolving a lot and we continue to invest there. Google shopping is doing well. And we work hard to make sure we bring the best experience possible, which is why we partner with companies like Walmart for example to make it easier to buy products. Consumer behavior is changing but we are comfortable given the breadth of how we do things and how we are focused on user experience there.”

— Sundar Pichai

Digital commerce is also inherently tied to Google’s cloud business. The more retailers that Google partners with on the digital commerce front, the more opportunity it has to extend its expertise in enterprise cloud services.

“On the commerce front, obviously, it’s a natural sector I think for us to drive partnerships. We already have deep advertising relationships with many of these providers, increasingly. Shopping is an area where we are beginning to work together. And finally, I think the cloud is another important way by which we can start working together.”

— Sundar Pichai

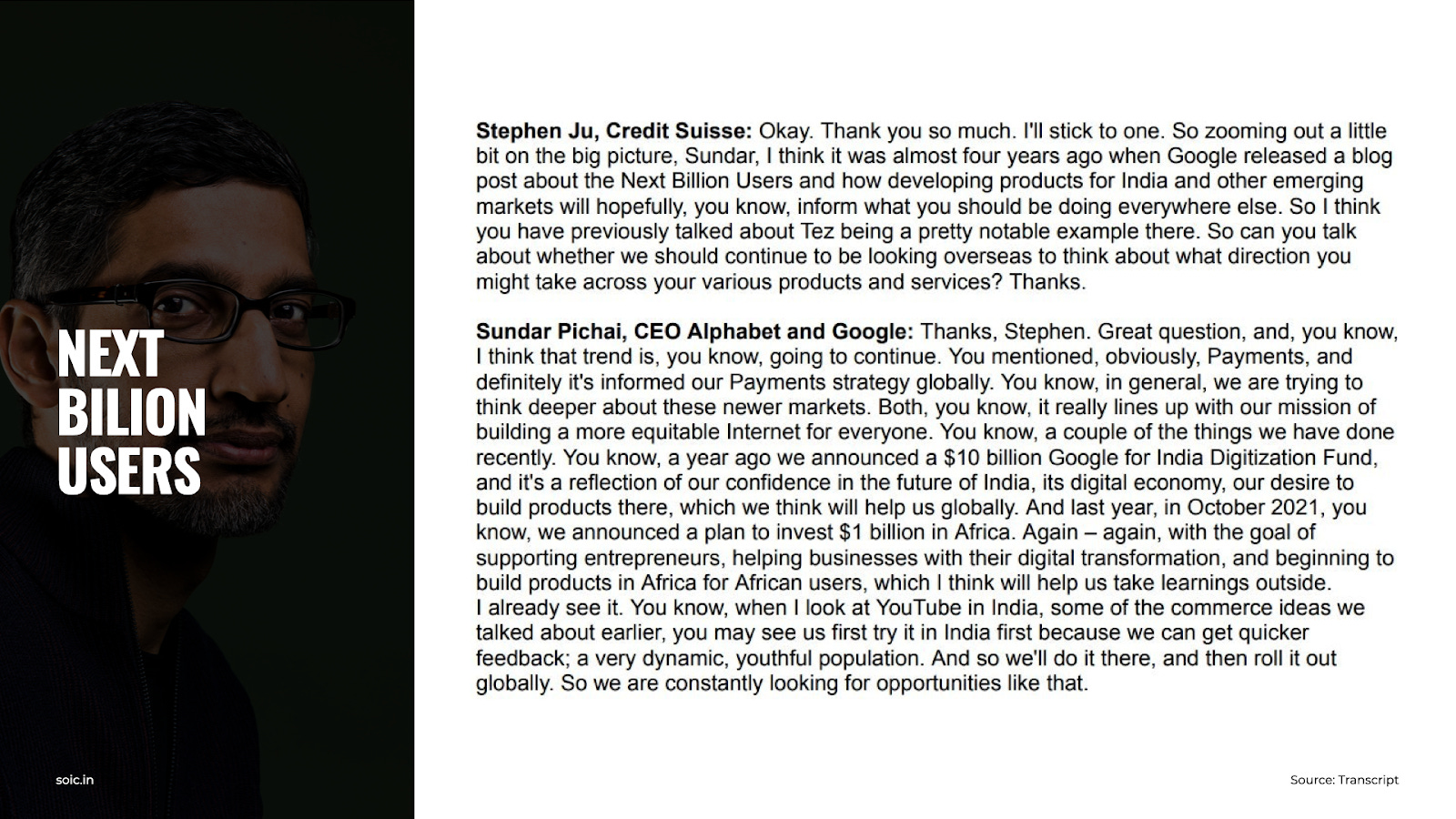

Next Billion Users — Expanding in India, Africa & Southeast Asia

Google’s recent investments, partnerships, and internal projects suggest an interest in building out a presence in India, Africa, and Southeast Asia, regions that are experiencing outsized growth in internet usage. These emerging economies offer incremental revenue streams as connectivity improves and more and more consumers gain access to the internet.

