Kotak Mahindra Bank: Anti-Fragile Among Fragile?

Concentrated India — Diversified Financial Services — Surrogate For The Booming Indian Economy!

If money is the lifeblood of an economy, then banking is the heart that keeps that blood pumping.

Banks in their most basic form are simply financial intermediaries that help people who have money (depositors) find people who need money (borrowers). A world without banks is inefficient. It’s also risky. It places the burden of handling transactions, securing money, and facilitating investments in the hands of everyday people who in most cases aren’t equipped to take proper care.

“If you are going to function in society, as an individual, a mom-and-pop business, or a billion-dollar corporation, you need one or more of the following: a bank account, a business loan, a car loan, or a mortgage, and with every bank account, business loan, car loan or mortgage, comes fees charged by the bank for the myriad services it provides.”

― Warren Buffett

When asked why he doesn't own banks, Terry Smith, a notable British fund manager, replied, “having an understanding of banks would make anyone wary of investing in them.” Banking is inherently a fragile business. In banking, a single event can play a significant negative role — Like the bank makes profits for years, then loses all and more it ever made in a single episode.

It’s the consistency, not the amplitude, of earnings that drive long-term value in banking. The first rule of compounding, Charlie Munger once said, is to never interrupt it unnecessarily. This is especially true in banking, where losses can snowball into acute shareholder dilution.

The financial sector appears glamorous, but it is fundamentally very fragile. Therefore, it is crucial that a firm has the simplicity and humility to say that this is a very difficult real-life business. The business of money is truly "fragile, handle with care".

— Uday Kotak

This is due to leverage—leverage is a double-edged sword. To many people, the biggest risk in the banking industry is leverage - banks are inherently levered entities. Leverage is simply the use of borrowed funds (which for a bank includes deposits), as opposed to equity, to purchase or otherwise acquire assets and run operations. In and of itself, leverage isn’t good or bad, it’s simply a tool. Leverage is a magnifier.

Leverage is the friend of a good bank, the enemy of the mediocre. Most companies are leveraged by a factor of three. The typical bank is leveraged by a factor of ten. This enables a bank to compound value at a rapid rate, but it also leaves little margin for error. “And mistakes, have been the rule rather than the exception at many major banks," says Warren Buffett.

One thing that makes banks different from traditional companies from a leverage standpoint is that banks are experts in managing risk. This is what they do (or are supposed to do anyway) all day long. For an industrial company borrowing to finance equipment, the sky is the limit when it comes to the potential return on their investment. Banks, however, lend money with known return characteristics. A bank’s risk department is responsible for ensuring that the bank doesn’t concentrate too many loans in a given sector. The underwriting department’s mandate is to attempt to write loans that will not lose value. Banks aspire to perfect underwriting records, even though that’s impossible. In addition, a bank can manage its deposit cost to better match up with its lending portfolio risk.

“Risk management lies at the core of what distinguishes financial institutions. One of the things fintechs are very good at is understanding customer convenience. But there is a balance between customer convenience and the safety of their money. This is a very important distinction — one that we as bankers normally learn the hard way. As a leveraged institution, the bulk of our money is other people’s money, and the net equity ratios of banks are obviously much higher than those of any other form of company…

Banks focus on managing risk because they have very small capital and a large amount of leverage. Fintechs are a while away from grasping the consequences of getting it wrong with leverage or customer security and losing money because of it. This is where I think the roles of fintechs and banks are going to be more complementary. Banks, meanwhile, can learn a lot from fintechs about being customer-friendly.”

— Uday Kotak

The biggest actual risk to a bank is the same risk that exists for any company - operational risk. This is the risk that management makes bad decisions. Perhaps they grow too quickly or in the wrong direction, hire the wrong people, make bad loans or other investments, and so on. All businesses have operational risks. All human beings are flawed and by definition, a business is an entity run for and by human beings.

The hardest part of banking is the need to balance opposing forces — Efficiency vs. Employee Morale, Revenue Growth vs. Risk Management, Short-Term Performance vs. Long-Term Solvency.

It takes a master swordsman to balance opposing forces to triumph at the battleground of banking. Uday Kotak is one such master swordsman — A banker among bank “executives”. He exhibits the even temperament that’s needed to steer highly leveraged institutions through the unforgiving vicissitudes of the credit cycle.

Born in Mumbai into a large joint family of Kutchi Gujarati traders, Uday Kotak had a keen entrepreneurial spirit, inclined more towards finance than his family’s commodities trading business. After an MBA from the Jamnalal Bajaj Institute of Management Studies, Mr. Kotak thought of a financial consultancy firm, but a keen eye for opportunity drew him towards discounting bills of large corporates.

