Intellect Design Arena - The "Tech" in Fintech

Shovel in the Digital Transformation 'Gold Rush'!

A capitalist economy is best understood as an evolutionary system, constantly creating and trying out new solutions to problems in a similar way to how evolution works in nature. Some solutions are ‘fitter’ than others. The fittest survive and propagate. The unfit die. The great economist Joseph Schumpeter called this evolutionary process “creative destruction.”

Schumpeter highlighted the importance of risk-taking entrepreneurs to make it work. Thus, the entrepreneur’s principal contribution to the prosperity of a society is an idea that solves a problem. These ideas are then turned into the products and services that we consume, and the sum of those solutions ultimately represents the prosperity of that society.

Capitalism’s great power in creating prosperity comes from the evolutionary way — it encourages individuals to explore the almost infinite space of potential solutions to human problems, scale up and propagate ideas that work, and scale down or discard those that don’t.

For a long time, most companies considered IT as something that supported the business—software and servers that ran the back office, or the PC on every desk. You had big software to manage the financials, and an even bigger enterprise resource planning (ERP) system to keep tabs on inventory, shipments, and other kinds of complex logistics. But essentially this was all bookkeeping—of money and materials.

IT also ensured employees had computers to do their job and printers to print things. In the 1980s and ’90s, these were all cost centers, meaning they cost the company money and did not, in and of themselves, make money. So it made sense for many companies to cut corners as much as possible and outsource this function, often to offshore firms where talent was less expensive.

But along came the web, and then mobile, and suddenly the interface that most companies had with their customers became digital.

The software went from the back of the business to the front. Instead of just automating back-office chores, software became the face that a company presents to the world. Instead of walking into your bank, you used an app.

This had two critical implications for the world of software:

Customers suddenly did care about the software that companies used because the customers directly interfaced with it. If you had a better website or mobile app than your competition, it would be a good reason for customers to pick you.

It meant that new competition could enter the market more easily. To become a bank or a retailer, you didn’t need to open up a branch or store on every street corner. You just needed an app or a warehouse somewhere.

These two trends became apparent in the early 2000s. Suddenly startups that were great at building software, and had no legacy infrastructure or storefronts to deal with, began springing up.

These digital-native companies focused their early energy on creating great customer experiences, and they used their software-building expertise to their advantage.

The new playing field was digital.

Digital has disrupted and reshaped every conceivable industry. And while banking has been disrupted, banks still struggle to find firm footing in this fluid technological age. Unlike travel or shopping or transportation, they have yet to slip into a low-friction groove of progress. This has less to do with adopting new technology than it does with how that tech is leveraged.

The battlefield, therefore, is not the technology itself, but one of better customer experience.

Transforming the customer experience is at the heart of digital transformation. Digital technologies are changing the game of customer interactions, with new rules and possibilities that were unimaginable only a few years back.

In the world of banking, there is today an inordinate amount of focus on technology, without the fortification of a viable architecture that will help them leverage the data and tech at their disposal to the fullest, and toughen them from disruption.

Bankers all over the world have witnessed the journey of transformation using technology—The arrival of ATMs replacing tellers, the trill of call centers, and the ubiquity of the internet displacing branches, and more recently, IVRs (Interactive Voice Response) replacing agents. And while the mix of all of this change is bringing about enormously interesting opportunities, a host of challenges constantly nip at the heel.

If we riffled through the history of computing even with half an eye, it becomes clear that banks have traditionally been front-runners in adopting new technology. And at that inflection point when money went electronic, conventional and new financial instruments found their way into the market, each more complex than the last. Technology began to dictate the way business was conducted in financial institutions.

Despite all this, the emergence of fintechs triggered a game of technological catch-up. A game that was rigged against large legacy institutions from the word go.

Fintechs themselves did not arrive out of the blue. They are not a cause, but a symptom of a powerful phenomenon characterized by Amazon, Netflix, Google, and their ilk – a tectonic shift in customer experience.

Customers have been influenced by the digital experience of technology companies like Netflix and Google. They want more intuitive and personal service, no matter the provider.

Most new banking entrants understand this and offer simple and personalized products to win customers and eat into the market share once held by traditional banks. The rules of engagement have changed and will continue to change.

Buyology is a core science for designing banking in the new world of Freakonomics, where everyone is struggling to understand the methods to get customers buying, and is defined as the science of understanding business relationships. It is all about knowing why people buy and how to create business encounters where purchases are made that can be replicated over and over. In other words, it is the ability to create long-term business relationships, not just a one-sale stand.

“Looking at it from sales and growth specifically, the biggest trend right now is how important customer experience is in developing and supporting a brand and improving sales performance. The customer decides when and how they want to interact with brands, and this impacts the way companies sell to their customers. Big macro trends, such as social, mobile, cloud, big data, and IoT help create different experiences, but ultimately the customer is becoming far more disruptive than the technology itself and shaping entirely new industries.”

— Tiffani Bovi, Salesforce.com’s Global Customer Growth, Sales and Innovation evangelist

We are in the middle of a dramatic and broad technological and economic shift in which software companies are poised to take over large swathes of the economy.

“Software eating the world” has catapulted the tech industry’s total available market (TAM) from “IT” to the global economy. Before the 2000s, tech companies typically sold digital tools to help companies improve productivity. Today, they compete with mature companies in the media, retail, financial, and automotive industries, among others, forcing incumbents to modernize and embrace digital transformation and, in turn, creating demand for software.

Companies that adapt to the new digital landscape will serve customers better and will survive. Those that don’t, will die. It may not be overnight, but it’s inevitable.

Understanding the emergence of the digital supply chain is critical to success in the digital economy.

Think about industries that produce physical goods—things like cars, refrigerators, houses. They have mature supply chains. Auto manufacturers don’t create every piece of a car themselves. They buy steel from a steel company, leather from a leather company, seats from a seat company, and so on. As industries mature, so do their supply chains, allowing many companies to specialize in parts of the process, making the entire industry more efficient and productive.

Until recently, the software industry had no such thing. Like Microsoft, Oracle, or SAP, most software companies pretty much wrote all of their own software end-to-end. That worked when the software was a highly specialized field and there were relatively few software companies, right up through the 1990s and into the 2000s.

But now every company is becoming a software company, and most companies can’t build everything from scratch. They need a supply chain—just like Ford and Toyota—that divides the industry into areas of expertise and allows each company in the ecosystem to specialize on its core competency.

But the software supply chain looks different. Instead of specializing in tires or steering wheels, software supply chain companies deliver reusable chunks of code that developers bring together to make finished applications. These are Application Programming Interfaces (APIs).

What is an API?

An API is an interface. The abstract concept of “interface” is defined in Communication Theory as “a point of interaction between several systems.” An integral part of Systems Theory, this concept is used for describing or modeling any type or form of system.

An API provides the means for one program to access the information and capabilities of another. An engineer writes a bunch of code to manage complex things and builds an API on top of the code to abstract away most of the complexity so that using all of that code is as simple as writing a few lines of code.

APIs give individuals and companies the power to add functionality to a website, application, platform, or software without having to write the code. This is accomplished by integrating the API code into a company's existing code.

APIs can be described as everything from Lego building blocks to front doors to even veins in the human body. Because the defining property of APIs is that they’re ways to send and receive information between different parts, communicate between software applications.

APIs, therefore, give companies access to data and competencies they wouldn’t otherwise have—or better yet, that they no longer need—by letting even non-tech and small companies combine these building blocks to get exactly what they want. This means companies today—including non-tech companies and small companies—can focus on their core competency instead, access bigger data, and get superpowers to scale.

The API interface is becoming the interface for business. In much the same way that storefronts gave way to applications and websites. APIs are changing the interface of business today and how entire companies are being formed from—or around—them.