Google has ramped up its investment in emerging markets in recent quarters, seeing explosive growth in digital commerce. Building up its e-commerce presence allows Google to capitalize on the growth in these regions while also maintaining its foothold in search and advertising.

Economies Of Scale Plus Reinforcing Demand And Supply Advantages.

The advantages of Google’s scale flow from both the relative size of its fixed-cost base and network effects; it retains customer captivity of both consumers and advertisers because of habit, switching, and search costs; and it secures major cost advantages through proprietary technology-enhanced continuously by learning and data.

The greatest benefits of scale in search are from the old-fashioned supply-side variety and stem from the ability to spread the huge fixed-cost requirements over the larger user base. Consider the fixed costs required to undertake the process of organizing the world’s information and the value of having a large R&D budget to continuously improve each critical step in the chain that produces search results on an ongoing basis. Google’s “crawler” programs automatically search the web and download pages to Google data centers. Google’s technology in this area determines the completeness of search results. Google’s “indexer” programs then organize the downloaded material into its databases and benefit from the design of the hardware and software of Google’s massive data centers. The efficient organization of Google’s data centers is itself subject to a technology patent. This hardware and software together account for the superior speed of Google searches. Finally Google’s “query processor” organizes search results for presentation to users. The combined effect of these investments and technologies make Google search results superior in completeness, speed, and, most important, relevance to those of other search engines.

“The higher the number of advertisers using an online search advertising service, the higher the revenue of the general search engine platform; revenue which can be reinvested in the maintenance and improvement of the general search service so as to attract more users.”…

“The higher the number of customers a business has, the higher the costs of the business, costs which must be invested in the maintenance and improvement of the business if it is to serve that higher number of customers.”

What matters (of course) is how costs and revenue increase as scale increases.

— Hal Varian

Google benefits from several network effects as well. Because Google’s search engine is ubiquitous, new users are likely to be introduced to it and trained to its use before even learning of its rivals. Other websites are also more likely to use Google because of its strong position with users. These tendencies, in turn, then increase the number of Google users, which is further reinforcing.

You must have noticed that when you start to write a search query, Google’s autocompleting feature often magically guesses what you might be planning to ask. This trick is based in part on the voluminous data the engine has about what other users are asking, suggesting a network effect from every incremental user improving the search experience of all users. More broadly, there is little question that Google’s greater familiarity with prior search behavior drives a scale advantage on the demand side by facilitating the effective customization of the selection and presentation of search results for individual users.

But all prior experience is not equal. The incremental value of a new search query by one user for the results of another user is trivial. On the other hand, Google learns a lot about how to optimize results by looking at the same user’s previous queries and clicks. So to the extent that there is a direct network effect on the user side of search, it is overwhelmingly driven by the number of one’s prior searches rather than the number of other searchers.

"I think you're going to continue to see us lead in Search quality. I just find the world of information is only continuing to grow, and it's getting increasingly multimodal in nature. Just like we took the lead from text to images, thinking through video, audio, incorporating it, and then providing it back to users regardless of whether they are typing, speaking, or looking at something, wanting an answer."

In advertising, Google benefits from more than just the ubiquity-related network effects that apply to search. For example, its AdSense program, which places ads on blogs and other relatively small, decentralized sites, is especially attractive to advertisers because of its wide access to such sites and ability to customize placements based on extensive experience with these sites. At the same time, websites are drawn disproportionately to AdSense because that is where the greatest concentration of advertisers resides. AdExchange, Google’s real-time bidding exchange for premium publishers and big brand advertisers, benefits from the same network effect dynamic.