Looking back, the transformation of banking from a purely social project to a more sustainable socio-commercial business dramatically unlocked India's economic potential. However, in the earlier socialist era, profitability and governance were relegated to the immediacy of providing institutional credit, leading to structural inconsistencies. Administered rates and operational inflexibility choked the competitiveness of banks. One such gap sparked what I saw as an opportunity: bill discounting!

— Uday Kotak

The First Taste Of Spread

In the 80s, Uday Phadke, one of Uday Kotak’s friends from JBIMS joined a Tata company, Nelco. Nelco was in the business of radios and electronics and always found itself tight on working capital. As its suppliers had to be paid 90 days later, Nelco used to borrow money for 90 days from banks at 17% through bill discounting, a rate mandated by RBI back then. Also, under the Credit Authorization Scheme (CAS), large companies like Nelco had a cap on the money they could raise from banks. The cap, at the time, was Rs. 5 crore. So, suppliers used to be in distress due to delays in payments.

Uday Phadke made Mr. Kotak a proposition, He said, ‘If you have some affluent friends, Nelco will accept a bill of exchange. You arrange payment for the supplier. And at the end of 90 days, Nelco will pay back the money. It is a Tata company, after all.’

‘At what rate of interest?’ Uday Kotak asked.

‘At 17%’ Uday Phadke responded.

In those days, bank deposit rates (fixed deposits) were 6% and lending rates were 17%, as fixed by India’s central bank. The banks were making a large spread, and there was money to be made by anybody who could enter and find a way of reducing this spread. This is where Uday Kotak sensed, “Your margin is my opportunity.”

Uday Kotak spoke with a few friends and family. He offered them a 12% return if they were willing to take the “Tata” risk—The name Tata was synonymous with security. He raised small amounts from each contact, ranging between Rs. 50,000 and Rs. 1,00,000. And instead of lending Nelco money at 17%, Uday Kotak said to Uday Phadke. ‘You give me more business. I shall make the lending rate 16%.’ Earning a spread of 4%.

Such bill-discounting was a serious business with narrow time margins.

“The money had to come into the account before the outgoing cheque was issued. The cheque would take 24-48 hours to clear, and within that time I would make sure that the refinancing would take place.”

— Uday Kotak

The fact remains that Mr. Kotak got his first business with zero capital invested. And that is how Mr. Kotak got into bill discounting—the buying and selling of paper.

“We bought it at 16%, and like a holder in due course, we endorse it. I would give physical hundis to investors, with invoices, challans, etc. As a bill of exchange is a negotiable instrument, we used to buy the bills, write the cheque, re-discount them and keep the spread. The banks were making 11%; we were making 5%. Due to the complexities of the interest rate system and differential spread between the deposit and lending rates, where banks were working with the spread between 6% and 17%, we could intermediate and create a market. That is how we started and soon the business grew…

Later all the foreign banks came - European Asian Bank and others. None of them had a deposit base here. But they were ready to take credit risk, so they would do what was known as co-acceptance. You also had another set of foreign banks and Indian banks who had surplus money like Standard Chartered, American Express, and some of the Indian banks, in which case, it became an inter-bank risk. If a Nelco bill was co-accepted by a European Asian Bank, you could do an inter-bank risk transaction. We then moved beyond individuals - to buy bills and refinance them from Indian banks. That’s how the whole bill discounting saga played out…

We made significant profits through bill discounting because the market was imperfect and there was no concept of the private sector in financial services.”

— Uday Kotak

Symbol Of Trust

In banking or finance, trust is the only thing you have to sell. Mr. Kotak had decided quite early that he would not refrain from putting his reputation on the line. This resolve became stronger when he read numerous books on top financial institutions like JP Morgan, Goldman Sachs, and Morgan Stanley carrying their family names. He, too, decided to put his name, front, and center. This thought was reinforced when he visited the United States in 1992, by which time the family name was established. Today, Kotak Mahindra Bank (KMB) is the only Indian private sector lender which retains the family names of its promoters.

“If you believe in yourself and the business, you should put your family name on the line. However, let’s be honest. The Kotak name was not well-known then, but the addition of Mahindra’s name gave the company instant credibility and recognition.”

— Uday Kotak

Like Nelco, Mahindra Ugine Steel was also a Kotak client. It was through this relationship that a game-changing event occurred in 1985, when Uday Kotak first met Anand Mahindra, now chairman and managing director of the Mahindra Group.

Steel was always in need of working capital. When they met, Mr. Kotak told Anand Mahindra, ‘We will raise money for you through bill discounting in 72 hours.’ In those days, 72 hours was quick.