Each API supplier provides only a piece of the solution—Amazon Web Services delivers the data center. Twilio provides communications. Stripe and PayPal enable payments.

When a company chooses to plug in a third-party API, it’s essentially deciding to hire that entire company to handle a whole function within its business — An increasing number of the things that firms hired whole teams of people to do are now achievable with a few lines of code.

Modern apps integrate dozens of these small components into a unique value proposition for the customer. This shift to component software is the next big leap in the evolution of the software industry.

To understand the new way of thinking about software, we need to look back at how the software industry began and how it has evolved.

At first, companies ran mainframes. Many still do—more than you might imagine. Then came minicomputers, Unix workstations, and finally the PC. From mainframes to PCs, the computers kept getting smaller, the operating systems changed, but the software industry pretty much used the same business model. A software maker would invest R&D dollars to create an application, then sell it to individual users or huge enterprises.

Selling to consumers was a good business. But selling to enterprises, the way Microsoft, SAP, and Oracle did, was a great business. From the standpoint of profitability, selling packaged software to big corporations might be the greatest business in history. You built software once and incurred practically no incremental cost for each unit sold. Companies weren’t using all this software to deliver better experiences to customers or differentiate themselves in the market. They just used software to run their internal operations—accounting, enterprise resource planning, and the like.

The Second Era of Software—Software as a Service (SaaS)—began, about twenty years ago. The company that pioneered this model is Salesforce. Its founder and CEO, Marc Benioff launched Salesforce in 1999 with the slogan “The End of Software.”

Of course, it wasn’t the end of software—it was just a new way of delivering software.

Over time, SaaS companies sprang up to serve every line-of-business owner. You paid based on the number of employees who were using the software. You didn’t have to worry about data centers or per-CPU licenses anymore. Many products were so inexpensive to get started that a small team could just put it on a credit card and expense it.

The model also came to be known as cloud computing, which became possible because of high-speed Internet connections and what’s called “multi-tenant” software. In cloud computing, you no longer needed to run your own data centers. And individual employees didn’t need to run local versions of a program on their PCs. They could just do everything they needed to do via a web browser. That made life easier in all sorts of ways. If a software program had a bug and needed to be updated, or if the software vendor released a new version of the app silently, customers didn’t need to send IT guys to everyone’s desk and install the new version. Those fixes and upgrades just happened—out in the cloud. To the user, this was all invisible.

Another change involved the business model — Instead of paying to license a program based on how many servers you deployed—including a big initial payment upfront and then paying annual maintenance fees—you just subscribed. When you stopped needing the software, you ended your subscription.

In short, Software-as-a-Service describes software deployed in the cloud and billed on a subscription basis. Compared to traditional on-premise software, Software-as-a-Service provides customers with several benefits, notably:

SaaS eliminates the need to procure and manage hardware.

SaaS is accessible with little more than a credit card and laptop.

SaaS requires minimal maintenance, with vendors responsible for updates and upgrades.

SaaS is subscription-based, with low upfront costs, an operating expense instead of a capital expense.

SaaS is easy to use with minimal training, similar to consumer software.

SaaS works on any computer or mobile device, which is ideal for remote work.

Third Great Era of Software—The Cloud Era — Cloud computing is perhaps the most important enabling technology behind SaaS companies. Before cloud computing became widely available, internet software companies had to be experts in building and running data centers, increasing the cost, complexity, and difficulty of scaling an internet software company significantly.

Introduced in the mid-2000s, cloud computing—specifically Infrastructure-as-a-Service—made it possible to rent computing resources instead of buying them. Cloud computing providers like Amazon Web Services (AWS) leveraged their scale to lower costs, increase reliability, and scale compute, storage, and other functions on-demand. Over time, cloud computing eliminated the need for software companies to procure and manage hardware.

Amazon was one of the pioneers of the cloud delivery model. In the mid-2000s its infrastructure was struggling to keep pace with its rapid growth. At the time, Amazon was building dedicated IT resources for each project. It moved away from this inefficient structure to a services model where IT was pooled as common infrastructure and made available to anyone in the firm as needed. Several years later, Amazon opened its infrastructure up to external parties. It launched its first AWS product, Amazon Elastic Compute Cloud, in 2006. This ushered in a new era of IT, where resources no longer needed to be built from scratch and could instead be accessed on-demand over the internet.

AWS has turned IT infrastructure into an operating cost. Rather than building out expensive data centers and investing ahead of growth, start-ups can rent computer power on an as-needed basis. Steve Blank, the founder of the lean start-up movement, has said that the founding of AWS was as important for Silicon Valley as the introduction of venture capital. Indeed, the costs of starting a new internet company have fallen by several orders of magnitude since AWS was launched.

In the digital economy, the cloud-infrastructure platforms are helping to level the playing field between the largest and smallest. They are enabling companies of any size to easily and affordably access the tools they need to run their businesses online. They are lowering the costs of starting and scaling a business and increasing the vitality of the economy.

The power of AWS stems from the fact that its users benefit from the collective scale of all the customers on the platform. AWS can invest more in the development and management of the service than any single customer can do on their own.

AWS builds scale on behalf of its customers. This means that smaller companies are no longer at a disadvantage when accessing computer resources. Hemant Taneja in his wonderful book, Unscaled called this process ‘unscaling’. An apt name for the driving platforms might be ‘Scale as a Service provider’.

IT infrastructure is just one operational area that is moving to a cloud delivery model. Similar shifts are underway in other sectors such as e-commerce, payments, and communications. Shopify, Stripe, and Twilio are three of the most prominent examples of ‘scale as a service’ platforms in these sectors.

AWS owns the underlying infrastructure. The other platforms sit on top of networks of third-party infrastructure. All together are like operating systems. They use software to remove complexity and make it easier to manage and consume the underlying services. There are parallels with the electricity grid, except the grid is the internet and the ‘electricity’ is represented by the digital transformation tools. All that entrepreneurs need to plug into this ‘grid’ are a computer and an internet connection. Once connected, they gain access at the touch of a button to powerful tools that would previously have required significant up-front time and investment.

This business model—The Platform Business Model—represents the next big thing in software.

The way we bank is fundamentally changing.

“There is a tide in the affairs of men, Which taken at the flood, leads on to fortune... On such a full sea are we now afloat. And we must take the current when it serves, Or lose our ventures.”

— William Shakespeare

Fundamentally the biggest shift in banking is that “banking is no longer somewhere you go, it’s something you do”. Executives ‘who take the tide at the flood’ and anticipate the value shift will be best positioned to seize tomorrow.

Think about your bank. It probably offers the same things that every other bank offers. Checking account, savings account—it’s a fiercely competitive business. So what differentiates one bank from another? It used to be about the experience inside the bank branch. What did it look like? Was it recently remodeled? Were the employees well dressed and friendly? But now, you don’t walk into a branch, you open an app. So banks need different skills—software skills. And they can’t just buy all this software from a vendor. To be sure, no shortage of companies will claim to sell the software that banks need to perform a digital transformation. But if all the banks just bought the same bank software, they’d all be undifferentiated again. So ultimately, they have to listen to customers’ needs and answer those needs with software by learning and iterating quickly.

Reasoning from first principles allows us to step outside of history and conventional wisdom and see what is possible. When you understand the principles at work, you can decide if the existing methods make sense. Often they don’t.

The idea of building knowledge from first principles has a long tradition in philosophy. The Western canon goes back to Plato and Socrates, with significant contributions from Aristotle and Descartes. Essentially, they were looking for the foundational knowledge that would not change and that we could build everything else on, from our ethical systems to our social structures.