Many of Google’s products in the area were rebranded as Google Ad Manager in 2018. AdSense and AdExchange—collectively reported as Google Network Members’ properties—Google’s businesses that benefit most strongly from network effects, are a fraction of the size of the core search business that benefits predominantly from the supply-side scale. The advertising revenue from this segment is less than a fifth of the revenue from Google’s owned search properties, including Google.com, YouTube, Gmail, and Maps. And that proportion has been falling for years.

Customer loyalty, from both searchers and advertisers to Google’s search engine is a critical factor reinforcing the benefits of scale. Users become more effective at using particular search programs with experience, and that experience makes the incumbent search engine more effective at delivering relevant results. The sacrifice of this historic search investment by moving to a new search engine is a further source of loyalty to Google. Experience with Google advertising and Google’s automated programs for placing ads leads to advertiser loyalty in the same way that experience reinforces searcher loyalty. This multisided and multifaceted loyalty is enhanced by the ongoing product improvements in both the quality of search results and advertising effectiveness. These enhancements increase switching costs as users recognize the futility of finding equally satisfying search results elsewhere.

Proprietary technology is the most substantive advantage a company can have because it makes your product difficult or impossible to replicate. Google’s search algorithms, for example, return results better than anyone else’s. Proprietary technologies for extremely short page load times and highly accurate query auto-completion add to the core search product’s robustness and defensibility. It would be very hard for anyone to do to Google what Google did to all the other search engine companies in the early 2000s. The steady improvement in proprietary algorithms over time has led to both increasing click-through rates for Google ads and steadily higher conversion rates for advertisers from clicks to sales. The latter improvements have, in turn, led to steadily higher advertising prices. In both areas, Google significantly outperforms its competitors and the gap is only increasing over time. The integrated advantages of data-driven learning and technology are persistent and continue to grow without topping out.

The core scale advantages that come from the vast and growing investments in both search and advertising R&D reinforce these already tightly connected supply and demand advantages. This kind of virtuous cycle between Google’s learning-enhanced proprietary technology and network effect supported customer captivity among both users and advertisers on the one hand and traditional cost-based economies of scale in R&D and other areas suggest that its remarkable economic performance is likely to endure.

Risks

“The essence of risk management lies in maximizing the areas where we have some control over the outcome while minimizing the areas where we have absolutely no control over the outcome and the linkage between effect and cause is hidden from us.”

― Peter L. Bernstein

Alphabet has listed numerous risks to its business and industry in its 10K — From Regulatory Risk (antitrust complaints filed by the U.S. Department of Justice and several state Attorneys General, the Digital Markets Act in Europe, and various legislative proposals in the U.S. focused on large technology platforms) to general business risk such as technological shift, competitive pressure, uncertain return on investments, etc. To learn more about it, you know what to do… Google it! :)

As investors, I believe we can’t do much more than just be aware of risks — It’s not in our control. What is in our control, is the price we pay in light of those risks.

Alpha-Bet?

As of 2021, Alphabet generated over $257 billion in revenues, at the base of over $180B in 2020. Over $209 billion (over 81% of the total revenues) came from Google Advertising products (Google Search, YouTube Ads, and Network Members sites). The advertising business—the only profitable one comes at over 40% margins still growing over 20% at this base.

This is followed by over $28 billion in other revenues (comprising Google Play, Pixel phones, and YouTube Premium) and by Google Cloud, which generated over $19 billion in 2021, growing at over 35% and is sitting on massive operating leverage.

Google’s search and advertising businesses, which is a cash machine, have laid the foundation for Alphabet to pursue a broad range of projects, experiment with moonshots, and strategize how it might disrupt industries like healthcare, banking, and transportation. Other bets are money-losing bets for now but might turn into something interesting in the coming decade.

In 2021, Alphabet generated over $92B in operating cash flows and invested back over $25B in CAPEX and around $50B in share buybacks.

"We continue to generate strong FCF with $18.6 billion in the quarter and $67 billion in 2021. We ended the year with $140 billion in cash and marketable securities. We also repurchased a total of $50 billion of our shares in 2021."

The most powerful investments merge dualities — Resilience & Optionality into one. This is where investment returns are at their most nonlinear. Google’s advertising has proven its resilience through its adaptability to evolving web experiences over the years. Google cloud and other bets present themselves with massive optionality.

There are fundamental flaws in using the backward-looking stuff—At the end of the day, 100 percent of the value of any equity depends on the future, not the past. At a $1.5 Trillion market cap, do you think Alphabet is an Alpha-Bet? In my judgment, it is! Let me know what you think…

Thank you for reading, see you soon!