Anand Mahindra, just 30 at the time, was impressed with the young Uday Kotak:

“When we met, the mini steel business was in recession. I remember asking him why he was willing to lend to us given the industry’s fragility. He promptly replied that his credit evaluation was based on the promoter’s reputation and record,” “I vividly remember being very impressed with his [Kotak’s] maturity and my gut instinct told me this young man was going to make an impact on whatever he chose to do. So rather impetuously I told him that if he ever decided to expand his firm and get into the leasing business—for which the government had recently liberalized licensing—I would be pleased to back him.”

— Anand Mahindra

Anand Mahindra subsequently invested Rs. 4 lakhs in Mr. Kotak’s venture in 1986. Apart from money, Mr. Kotak asked Mahindra to be able to associate the Mahindra name alongside his own. Mr. Kotak explained to Mahindra,

We are in the business of reputation. Names matter. Let’s put our names into the company. All the great financial houses—the Morgans, the Rothschild’s and the others—are known by the names of their founders. Let’s show people that we care enough about this business to put our names on it.

And thus, Kotak Mahindra Finance Ltd. (KMFL) started operating as an NBFC in April 1986. With an initial capital of Rs. 30 lakhs.

Taking On The Mighty Citi

In 1989, another major opportunity presented itself to Mr. Kotak, when Citibank entered the car financing business in India. Citi offered customers car loans at a flat 13% hire-purchase rate of interest, which remained the same even though the loan balance lowered, thereby taking the bank’s internal rate of return to as much as 36%. That was the kind of spread in the car loan business. Foreseeing the opportunity, KMFL immediately entered the business of car financing. As an NBFC, it borrowed from banks to lend to customers against their vehicles as security.

There was no way we could compete against Citibank, but Citi had one constraint. They could lend against cars only when the vehicles were available and cars were in short supply. Having a ready car to sell was a differentiating factor.

Uday Kotak recalls,

We came up with an interesting solution. Maruti was making the most popular car then, with a six-month waiting period for delivery. So, we started the concept of booking cars in bulk, so that when the customer wanted, we could provide instant delivery. We could pre-book 5,000 to 10,000 cars in our own name, effectively like a dealer would, but with the understanding that when the car was delivered, ownership would be moved to the customer’s name. Thus, we were able to give our customers instant delivery. However, in those days, there was a high premium on the cars, We decided not to charge the premium, but customers who wanted the car from us on instant delivery terms had to get the car financed from us. That is where the spread was and we were able to compete with Citi. The finance terms and interest rate were same as Citibank—13%, It worked and became a good business for us.

Turning Into A Bank

On 2 January 2001, Dr. Bimal Jalan, then announced the opening up of the Indian banking sector to private sector banks by giving out new bank licenses and releasing the guidelines for new private sector banks.

The decision to transform itself from an NBFC to a commercial bank was the result of long deliberations among the core Kotak Mahindra team. Mr. Kotak felt that if they have to be a sound, stable, strong financial institution in India serving customers, they must have a banking platform.

“At that point, nobody was interested in banking. If we had to be meaningful in India, we had to have a full customer view.”

— Uday Kotak

And thus, Kotak Mahindra Bank (KMB), a new private sector bank, the first NBFC to be converted into a commercial bank, was born in February 2003.

As a new bank among established players like HDFC Bank and ICICI Bank, KMB needed to position itself differently from the other banking companies.

Mr. Kotak clarifies the thought that went into the question:

Our platform is based on two simple principles. One is convenience and the other is solutions. We offer convenience by telling our customers they can use any bank’s ATM and we will pick up the tab by providing a pretty significant home banking facility, where we pick up cheques or cash from a customer’s home. We have a small customer base and we bring a differentiation; the larger banks cannot compete because they cannot offer the same facility to millions of customers.

The second platform is - solutions. How do we differentiate ourselves as ‘Bank No. 110’? I don’t remember the exact number, but we were pretty low down. So, we created a theme. We reasoned that people have known us for our prowess in investment, capital markets, and securities. We were also known for our partnership with Goldman. So, we decided to start a bank that would provide high-quality differentiated advice that was concisely caught in ‘Think Investments, Think Kotak.’ Our entire branding is based on that - it is the origin of ‘Think Investments, Think Kotak’. In India, most banks don’t talk about investments, capital markets, etc. We offer solutions and advice. The challenge is: how do we integrate services while keeping the RBI regulations, as between banking and brokerage, in mind? More and more customers need both and it is not easy to integrate. Regulation is one issue, the other is that the nature of the brokerage customer is different from a bank customer; bundling them can bring powerful results.