Ask yourself a couple of simple questions. If you were starting from scratch today, building a banking, monetary, and financial system for the world, a banking system for a single country or geography, or just designing a bank account from scratch, would you build it the same way it has evolved today? Would you start with physical bank branches, insist on physical currency on paper or polymers, signatures on application forms, passbooks, plastic cards, checkbooks, and the need to rock up with multiple different pieces of paper and IDs for a mortgage?

If you were starting from scratch with all the technologies and capabilities we have today, you would design something very, very different in respect to how banking would fit into people’s lives.

The banking system we have today is a direct descendant of banking from the Middle Ages. The Medici family in Florence, Italy, arguably created the formal structure of the bank that we still retain today, after many developments. The paper currency we have today is an iteration of coins used before the first century. Today’s payments networks are iterations of the 12th-century European network of the Knights Templar, which used to securely move money around for banks, royalty, and wealthy aristocrats of the period. The debit cards we have today have been iterations of the bank passbook that you might have owned if you had had a bank account in the year 1850.

When web and mobile came along, we simply took products and concepts from the branch-based system of distribution and iterated them to fit onto those new channels. Instead of asking whether we need an application form in the online process at all, we just built web pages to duplicate the process we had in the branch.

Businesses want to think in terms of categories. Consumers want businesses to think in terms of their needs. Banks have traditionally provided three core pieces of utility:

A Value Store—The ability to store money safely (investments fall into this category)

Money Movement—The ability to move your money safely

Access to Credit—The ability to loan money when you need it

Since the emergence of banking during the 14th century, banks have taken that core utility and added structure. Initially, this structure was about network—where you could bank. Banks then added structure around the business of banking, trust, and identity—who could bank, what was a bank and how you had to bank. Today, consumers fight through more friction than ever before just to get to that underlying utility.

Technology now affords us the ability to radically eliminate that friction and create banking embedded in the world around us, delivering banking when and where we need it the most. This is called “Semantic Banking” — The semantic web today is all around us. It is immersive, ubiquitous, informed, and contextual. The semantic bank will have these features, too. It will prompt us with the things we need, and warn us against doing things that will damage our financial health. It will be personalized, proactive, predictive, cognitive, and contextual. We will never need to call the bank, as the semantic bank is always with us, non-stop and in real-time. As a result, nearly every bank function we think about today—paying, checking, reconciling, searching—goes away as the semantic bank and web do all of this for us. We just live our lives, with our embedded financial advisor and the core utility of banking as an extension to our digital lives.

When it comes to this new augmented world, banks are significantly disadvantaged over the real owners of utility, and they must constantly jostle for a seat at the new table. The utility today isn’t via a branch or an ATM, but the smartphone, the IP layer, data, interfaces, and AI.

Everything happening in the market is converging to impact Financial Institutions:

Customers are Changing—Customers are becoming more demanding as their needs evolve and competitors raise the bar with new services. Traditional financial products are not sufficient and are failing to evolve.

Competitors are Evolving—Big tech has secured a foothold in the market and fintech is carving out new segments (and dominating them).

Tech Costs are Rising—The compounding costs of building new layers of tech on top of yesterday's infrastructure are no longer sustainable.

Disruption is not new. When you look back over the last couple of centuries, you see time and again evidence that incumbents underestimated the impact of change on their industry.

Today, the huge potential changes we’re facing are no longer just focused on front-end user experiences in the banking sector. We’re seeing currency, capital markets, wealth management, bank licenses, labor force, and economics all under attack from new emerging systems, paradigms, and technologies.

In an age where technology has changed how we interact, both with one another and service providers, businesses not embracing this change will be left behind —, particularly in financial services. Perceived as a threat for most incumbents, these outside influences can also be an incentive to change, the opportunity to redefine financial services for consumers, and themselves.

Incumbents need to internalize the words of J. K. Rowling, —“we do not need magic to transform our world. We carry all the power we need inside ourselves already. We have the power to imagine better.” Transforming the core business can magnify an incumbent’s strategic advantages over digital newcomers in terms of people, brand, existing customers, and scale. Financial institutions that view tech as a competitive advantage will win over companies that view tech as a “cost”. Investments in certain technologies do confer a competitive edge—one that has to be constantly renewed, as rivals don’t merely match your moves but use technology to develop more potent ones and leapfrog over you.

According to Salesforce, “Digital transformation” is the process of using digital technologies to create new—or modify existing—business processes, culture, and customer experiences to meet changing business and market requirements.

Digital transformation is the successor to digitization.

Digitization helped companies move their workflows from pen and paper to computers and software. This improved productivity without transforming business models. ATMs replaced some bank tellers, for example, but still dispensed cash.

With the internet at its core, digital transformation has been and is more profound.

With mobile wallets and apps, consumers do not need physical cash to pay for goods and services. Likewise, businesses can leverage mobile apps to improve customer loyalty, perform real-time analytics, and issue digital receipts. As a result, challenger banks can acquire customers through app downloads instead of bank branches, a change much more disruptive than digitization.

The digitization of banking is now mainstream, and all bank capabilities will be packaged as digital structures whereby products will be apps, processes will be APIs, and retailing will be contextual, delivered through mobile Internet at the point of relevance.

Those who think digital networks are just layered on top of old infrastructures, networks, distribution strategies, and organizations are wrong. Believing this is precisely why banks have ended up with silo structures, painful processes, and inappropriate skills.

Banking software is still stuck in the stone ages. Bank operations today are a cacophony of 10+ software vendors providing disconnected monolithic software for Core Banking, Debit Processing, Credit Processing, Prepaid Processing, Loan Origination, Loan Management, Fraud Management, Mobile apps, Net Banking, Customer Lifecycle Management and more. While the software is busy eating the world, most banks stagnate on decades-old technology built at a time when Mainframes, Cobol, and Batch-processing were in vogue.

Banks were ‘built to last’ but today they need to be built to change. Changing regulations, customer demands, and margins being squeezed by maintenance costs and challengers have made it evident that this is not the time for indecision.

The increased pace of change requires a new architecture.

Most banks, with few exceptions, run on aging IT infrastructure that was deployed in the 1980-the 90s and have been built on monologic architecture (single/bundled software application where database, user interface, and server applications are managed in one place), mainly built for the industrial age. Such infrastructure was mostly vertically integrated architecture with a value chain deriving from proprietary products -and allowing banks for more controls over all their systems. Thus, banks had their systems locked into proprietary internal and legacy structures, and their customers too (via mediocre digital experiences).

Financial institutions without a modern digital platform will find it hard to remain competitive. Banks need to evolve from the vertically integrated legacy technology stack they are using today and opt for more open, interoperable, and scalable architectures. They need to recall the words of Vincent van Gogh:

“Do not quench your inspiration and your imagination; do not become the slave of your model.”

Imagination is the source of disruption. Technology makes it feasible, and an ecosystem of connectivity makes it viable as a business. Rebuilding with a new tech architecture unlocks new fundamentals to an increased pace of change. Often incumbents lift and shift their old code and infrastructure to the cloud. This may cost more, be less reliable, and doesn’t improve speed. As a result, most incumbents have not yet fully embraced cloud infrastructure. To get the benefits there are three fundamentals:

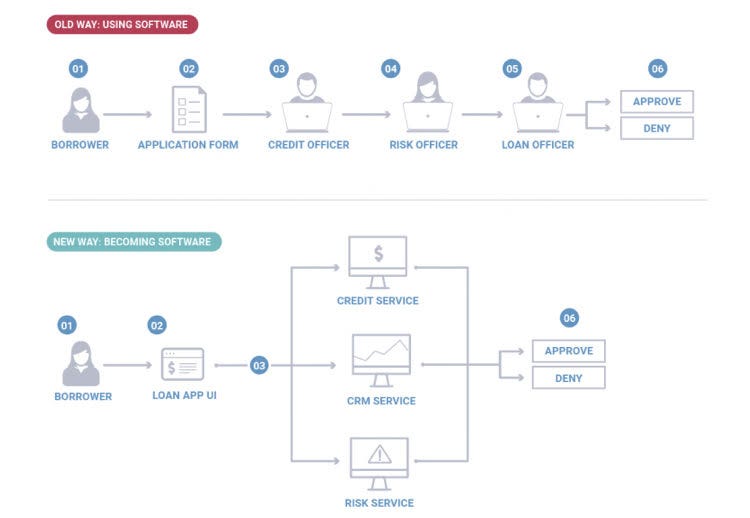

Breaking Monoliths into Primitives reduces the size of services, reduces the size of every change, and reduces the cost and risk of each change. Monoliths are unwieldy assortments of systems, tech, and processes that are difficult to manage and slow to change. Alternative to monoliths, primitives are small, modular components that can easily be used to build any product. In software engineering, a primitive is a basic interface or segment of code that can be combined with others to make more complex programs. Examples of primitives include— storing value, moving value, exchanging value, debiting, crediting, KYC. When primitives are re-assembled in new combinations, any financial product can be constructed (and perhaps more importantly, new innovative products too). By building from primitives, each mission team has the building blocks to solve customer problems faster without having to worry about governance or overhead from other parts of the organization. The smaller the primitive, the more ways it can be re-combined to create new products.

Shifting Silos into Horizontals maximizes the re-use of capabilities (like digital onboarding), reducing the complexity of all changes. Silos are the business units that form when operations are built around products and geographies, leading to duplication of each capability. The alternative to silos, horizontals center operations around modular capabilities that can then be used to build and manage products. Instead of building each functionality multiple times for different use cases, build each one once, in a way that means they can be used for all relevant products and customer contexts. Rebuilding each capability as its layer removes silos. This requires an architecture that is capable of bringing together all of these primitives. When combined with modern techniques like DevOps and automated testing this architecture enables re-use of capabilities, more innovation, and faster change.

Moving from Whale Vendors to the School of Fish Providers leverages new specialist providers that have turned cost centers into best-in-class operations. Whale vendors are large, traditional vendors that are often inflexible and difficult to change. The alternative to whale vendors, school of fish providers, is an assortment of specialist providers that offer flexibility and are easy to integrate with.

To increase the pace of change, incumbents must make more use of smaller, best-in-class providers.

Meet Intellect Design Arena — A Global Fintech Product Powerhouse — Enable Banks to become Digital Leaders, and help them ‘disrupt the disruptors’

Intellect Design Arena creates a full spectrum of financial technology software for banking, insurance, and other financial services — built on the principles of Design Thinking, which is the key differentiator amongst its peers in the FinTech industry. Intellect has built the world’s only Design Center for financial services.

With a singular focus on products. It addresses the needs of financial institutions at varying stages of technology adoption. It offers a suite of vertical and integrated products that enable financial institutions to act as the principal service provider to their customers.

Intellect operates in over 97 countries—across continents, with 60% of business coming from advanced markets.

Ralph Waldo Emerson once said, “what lies behind you, and what lies in front of you, pales in comparison to what lies inside of you.” Financial institutions utilize Intellect Design Arena for not just digital transformation initiatives but to be “truly digital”—moving beyond digitization, to building products and services with digital capabilities at their core across global consumer banking, central banking, global transaction banking, insurance, and risk, treasury, and markets. To be truly digital is to be able to offer real-time, relevant, highly customized experiences.

Don’t mine gold when you can sell shovels!

In the as-a-service economy, everything is a shovel. When every function in the value chain can be modularized and provided as-a-service, it doesn’t take a genius to figure that while everyone joins the digital transformation ‘gold rush’, the vast majority of value will accrue to the ones selling the shovels.

Intellect sells contextual and composable picks and shovels to enable financial institutions’ new gold rush.

Intellect provides mission-critical products, solutions, and platforms — aligning with the five key business needs of financial institutions:

Revenue Accelerators — that would help them spring back to the growth path.

Transformation Accelerator — would help accelerate the bank's digital transformation while reducing the risk of a rip & replacement.

Risk Mitigation — that would help assess and manage risk while pursuing larger business opportunities.

Customer Self-Service — that would eliminate the limitations on in-person services and bring more customers to digital channels.

Cost Reduction and Operational Efficiency — that would ensure Straight-Through-Processing and eliminate waste within processing cycles.

Intellect offerings are through its four lines of businesses – Global Consumer Banking, Global Transaction Banking, Risk, Treasury and Markets, and Insurance.

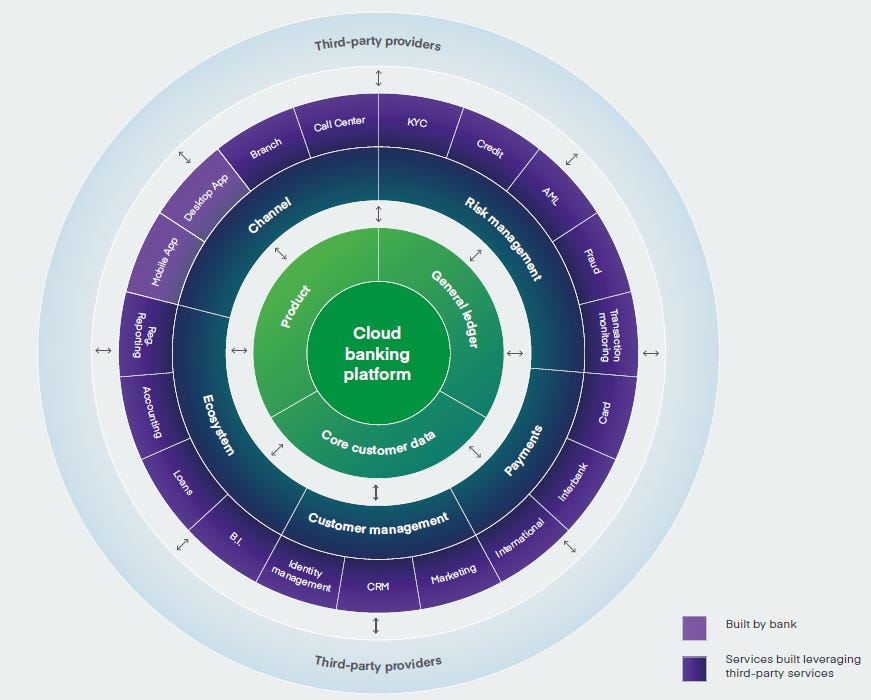

Before we go into each vertical, let’s start with Intellect’s Cloud Transformation Accelerator Platform—iTurmeric, on which many of their products are built.

In a world where technology is continuously disrupting workforces, customer expectations, and even entire industries, the ability to modernize quickly and cost-effectively has become imperative. The evolution of technology has made the competition more aggressive for financial institutions across the world. They are still saddled with legacy platforms and are increasingly feeling the pressure to accelerate their digital transformation. Many financial institutions face the challenge of aging, legacy infrastructure that is hard to maintain, yet expensive and risky to replace.

iTurmeric FinCloud challenges software implementation paradigms and infuses the traditionally cumbersome process with progility (progressive + agile), vital for financial institutions in this new era of banking technology — Build new to replace the old and progressively change systems instead of going big bang. This means embracing cloud and taking a composable approach with partners who specialize (instead of one-size-fits-all), giving the business agility and control. A gradual transition where individual systems are targeted and changed in a surgical approach allows a controlled change. A new technology stack is built for business units giving them enhanced functionality and interoperability with current systems.

iTurmeric helps accelerate a bank's cloud journey and promotes collaboration with partners and customers to build new and innovative solutions — a seamless integration across the bank’s ecosystem.