Propelling Into The Big League

Acquisitions have been hard to come by in the banking sector because good assets are never available at a reasonable price. Kotak Mahindra’s all-stock acquisition of Bengaluru-headquartered ING Vysya Bank in November 2014 was a strategic move that came at a reasonable price. With the valuation differential between KMB (~4.5x P/B) and ING Vysya (~2.2x P/B), the equity dilution was limited to just 15 percent.

The deal not just brought size, but also reach in terms of a complementary branch network. The merger helped Kotak double its branches and expand its network pan-India, with a deeper focus on the south. Importantly, in one stroke, the bank garnered a total of 64,600 crores in assets and 44,600 crores in deposits, making it the fourth-largest private sector bank in the country with assets totaling 1,98,000 crores and deposits amounting to 1,12,000 crores at the time of the merger.

The deal helped KMB leverage ING’s digital banking strength, as ING was among the top two or three consumer banks in Germany with zero branch presence, as also its expertise in international corporate banking. It helped KMB ramp up its branch presence in South India, in a scenario where 46% of KMB’s branches were in West India only. The bank was also able to diversify its loan book beyond its own retail loan business, as ING’s strength was its small and medium enterprises (SME) clientele. With ING Vysya nearing the foreign shareholding cap of 74%, the merger also yielded more liquidity and significant headroom for foreign money, as the foreign shareholding was 47%. The deal also helped Mr. Kotak reduce the promoter’s stake in KMB, in line with the roadmap given by the RBI, and move towards the prescribed stake of 30%.

Business of Exclusion

Banking can be thought of as a business of exclusion. Banks are more or less market takers on deposit and lending rates. That is, they generally must do what the market as a whole dictate as it relates to rates on loans and deposits. A bank might be able to make a few extra points at the margin, but deposit-taking and lending are commodity businesses that are incredibly competitive in most cases.

Because banks are taking deposits and making loans at the market rate, the levers they have to control their performance are the types and quality of the loans they make and their expenses. Banking is a business of exclusion because bankers need to be able to walk away from questionable loans, whether as a result of the quality of the loan itself or the pricing. In an environment where people need money, it is prudent to pass on most deals and only extend loans to the best borrowers at the best possible prices.

Lending can be described as having a limited upside with lots of downsides. In the world of banking, risk reduction means avoiding bad loans. This is easier said than done. Banks feel pressure from their shareholders and their board to continually grow. If the pressure is strong enough on the lending and underwriting team, it won’t be long until some poor-quality loans slip through the cracks.

“In the banking business, errors of commission are more expensive than errors of omission. In the investing business, it is the other way around. Errors of omission are more expensive than errors of commission.”

— Uday Kotak

Interestingly, if a bank pays the average rate on deposits, earns the average rate on loans, avoids bad lending, and has average expenses, it isn't an average bank, but an above-average bank. As Warren Buffet says, “Banking is very good business if you don’t do anything dumb.”

With little differentiation in finished products (loans and services) and no aspirational value attached to these products, low raw material cost (as measured by the cost of funds) and superior execution are the only two key competitive advantages for a bank. Moreover, a hugely leveraged balance sheet (10x leverage is normal for banks) means that below-par credit selection usually has a disproportionately large adverse impact on the bank’s profitability.

I believe that in the case of a bank, liabilities are bigger assets than assets, and therefore building the deposit franchise sustainably over a long period of time is core to sustainable banking. If there is one thing we are deeply committed to that is building: a), low cost and sustainable deposit franchise. b) Banking is a business of risk but I believe that the returns must be commensurate or better than the risk you take. If there is an x amount of risk, the returns out of that risk should be x plus. Most of the time, bankers make a mistake in pricing this risk and in that context, one of the important maxims we have at Kotak is return of capital is more important than return on capital. It is very easy to lend but very difficult to bring money back. And therefore, as long as we think we can get a good return commensurate or better than the risk we will lend. c) We love knowledge and franchise businesses, businesses which are built on brand, reputation and knowledge and skill. Those are the businesses which do not require financial capital therefore keep on building those businesses. d) Digital is here and real and therefore future depends on how well you can manage a world which is a combination of digital and non digital. These are our four mantras; low cost and sustainable deposits and building of the liability franchise and take risks but must get disproportionate returns for the risk. Knowledge, skill and franchise businesses matter and digital is our present and future.

— Uday Kotak

The Road To Power (Less Risk On The Asset Side) In Banking Is Paved With Low-Cost Liabilities (CASA)

Customers view deposits as a place to safely store their money and perhaps get interest payments, whereas bankers view deposits as a funding source, the fuel for their lending engine. Customer deposits can be a huge source of strength for a bank. A bank that can successfully acquire cheap and “sticky” deposits (i.e. deposits from customers who expect little in interest that are unlikely to walk quickly out the door for a little extra interest) can gain an advantage over competitors. Banks without strong deposit networks struggle to fund their daily operations.