Today, even the simplest banking service involves a complex orchestration of core systems, transaction processing, decisioning, reporting, analytics, authentication, security, and beyond. Instead of locking these functions together for dedicated applications and workflows, composable banking separates the functions so they can be combined and recombined in new ways to deliver new services and customer experiences — Composable banking is an approach to the design and delivery of financial services based on the rapid and flexible assembly of independent, best-for-purpose systems. It helps banks create modern customer experiences to compete in the fintech era — and constantly evolve them to respond to change.

With iTurmeric FinCloud, the systems of the new digital banks can be tested and run in isolation or in parallel with core legacy systems, which can, in turn, continue to run without interruption or compromise. The discrete nature of these APIs means that newer systems can be put in place without impacting mission-critical legacy infrastructure.

Contrary to how the industry has operated for decades, the iTurmeric platform allows institutions to mitigate risks, test models and strategies, and implement them in a controlled environment.

In short, iTurmeric FinCloud, with its first-of-its-kind enterprise integration, API-first architecture, cloud-native, microservices-based platform, enables banks to progressively modernize and participate in the experience economy, without the risk of rip and replacement. The aim is to build and test a new bank to determine the best way forward, then migrate from old to new in less time, with low risk and easily configurable to changing market dynamics. This allows businesses to optimize for what matters: growth to some, profit margins to others, innovation for others.

Corporate Banking

iGTB — the Corporate Banking Solution arm of Intellect offers the world’s first complete global transaction banking platform. It is the largest business unit of intellect in terms of revenue and is the most established offerings given its strong market acceptance, brand positioning, customers, and potential cross-sell opportunity.

Key product offerings under iGTB are:

Contextual Banking Exchange (CBX)

CBX, a Digital Banking Platform for Cash Management, enables banks to become more ‘business aware’ and contextual by providing actionable insights, foresight, and oversight towards their clients: SMBs, SMEs, and larger corporates. Through the use of AI, Machine Learning, and Predictive Analytics it anticipates events and translates them to actions or recommendations to a corporate treasurer or CFO, through context-aware informed interaction and decision making.

The platform is abstracted as a set of large-scale distributed services, developer-friendly APIs, and fully componentized UIs that provide developers with a production-ready application container runtime environment with fully automated service deployments. This gives the option to leverage the platform head-less or through customizable pre-built UI components covering the full spectrum of corporate banking — Payments, Liquidity Management, Virtual Account Management, Collections, Receivables, Escrow, and Cashflow Forecasting.

This enables banks to accelerate customer self-service and both up-sell and cross-sells their services by providing clients with context-aware recommendations on the best next action or best-next offer needed to meet their objectives. This helps the banks become an integral part of the corporate value chain and build ecosystems around them. It further equips the bank to anticipate its clients' financial needs better, leveraging all the data at its disposal to position itself as a trusted advisor.

Digital Transaction Banking (DTB)

DTB is an integrated platform that prepares transaction banks to provide for every client and every sector’s needs, with a configurable and intelligent platform. It encompasses every aspect of transaction banking, covering the working capital cycle from accounts services, payments, and liquidity management to collections & receivables, virtual accounts, trade finance, and supply chain finance.

With DTB, transaction banks can successfully optimize capital, and maximize ROA and fee income. It can also improve product cross-sell & distribution channel effectiveness, support SME franchise and growth sectors (through working capital provisioning and advisory services) and ensure full regulatory compliance for the large to very large corporates and MNCs.

Payments Services Hub (PSH)

PSH offers advanced cash management for corporate banking through the loosely-coupled, workflow-connected channel aggregation and orchestration, end-to-end payment processing, and format conversion on a digital portal. Leveraging the power of context, PSH enables routing of payments through the best possible rails based on customer preferences, preset parameters, and a host of other contextual cues.

With Payments Services Hub, banks can consolidate multiple channels such as internet banking, mobile banking, corporate portals, social media, etc. through a single integration layer. In addition, they can implement and realize new services swiftly. The solution powers banks to aggregate data from multiple sources and route them to the appropriate CSM (Clearing and Settlement Mechanism). It allows banks to enjoy the power of analytics, transparency, ease of tracking, enhanced operational efficiency, and reduced operating costs. The solution by itself is a scalable, flexible integration layer capable of handling ever-increasing volumes. Operationally, it enables easy onboarding and support for multiple formats, minimizing processing costs for bank customers.

Liquidity Management Solution (LMS)

Intellect's Liquidity solution is a market leader in corporate liquidity management and has been implemented at leading global banks. It is a comprehensive product that includes product processors for sweeping, notional pooling, inter-company loans, as well as real-time fund check and investment sweeps. It also has a world-class digital front-end that delivers a faster, simpler, and seamless experience to the customer.

Apart from standard features such as physical cash concentration and notional pooling, single country and cross-border sweeps, single or multi-currency structures, and others, Intellect’s Liquidity solution also delivers investment sweeps, interest reallocation hub, and overdraft limit reporting. As the market-leading Liquidity application, it also offers N-levels of sweep accounts, automated investment sweeps into money-market funds, automated reverse sweeps, geographic specialization (including Entrust loans), and multiple interest allocation models in its off-the-shelf product.

Trade and Supply Chain Finance (TSC)

Trade and Supply Chain Finance is the first and only integrated platform that enables banks and clients to carry out all trade and supply chain operations from a single place, with integrated limit management. This solution facilitates buyers, who are also sellers, to carry out both operations through a unified interface with ease. It delivers smart contextual solutions that are designed to contain cost, reduce risk and increase overall competitiveness.

Retail Banking

iGCB — the Retail and Central Banking Solutions arm of Intellect, offers an end-to-end Contextual Banking suite for retail and corporate banking across Core, Lending, Cards, Wealth, and Central Banking.

Intellect Digital Core (IDC)

Distilled to its essence, a core banking system is the software used to support a bank’s most common transactions from daily banking to lending and interacts with accounting and reporting systems. These core capabilities that drive all banking services and processes can be identified, optimized, and integrated.

Intellect Digital Core’s flagship Core Banking platform is a fully integrated solution across Core, Lending, Treasury, Trade Finance, and Cards.

IDC presents banks with the best of both worlds, i.e. Customer Experience (Digital ‘Outside’ or front-end) and Operational Efficiency (Digital ‘Inside’ or backend).

The target market is from Digital Challenger Banks (new format Banks that operate only in the Digital space), Banks that seek to modernize their Back end platforms that were set up over two decades ago, new Bank licensees, and Banks that set out on a progressive modernization initiative of renovating their technology architecture.

Digital Lending

Intellect Digital Lending is designed on the ‘Instant and More’ principle. It aims to deliver a superior customer experience with in-principle loan approval in 2 minutes and operational efficiency with over 99% Straight-Through Processing (STP). The product encompasses a comprehensive Loan Life Cycle Management System that provides end-to-end solutions. It addresses the bank’s business objectives from origination, servicing, and managing to collections.

Intellect’s lending solution is designed to drive digital transformation in the lending business and spans across Retail, Corporate, SME, and unbanked segments. With its modular yet integrated product offerings in the lending space, Intellect offers Credit Origination (COS), Loan Management and Servicing (LMS), Collateral and Limits Management (CLMS), and Debt Management, either as a bundled Lending suite or specific point solutions.

Digital Cards

Intellect Digital Cards is a comprehensive, fully digital payment solution that offers an end-to-end solution from card origination, management, loyalty, and fraud management to collections. The system is also equipped with a self-service mobile app for a real-time experience for the end customers. The six pillars of the comprehensive solution are multiple lines of credit on a single account, transaction-level pricing with hierarchical management, integrated, configurable installment module, flexible loyalty module, real-time fraud management system, and customer self-service app.