Kotak Mahindra Bank’s strategy is based on its fundamental philosophy to build a low-cost and stable liability franchise, and it has been successful in that over the past decade.

Deposit funding can be one big conundrum for most banks. When Kotak was relatively new in the banking business, attracting savings account customers seemed like a daunting task.

The move by the Reserve Bank of India to de-regularise interest rates on savings accounts in 2011 helped KMB build its CASA franchise, which has significantly contributed to lowering KMB’s cost of funds.

Though nobody saw an opportunity, Kotak moved quickly and leveraged this opportunity by increasing its savings bank interest rates to 6% for balances above 1 lakh and 5.5% for others – a move that translated into significant growth in savings accounts. Within 2 years of RBI’s interest rate deregulation, Kotak more than doubled its savings account book from 3,330 crores as of 31st March 2011 to 7,268 crores as of 31st March 2013, posting a CAGR of 48%.

KMB launched a campaign ‘6 is bigger than 4’ hitting at the 4 percent rate that almost all banks were offering at that time. The medium selected to bombard the message was the 20-20 extravaganza, the Indian Premier League (IPL), the weapon was sponsoring fours, and the message was ‘Why take 4 when 6 is more.’

At a time when consumers used to care only about interest rates of fixed deposits, KMB changed the narrative, and game, overnight. While the savings account book of Kotak was at 3,331 crores in the year ended March 2011, it leapfrogged to I,69,313 crores in the year ended March 2021. What is more, in March 2011, HDFC Bank, ICICI Bank, and Axis Bank were 20 times, 21 times, and 13 times, respectively, of Kotak on the savings book size. By March 2021, the respective numbers had shrunk to 3.6 times, 2.5 times, and 1.8 times.

A bank with low-cost deposits is a bank with a good brand. This blanket statement can be made because it’s hard for banks with bad brands and reputations to attract deposits.

Initially, KMB was losing money on the retail deposits, but this customer acquisition cost was necessary to take short-term pain for long-term gain. Kotak has the ‘capacity to suffer’. These retail deposits are extremely “sticky” in nature, “Once you onboard a deposit customer, the relationship is practically lifelong. So, you first need to attract deposit customers before you can start offering products and services to them,” says Dipak Gupta.

Obviously, we need to make this customer much more engaged with us and, over time, significantly profitable as well. This is our front-end investment which is creating immediate cost pressure but building a very strong base for our future.

— Uday Kotak

Stability is critical, and that comes from savings accounts. Not only is the cost of funds lower on these accounts, compared with the overall cost of deposits, but they also allow the bank to cross-sell financial products to a larger base of customers, which now stands at 26 million. For example, in the unsecured credit card business, 90% of the bank’s incremental signups come from existing customers.

Recently, Uday Kotak realized every banker’s dream — “We have dropped rates, at the same time we have kept the customer franchise.”

Deposits can be a source of a bank’s competitive advantage. Every bank relies on deposits for funding, but banks that can maximize their deposit structure, grow deposits, keep costs low, and retain customers are a step or two ahead of other banks. A bank’s deposits are a very powerful profitability lever that banks can use.

A bank’s deposits provide a low-cost source of funding and are a crucial asset that should be cultivated and nurtured. Too many banks view their deposits as a cost center, but deposits aren’t the only expenses for a bank. A bank also has expenses related to acquiring and supporting its deposit base.

“We consider the customer franchise as a key part of our decision. We are not going to give away our customer franchise and the savings deposit growth strategy which we have had, while obviously being conscious of the commercials of what we are doing. Therefore, it's a very careful balance we are doing between those, and ensuring that the franchise of sustainable and low cost deposits and the competitive advantage we have, we keep on driving home while reducing the cost of funds for the Bank.”

— Uday Kotak

KMB’s CASA ratio has increased from 32.2% at the end of March 2012 to 60.7% at the end of March 2022. While CASA ratio for HDFC Bank, ICICI Bank, and Axis Bank stands at 46%, 41%, and 45% as of March 2022. This provides a significant competitive edge, as they are able to leverage their low cost of funds to lend more aggressively and open up further opportunities to acquire high-quality customers.

With our mix of over 60% CASA, our cost of funds is a significant competitive advantage I would like to believe, probably best in class. And we will hammer that cost of funds advantage to get significant customer engagement and produce our risk-adjusted returns in totality.

— Uday Kotak

Now, you must be wondering that despite paying more interest on deposits to customers as compared to peers, how come Kotak has the lowest cost of funds. This is because the incremental deposits were growing at a very fast pace and became a higher proportion of the overall funds. So, despite paying higher interest on SA, Kotak managed to have a lower cost of funds by having the proportion of CASA higher than its peers. This made Kotak have the proportion of least preferred deposits which are term deposits lower than compared to its peers.