Banks and retail businesses prefer a one-stop solution for cards as it would be convenient as against having to manage multiple vendors for a different line of credit. Intellect Digital Cards is designed to deliver a platform that runs multiple lines of credit on a single account with a single account and billing. The solution is available in both license and cloud models with support for private and public cloud options.

Enhanced to manage e-Wallet capabilities, the product is also being offered as a Platform as a Service (PaaS) model with revenues accruing on a per transaction basis. Banks, financial and retail institutions can also choose to avail support for managing back-end operations from Intellect, thus getting cost advantage and quick-to-market solutions.

Wealth Qube (Digital Wealth)

Intellect WealthQube is a state-of-the-art, relationship-centric, one-stop digital wealth management solution. It enables straight-through processing of a variety of investment products from front to back office for in multiple markets. The solution is built for Private Banks, Retail Banks, Wealth Managers, Asset Management firms, Advisory firms, Broker-Dealers, Trusts, and IFAs to service client segments across HNI, Mass Affluent individuals, and institutions. This platform is built on a design framework of 6 Offices (Functional Units), 23 Desks (Functions), and 130+ tools. It is API-based, scalable, Omnichannel, and has modern UI (User Interface) providing a superior user experience.

Intellect Wealth Qube supports hybrid wealth management services and intends to deliver 20-20 Advantage i.e. 20% increase in RM (Relationship Manager) productivity and a 20% increase in revenue. Apart from this, customers across various markets leverage Wealth Qube to harness the advantage of Digital-first experience and reduced Total Cost of Ownership (TCO). One of the key features that this solution offers to its users is Contextualised analytics that powers business expansion and performance through actionable insights.

Central Banking

As a Banker to the Government, a Banker to Banks, a Government Debt Manager, a Currency Manager, and the overall Supervisor & Regulator of the country, Central Banks have to deal with high levels of complexity. Intellect Quantum Central Banking Solution is designed specifically for Central Banks, aimed at reducing complexity. It is built on an underlying technology design, driven by four parameters - real-time informed decision-making & risk management, unmatched configurability for speed and ease of change, tightly integrated analytics, and uncompromising security.

Intellect's Quantum solution provides a comprehensive platform for Central Banks with a flexible choice of instruments. It empowers them with faster decisions and timely intervention with the help of 360-degree dashboard views, on-demand financial statements, and reports, and real-time risk monitoring. It empowers Central Banks to progressively modernize and transform through a formidable range of instruments including currency chest management, public debt & depository management, enterprise general ledger & collateral management.

Risk, Treasury & Capital Markets

iRTM, the Treasury and Capital Markets solution arm of Intellect, offers a comprehensive suite of products to address the requirements of banks and capital markets. iRTM’s comprehensive suite of solutions addresses the requirements in treasury, liquidity risk, and capital markets domain.

Capital Cube (Treasury and ALM)

Capital Cube is an Integrated Treasury & Asset and Liability Management (ALM) solution, that aids the treasurer to strategically manage the balance sheet, adapt to regulatory regimes, optimize liquidity, and leverage risk to maximize profits for the bank. The solution provides updated information on liquidity, funding, and exposures. It also assures solvency, protects margins by an accurate view of asset and liability positions, effective hedging and performance attributions, and provides greater visibility and control to the treasury.

Capital Cube enables greater strategic planning and execution by bringing together the six key business levers for today’s treasury: Integrated front, Mid & Back Office treasury, ALM, Capital Adequacy, CBX-FX, Risk Management, and Analytics.

Capital Alpha (Brokerage Solution)

Capital Alpha is a multi-asset, multi-exchange, multi-channel, multi-currency, multi-lingual integrated front-to-back solution. Capital Alpha is the quintessential ‘Broker-in-a-Box’ solution that provides Omnichannel trading experience through contextual research and analytics. It also ensures compliance through real-time and integrated pre-and post-trade risk management.

Capital Alpha is Intellect’s solution for Capital Markets that combines the functionalities of the front, mid, and back-office of retail and enterprise broker houses, and offers the combined benefit of speed, leverage, risk management, and analytics. The product integrates with and supports other Capital Market functionaries such as Custodians, Registrar and Transfer agents, and Mutual Fund participants.

Capital Sigma (Asset Servicing)

Intellect’s Asset Servicing solution suite helps achieve 95%+ Straight-Through-Processing and increases operational efficiency by digitizing Custody, Fund Services, and Investor Services functions. It can coexist with the current ecosystem in an enterprise. Ready-made adapters are available through API-based Capital Market Interface Exchange that can connect to market interfaces in multiple regions/countries and ensure seamless implementation. The solution experience is further enriched by a multifaceted Client Portal, providing a transparent view of the post-trade lifecycle and additional self-help tools.

Insurance

Intellect SEEC, the insurtech arm of Intellect, is tackling the biggest challenges for insurance with contemporary technologies like Big Data, AI, and ML. Intellect SEEC addresses the Digital and Data needs of the Insurance carriers both through products and by offering Data as a Service.

Intellect’s insurance division has built many robust applications to serve property and casualty insurance sectors. One of them is Intellect Xponent — a cloud-native underwriting platform.

Intellect Xponent is a complete underwriting workstation for managing complex commercial specialty risks. This highly configurable solution utilizes big data and risks analysis frameworks to deliver intelligent insurance workflows that facilitate risk analysis, underwriting, policy life cycle management, and more. It provides insurance carriers the ability to consume submitted data with no manual effort, enrich risk data from both structured and unstructured data sources and orchestrate intelligent decisions.

Harnessing the latest exponential technologies to Insurance, Xponent provides underwriters with an efficient way to assess risk impact. It offers a faster and seamless experience for agents to retrieve application status and a quick turnaround time for customers. The solution also incorporates cognitive process automation and voice and text-based human-machine interactions.

Many insurance carriers are utilizing Intellect Xponent to streamline their underwriting processes. Intellect’s customers implement Xponent because it allows them to leapfrog technologies and adopt a cloud-native system that can be configured and deployed in a short period. It also provides them an edge of precision in their underwriting processes.

In a digital-first world, industry-specific AI is required to keep up and adapt.

Leveraging the power of Intellect Fabric — a component of Intellect’s reference architecture, powered by Artificial Intelligence and Machine Learning, drives “Intelligent Hive” — This solution feeds contextual intelligence to financial institutions, using both structured and unstructured data. It is the perfect blend of domain awareness and data — helping financial institutions build ‘contextuality’ in their customer interactions, sharpen their offerings and maximize strike rates. It also helps to quickly build applications that leverage Big Data and Machine Learning in a cloud-native environment.

Intellect's Fabric Data services function as a Data refinery — aggregating data from multiple sources, triangulating them to address data veracity, and feeding them to consuming applications.

Intelligent Data Exchange (IDX) platform combines the functionalities of data upload, validation, and contextual enrichment that collectively delivers highly accurate input data, eliminating several steps of human intervention, correction, and data input. Powered by AI and ML, it is suitable for automatic uptake of forms, contextual scanning of documents, and similar applications which aim at converting unstructured/semi-structured manual data to structured information.

These apart, Intellect offers full-spectrum Digital e-Governance solutions for public sector services through its iGov business arm.

Intellect operates the Government eMarketplace portal (GeM) as a Managed Service provider along with consortium partners and earns a fee based on the transaction value — Transaction-based revenue model, linked to procurement value on Government e-Marketplace; higher procurement, higher revenue. This portal is set to scale much higher Gross Merchandise Value (GMV) values in subsequent financial years, as more State Governments, Departments and Public Sector Enterprises are onboarded and commence transacting on the portal. Central Government’s commitment is to make the Government e-Marketplace a single-point sourcing platform with targeted Gross Merchandise Value (GMV) over Rs. 1 lakh crores.