When a customer puts money on deposit at a bank, they have to choose what type of account they would like. They can choose between different products, such as a current account, a savings account, or a fixed deposit. In any of these types of accounts, the money is on deposit at the bank only so long as the customer desires. Banks attempt to manage the duration of deposits through a variety of deposit products. A demand deposit is a deposit that can be redeemed by a customer at any time. Think of this as similar to a traditional current liability.

Term deposits are products that lock up a customer’s funds for a specified amount of time. Often, the maturities in these types of products are longer than a year. Banks attempt to lock up funds in FDs with stipulations on the product. A customer can cash out an FD earlier than the maturity date, but they end up paying an early redemption fee or being penalized to the tune of a few months’ worths of interest. Think of a term deposit as similar to a non-current asset. In general, a bank’s demand deposits are a cheaper source of funding compared to term deposits.

When a bank can’t attract sufficient deposits they are forced to rely on other funding sources — Subordinated Debt Instruments, RBI, and inter-bank borrowings.

CASA plus term deposits below 5 crores account for 91% of the total deposits for KMB.

When everything can be processed online a bank’s branches have lost their value as a touchpoint for customers and have become an expensive line item on financial statements. It doesn’t make sense to employ people to serve customers in a building that customers never frequent. “Today, every customer has the branch on their mobile. The mobile is the biggest branch. Hence, being the Godzilla is not necessarily going to be a big advantage. At Kotak, in the coming years, you will see and hear a lot more from young engineers and data scientists and less from grey-haired people in the ranks,” says Dipak Gupta.

Banks have modified their deposit sales from a previous brick and mortar existence and moved to the digital world.

What we look out for is customers and capabilities, not physical branches. When I say I have 1600 branches, I think it would be a liability if I had 10,000 branches. And that's very clear because I think the digital and technology change is going to make the density of branch network requirements… more even for current account customers, for savings account customers… 94% of the transactions have moved outside the branches…

Our view is that expenditure on physical will be more measured, it is going to be much more around customer, products, digital experience on a strong technology base. And if at all, we will be spending more money, it's going to be in these areas and we are not going to stop that spend in the short to medium term for really what I think is a significant catch up where our competition may not just be other banks, our competition has to be tech players of the future and present and how they are playing the game and how do we learn from them. I think Indian banks have a unique opportunity that while we continue to be regulated, how do we transform and transcend to be a customer-oriented product tech player.

— Uday Kotak

Fundamental to Kotak’s strategy going forward is a combination of conventional branch banking and digital banking. The bank has been aggressive with its digital push. Be it creating a great customer experience through its mobile app or engaging with customers through chatbots or acquiring customers through social media channels such as WhatsApp or Twitter, Kotak is experimenting constantly.

It took Kotak Mahindra Bank eight years to acquire its first million customers. The next 2 million came in just four years, thanks to the 6 percent savings account offer it rolled out in October 2011 when the Reserve Bank of India deregulated savings interest rates. If 6 percent gave Kotak its ‘aha’ moment, 811 gave Kotak its ‘gaga’ moment. ‘811’ — a banking app that allowed customers to open accounts with zero balance and complete all KYC formalities on their smartphone in just under 10 minutes. Kotak was the first bank in India to integrate the Aadhaar-based OTP authentication process for account opening on mobile. Only Aadhaar and PAN numbers are required to open and operate 811.

With Aadhaar, we set out to create a forward-looking digital ID platform that would empower over a billion Indian residents to get access to services at unprecedented speed and convenience. It is heartening to see how the banking industry, led by Kotak 811, has leveraged Aadhaar to reimagine bank account opening from days to minutes. I commend Uday and his team for taking the lead and continuing to leverage the power of technology and Aadhaar as they transform the banking experience for Indians.

— Nandan Nilekani

This app was inspired by the date on which Prime Minister Narendra Modi had announced demonetization—8 November or 8/11. The goal was to try and double the customer in 18 months and was in fact KMB’s response to the disruption in banking.

A year ago, we set out on an ambitious journey to bring millions of Indians into the banking fold by using technology to mitigate much of the friction in opening a savings bank account. We now aim to expand the convenience and simplicity of 811 to make banking more accessible to Indians across all demographics in every `Kona’ of our country.

We had started the launch of 811 in end of March 2017 with 8 million customer base. And we had said that we would want to double that in 18 month period. As of September, which is end of 18th month, we have crossed the customer base mark of 16 million customers.