Over the years, Intellect has invested strategically and built meticulously to achieve a unique, future-proof tech stack that is contextual, microservices-based, API-first, and cloud-ready, powered by AI and ML. Supported by a revolutionary integration technology iTurmeric, the first-of-its-kind enterprise integration, cloud-native platform based on API first architecture, enables banks to progressively modernize while ensuring business continuity without the risk of rip and replacement.

What is the role of platform APIs?

An API is a programmable interface to access platform functionality. APIs serve platforms externally by allowing managed and controlled access. Internally, APIs can be used to connect services or applications and control access to data or services resulting in extremely clear and clean system architecture.

These technical interfaces standardize access to an organization’s assets (data and services). APIs lead to a liberation of access to data and services. In the coming years, every organization will need an API strategy and access to assets via APIs, just like every organization has a website strategy to allow access to its information.

The better these APIs are designed and documented, the more effectively the platform infrastructure can be accessed and leveraged. Because of that, it can be customized by outside developers—users—and in that way, adapted to innumerable needs and niches that the original developers of the platform could not have imagined.

Now, that you have got some idea of Intellect offerings, let’s turn our eye to how they add value.

Adam Brandenburger and Harborne Stuart, professors of strategy, offer a very concrete and sound definition of how a firm adds value. Their equation is simple:

Value Created = Willingness-to-Pay – Opportunity Cost The equation says that the value a company creates is the difference between what it gets for its product or service and what it costs to produce that product (including the opportunity cost of capital).

Archimedes said: “Give me a lever long enough and a fulcrum on which to place it, and I shall move the world.” I don’t know about the long lever, but Intellect does have multiple levers and a fulcrum.

Levers of Monetization

Intellect generates revenues in the following streams:

License fee paid by customers for use of their software products in an on-premise model. License realization increases – both as a per-deal figure and as a share of total revenue with an increasing share of advanced markets in the total revenue pie and greater maturity of products in meeting the RFP (request for proposal) requirements.

Customers' implementation and customization fees for rolling out software products and customizing them to their specific requirements. Intellect offers ongoing production support to customers in various flavors – deployment of dedicated teams, technology management services, business growth support, ongoing customization, and change requests – to keep pace with the innovations of customers, all of which contribute to implementation revenues.

Annual Maintenance fee paid for maintaining the software and making upgrades available, where applicable. A higher license revenue-earning also has a downstream impact on higher AMC revenues, which are often a percentage of the license component. AMC revenues are further bolstered by the increasing footprint of implementations.

Subscription fees (SaaS) for use of software on hosted model or cloud deployment. In addition, SaaS revenues have a potential upside where they have been linked to the business metrics of customers, such as quantum of transactions, number of accounts/customers, or revenue numbers.

With an accelerated shift of industry towards the public cloud model, Software-as-a-Service has become the preferred operating model for software companies due to the following reasons:

Leveraging the public cloud, SaaS companies can serve software to customers who do not have to build out their own data centers.

All customers use the same software, lowering the cost and complexity typically associated with multiple versions and operating environments.

Subscriptions generate predictable, recurring revenue with automatic renewals, conferring higher valuations on SaaS stocks than on traditional software stocks.

SaaS software vendors own their customer relationships and, with full insight into usage patterns and payments, can upsell and cross-sell other products more effectively.

The Software-as-a-Service model is a win for all stakeholders—developers, customers, and investors. As such, over time, the vast majority of software revenue will be recurring. While not a new model, the rapid growth of the public cloud as a computing platform and the push for digital transformation have created a SaaS market much larger and sooner than most had expected.

Intellect is also looking to collaborate with the fintech ecosystem by establishing and participating in API-led Fintech Marketplaces, which would open another stream of revenue. It is also looking to sell a component of its platform as a standalone product by taking smaller software pieces and creating an independent go-to-market strategy for them. Since there are no product development costs — it will be a high-margin business. This is expected to help cater to companies outside its core banking, financial services, and insurance (BFSI) space.

Now, let’s see what drives the cost.

Drivers of Cost

Product Manufacturing – Development of products, building next versions of current products and adding user journeys, technology re-platforming.

Research & Engineering – Costs in building core technology components/frameworks/architectures and tools.

Service Delivery – Implementation costs in delivering the products to customers (roll-out costs) and offering production support/maintenance costs.

Sales & Marketing – Business development, branding, market development, marketing, and pre-sales costs.

General Administration Costs – Costs of infrastructure, shared and support services including corporate management.

The heart of the power of Intellect’s business model is: Value Increases Exponentially — Costs increase Linearly.

Intellect began as part of Polaris Consulting Services, which handled software development and back-end operations for the American bank - Citibank. In 2014 Polaris Consulting Services demerged itself into two new entities: a services company and a product company focused on software as a service (SaaS) and enterprise products for banking and insurance, which became Intellect Design Arena.

Post its de-merger from Polaris, Intellect spent the first three years of its journey post listing in

Investing in its Products - enriching their functionality and architecture.

Investing in Sales & Marketing - brand building, enlisting analyst endorsements, and gaining market acceptance - apart from hiring leaders who brought relationships.

Expanding its Footprint - winning customer logos and enhancing its referenceability.

Sharpening its Execution by investing in delivery excellence.

Building its Leadership bandwidth and expertise.

Intellect operates in a high gestation — high upfront costs but low incremental costs business. Like most software product companies, Intellect was incurring losses in its initial years on an income statement level, because investments in Research & Engineering and Sales & Marketing are front-loaded; Both — key cost lines as a percentage of revenue were in a range of 20-30% and 40-50% respectively. But these costs do not remain at these elevated levels forever. It comes down significantly as the company transitions from the investment phase — to the monetization phase.

Turning Revenue into Operating Profit

Margin expansion can make growth better than it looks — margin expansion usually happens when the gross margin is high, price competition is low, and fixed cost is significant. The best form of leverage in business is products with no marginal cost of replication. It's awesome when you see this unfold in the numbers. Voila, Intellect Design Arena for you — The business is extremely scalable because the software has zero (or near-zero) marginal costs once developed, i.e. it costs virtually nothing to create another copy. Combining this scalability with subscription-based pricing results in a revenue model with high gross margins and predictable revenue.

Bill Gurley on the value of high gross margins for a business:

“There is a huge difference between companies with high gross margins and those with lower gross margins. Using the DCF framework, you cannot generate much cash from a revenue stream that is saddled with large, variable costs… Selling more copies of the same piece of software (with zero incremental costs) is a business that scales nicely. Companies that are increasing their profit percentage while they grow are capable of carrying very high valuation multiples, as future periods will have much higher earnings and free cash flow due to the cumulative effect of growth and increased profitability.”

To understand the nature of this business, you must know the difference between what economists call rival and nonrival goods. With a rival good, one individual’s consumption reduces the quantity available to others. A car, a pen, and a shirt are examples. In contrast, many people can use a nonrival good—a set of instructions—at once. Software is the prototype. A company can distribute software widely. And since the additional use of this knowledge does not rely on scarce resources, wider sharing may lead to more growth.

The software can enjoy strong economies of scale because they are commonly cheap to reproduce and share. Economies of scale are a measure of cost per unit as a function of output. The original code may be very expensive to produce but the cost per unit sold drops rapidly because it is inexpensive to share.