— Uday Kotak

In January 2020, when the RBI amended Know Your Customer (KYC) norms and introduced the video-based KYC option to onboard customers, KMB was the first bank to integrate the video KYC process in the account opening journey.

“My science fiction view of banking is that you will see a complete blurring of financial services and technology, and banks of the future will have to work at a quarter of their current cost models.”

— Uday Kotak

The launch of 811, India’s first downloadable digital banking ecosystem with biometric-led KYC verification, has resulted in a paperless, real-time banking experience for customers, reducing the turnaround time for opening a bank account from a few days to a few minutes, has reduced the cost of customer acquisition and has increased the productivity of field force. This new product has significantly reduced the cost of customer acquisition, compared to its regular accounts, by almost 80-90%. Even more, servicing these accounts costs next to nothing.

According to Uday Kotak, a smart branch strategy combined with digital will ensure that they can expand the productivity of low-cost liability and deposit base.

A strong, durable advantage on the deposits side in terms of economies of scale at the customer level and the branch level especially is what creates value in banking.

Efficiency and prudence are in harmony, not conflict. Being a low-cost provider bestows tremendous strategic advantages on a bank beyond immediate profits. An efficient bank can be competitive on the asset and liability sides of its balance sheet — making better loans to better borrowers and securing a more stable source of funds — yet, still earn over its cost of capital.

Asset quality is paramount.

When the marketplace is in trouble, bullets will fly around, some will even hit you. You just have to ensure that not too many do and that the few that hit you do not kill you.

— Dipak Gupta

Asset quality is paramount. As an outsider, we don’t have access to know or understand the details of a bank’s troubled assets. What we do know is the level of troubled assets in relation to their capital and the trend of their troubled assets. Use history as a guide.

KMB has managed to maintain strong control over asset quality on a multi-year basis. The bank’s gross non-performing assets (NPA) largely remained between 2% and 3% over FY15-FY19 and moved up to 3.56% at the peak in 1QFY22 during the pandemic. The bank has further demonstrated its control of asset quality with GNPAs at 2.34% in 4QFY22, despite the ongoing pandemic. Similarly, the credit costs have remained in the sub 1% range on an annual basis even during events such as demonetization and implementation of the Goods and Services Tax and The Real Estate (Regulation and Development) Act. However, the bank’s credit costs surged in a few quarters during the past two years due to the creation of COVID-19-related provisions in addition to the provisioning requirement during the pandemic. However, while KMB has written back 452 crores from the COVID-19 provision buffers in 4QFY22 with the impact of subsequent waves of the pandemic becoming less impactful, it still carries 547 crores as additional COVID-19 provisions.

A non-performing asset is a loan or an advance where the borrower has stopped making required payments for 90 days or more (there are other factors and NPA can encompass different things, but a longer discussion is outside the scope of this post). It’s important to note that designating a loan as non-performing doesn’t mean that it’s worthless.

When a loan becomes non-performing the bank begins the process of maximizing its recovery either via foreclosure of the property, repossession, or through filing an involuntary petition for bankruptcy against the borrower. In most cases, the process of recovery is arduous – it’s long, costly, and ties up the bank’s capital for an extended period.

Some NPAs do in fact go to zero - most don’t - but what they have in common is that all of them by definition are not performing as expected.

Think of past-due loans and NPAs as an early warning system for future potential problems. If a borrower starts to miss payments or make late payments for extended periods it is likely, or possible in any case, that they are experiencing some financial distress.

What makes Mr. Kotak the banker that he is that, RBI asks to wait for 90 days to declare an account NPA, Mr. Kotak said that “even if it is not 90 days, in our assessment if there is an inherent weakness in the account then we will go ahead & classify it as NPA.” This is in total contrast to where every banker tries to hide NPAs.

“Where we have questions on the viability of the business, we have taken a bolder call, let this flow-through NPA rather than give moratorium which is kicking the can down the road.”

Net NPA is the amount resulting from the sum of the defaulted loans after deducting provisions for uncertain and unpaid debts. As of 31st March 2022, Kotak’s net NPA stands at 0.64%.

The provision for loan losses is a contra account found on the balance sheet. That is, it’s simply a reserve for expected or anticipated losses on outstanding loans. Periodically, a bank will review their loan book and analyze whether they expect (based on certain criteria) to receive the contracted principal and interest on each loan. To the extent they determine a loss might be suffered, they are required to reserve funds to cover that loss. If and when losses are incurred, the loan loss reserve account is reduced.

When the economy hits a rough patch and losses are anticipated, one will often see the allowance for loan losses increasing dramatically quarter over quarter. As losses are realized, this amount is reduced. There is a timing disconnect between when the funds are reserved via the income statement and when they are actually applied at a later date. Often you’ll see that there has been an excess of reserves put away, and they are “released” when things improve. When reserves are released they end up on the income statement increasing net income and, thus, distorting profitability.