Scale Economies Shared

Scale Economies Shared—a term coined by Nicholas Sleep, describes a business that shares the benefits of scale with its customers; ‘increased revenues begets scale savings begets lower costs begets lower prices begets increased revenues’. These businesses optimize for longevity - not short-term profitability. Persistent low prices attract customers, leading to increased turnover that drives scale benefits which are then returned to the customer in the form of even lower prices; a virtuous feedback loop. As the business grows, the moat gets wider.

SaaS providers can achieve higher economies of scale, which translates into lower pay-as-you-go prices due to a large number of banks using the same services.

There are very few business models where growth begets growth. Scale economics turns size into an asset. Companies that follow this path are at a huge advantage.

The basic way that companies grow is by earning a return on investments. Return is measured by profits, which are the product of sales and margins. Investments can be tangible or intangible assets.

The nature of the investment has changed markedly in recent decades, from one dominated by tangible assets to one mostly in the form of intangible assets. Intangible assets have some characteristics that distinguish them from tangible assets, including greater potential economies of scale and higher risk of obsolescence.

The good news is that intangible-intensive companies can grow faster than their tangible counterparts. The bad news is they can also become irrelevant and shrink fast.

The high growth prospect of software businesses attracts a lot of people. But, growth, just for the sake of it, is harmful. One key to wise growth is making sure what Warren Buffett wrote in his 1992 letter is true:

“Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous… Growth benefits investors only when the business in point can invest at incremental returns that are enticing – in other words, only when each dollar used to finance the growth creates over a dollar of long-term market value. In the case of a low-return business requiring incremental funds, growth hurts the investor. In The Theory of Investment Value, written over 50 years ago, John Burr Williams set forth the equation for value, which we condense here: The value of any stock, bond or business today is determined by the cash inflows and outflows – discounted at an appropriate interest rate – that can be expected to occur during the remaining life of the asset. Note that the formula is the same for stocks as for bonds. Even so, there is an important, and difficult to deal with, difference between the two: A bond has a coupon and maturity date that define future cash flows; but in the case of equities, the investment analyst must himself estimate the future “coupons.” Furthermore, the quality of management affects the bond coupon only rarely – chiefly when management is so inept or dishonest that payment of interest is suspended. In contrast, the ability of management can dramatically affect the equity “coupons.”

The key difference between traditional software and Software as a Service is that — Growth hurts, but only at first. Companies like Oracle and SAP do most of their business in the traditional software world by selling a “perpetual” license to their software and then later selling upgrades. In this model, customers pay for the software license up front and then typically pay a recurring annual maintenance fee (about 15-20% of the original license fee). This is great for old-line software companies and it’s great for traditional income statement accounting. Why? Because the timing of revenue and expenses are perfectly aligned. All of the license fee costs go directly to the revenue line and all of the associated costs get reflected as well, so a $1M license fee sold in the quarter shows up as $1M in revenue in the quarter. That’s how traditional software companies can get to profitability on the income statement early on in their lifecycles.

Now compare that to what happens with SaaS. Instead of purchasing a perpetual license to the software, the customer is signing up to use the software on an ongoing basis, via a service-based model — hence the term “software as a service”. Even though a customer typically signs a contract for 12-24 months, the company does not get to recognize those 12-24 months of fees as revenue upfront. Rather, the accounting rules require that the company recognize revenue as the software service is delivered (so for a 12-month contract, revenue is recognized each month at 1/12 of the total contract value).

Yet the company incurred almost all its costs to be able to acquire that customer in the first place — sales and marketing, developing and maintaining the software, hosting infrastructure — upfront. Many of these up-front expenses don’t get recognized over time in the income statement — So, the timing of revenue and expenses are misaligned.

Therefore, the income statement alone can no longer tell us everything we need to know about a SaaS business.

Even more significantly, the cash flow timing is also misaligned: The customer often only pays for the service one month or year at a time — but the software business has to pay its full expenses immediately.

Thus, cash flow is a lagging not a leading indicator of the business’s financial health.

“The constant rise in the importance of intangibles in companies’ performance and value creation, yet suppressed by accounting and reporting practices, renders financial information increasingly irrelevant.”

— Baruch Lev and Feng Gu, The End of Accounting (2016)

These types of recurring revenue businesses are different because the revenue for the service comes over an extended period (the customer's lifetime). If a customer is happy with the service, they will stick around for a long time, and the profit that can be made from that customer will increase considerably. On the other hand, if a customer is unhappy, they will churn quickly, and the business will likely lose money on the investment that they made to acquire that customer. This creates a fundamentally different dynamic to a traditional software business: there are now two sales that have to be accomplished:

Acquiring the customer

Retaining Customers (to maximize the lifetime value).

Once Intellect has generated enough cash from its installed customer base to cover the cost of acquiring new customers, those customers stay for a long time. The business is inherently sticky because the customer has essentially outsourced running its software to the vendor, making them very predictable to model and more likely to yield high cash flows.

When a software company (in our case, Intellect) transitions its business to a SaaS model, revenues and earnings often decline initially. Generally, the company loses the traditional upfront licensing payment and replaces it with a lower monthly subscription fee. And expenses are often higher in the near term because a true shift to a SaaS platform requires investment in technology, salespeople, billing services, etc.

In industry parlance, this is sometimes referred to as “Swallowing the Fish” because of the fish-shaped effect a subscription transition can have on a company’s profit metrics. But, as the majority of users are transitioned, revenues and earnings typically recover and margins can potentially exceed prior levels. The recurring nature of the new subscription revenue stream not only has more potential for pricing power, as it is easier to institute modest price increases regularly, but it also requires less selling and servicing expense.

“The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you’ve got a terrible business.”

— Warren Buffet

Embedded Switching Costs

Intellect has embedded switching costs for its current customers and can charge higher prices for equivalent products or services than competitors. This benefit only accrues in selling follow-on products to their current customers; they hold no benefit with potential customers and there is no benefit if there are no follow-on products.

Embedding works when you integrate your software into a customer’s operations so the customer can’t rip you out and replace you with a competitor. This is even more prevalent when customers are organizations, not individuals, and is typically accompanied by a direct sales force to drive the embed.

Embedding directly heightens switching costs as part of the process of user adoption.

Ultimately, we see the reverse of what we saw in the investment phase of the company: all the costs of acquiring that customer were incurred upfront and long ago, and now the company gets to harvest nearly all the incoming cash flow from its customers as profits.

The real assessment for investors to make, then, is not whether current revenue and earnings per share multiples are too high — but whether you believe that the investments the company is making today (that by their very nature depress near-term earnings and cash flow) are being made appropriately and thus will result in true free cash flow generation over time.

Understanding what the past and present do to the future, matters most.

Multi-Tenancy

Another interesting aspect about this business is Multi-Tenancy — A “multi-tenancy” solution is where a single instance of the software application serves multiple customers. The customer of the software, or tenant, may be given the ability to customize some parts of the application, but they cannot customize the application’s code.

The SaaS revolution, although a creature of the internet revolution, did not hit its stride until well after the first internet boom had crashed and burned. The national buildout of broadband capacity combined with dramatic improvements in computing and storage capacities facilitated the explosive growth of “on-demand software,” as the sector was often originally described. The idea of providing software as a service was not a new one. Service bureaus targeting small- and medium-sized businesses (SMBs) had provided central hosting applications dating back to the 1960s. And a variety of so-called application service providers (ASPs) emerged in the late 1990s to provide hosted software for an affordable monthly charge, sometimes delivered over the internet. But these software implementations were typically “single-tenant”—only one company could use them at a time. What was truly revolutionary about the SaaS model was that it allowed a single instance of the software to serve multiple clients simultaneously, a so-called multitenant architecture. And what vastly expanded the market potential was the increasing acceptance, and ultimately preference, of even global multinational businesses for SaaS applications.