Kotak aggressively provisioned in the early phase of the Covid crisis.

For sustainable build-up of value, we are ready to endure pain today in the P&L, if we make a mistake or lose money.

— Uday Kotak

When KMB acquired ING Vysya Bank, it immediately identified bad assets and moved that almost entirely into a separate distressed asset division. It represented 6% of the ING Vysya book and 2.5% of the combined book. The management was not afraid to take a hit on the P&L. Later in FY18, twelve accounts across all the banks were taken into insolvency and bankruptcy. Of that Kotak had four accounts and all of them were inherited from ING Vysya Bank which was already identified as bad during acquisition.

A well intended measure of smoothening cash flows through restructuring runs the risk of becoming a tool for 'ever greening'.

We don’t like restructuring as a philosophy, so we’ve always been very conscious and conservative about doing restructuring. We would rather take it, and take the pain through P&L and get our recoveries… First on let me just give you again something which is on philosophy which is important. If we have to restructure a loan, as long as we are not going to lose our money, we are comfortable making an NPA and then restructuring as a philosophy. And therefore, if you look at our restructured standard loan it is the lowest in banking. And that is coming again out of a view that much rather restructure after taking it through the NPLs if we have to. And of course, it is not that we don’t restructure just for the heck of it. Because when you take a loan to an NPA, your provisioning is much higher than a restructuring, number one. Number two is in a restructuring you continue to accrue interest. In an NPA, you stop accruing interest as well as reverse the accrued interest. So both these from a revenue and P&L point of view are significantly different from a standard restructured loan but we are happier to do that because at least we know what are the things we really need to focus on and get on with, trying to get fair value of that asset.

— Uday Kotak

Throughout the 2010s when corporate loan restructuring was available, banks used it to hide NPAs. Kotak on the other hand let the questionable loan slip into NPA & had a very minimal restructured book.

Even after the Covid crisis, Kotak has a minimal restructured book. The standard restructured book, whether it is through COVID-1, COVID-2, or MSME resolution framework all put together, is 0.54% of its overall book.

Examining a bank’s assets for future risk is worthless if the bank is currently on shaky footing. And as we can see, Kotak is on a strong footing.

A bank's troubled assets show what’s happening now, the bank’s loan portfolio holds the key to what could happen in the future.

When looking at a loan portfolio, one should try to envision the types of ways the portfolio could cause bank issues in the future.

Future credit risk at a bank is determined in part by looking at the existing trends related to the loan portfolio and extrapolating them into the near-term future. It should be pointed out that extrapolations far into the future don’t hold much predictive value, but in the near term, outside of exceptional circumstances, current trends tend to continue until they’re forced to change.

Ultimately, a bank’s lending mix in terms of size, yield, and industry will determine its profitability and related risk profile. Lending is a balancing act between loans that are potentially riskier but yield more, versus loans that are perceived or deemed to be safer, but yield less. A bank also needs to balance the size of loans and borrower mix. A bank that goes “all-in” on riskier loans to increase their portfolio yield and interest income need to either have a high loss reserve or a bankruptcy attorney on speed-dial.

The first principles of finance: if you put in 10 of equity and borrow 100, you can lend out 110. However, if just 5 of loans out of the 110 go bad, you lose 50% of your equity, and it takes just 10 of assets going bad to bankrupt you!

It is important that banks focus both on "return on equity" as well as on "return of equity".

— Uday Kotak

The types of loans, the duration of those loans, the lending mix, as well as the historical performance, tell a story about a bank’s management and the quality of its lending. For Kotak, lending is rooted in the belief of being a custodian of depositors’ money and providing returns for years. The reason Kotak is a prudent banker is that he clearly understands the core nature of the business — Equity is a very small portion of the total balance sheet of banks but bankers start thinking they have control and ownership of overall assets. The truth is: they don’t, it is other people’s money.

We are not obsessed with high margins, but we are certainly obsessed with risks for the returns we get.

— Uday Kotak

“You can afford to run much less risk in banking than in commerce, and you must take greater precautions because a banker, dealing with the money of others, and money payable on demand, must be always, as it were, looking behind him and seeing if payment should be asked for.”

- Walter Bagehot, author of Lombard Street: A Description of the Money Market (1873)

Kotak has always been focused on building a healthy and profitable business. It has been particularly focused on ensuring the right risk-return metrics. Pricing models such as Risk-Adjusted Return on Capital (RaRoC) measurements have got ingrained in the system.

“It’s not that we’re scared of taking risks. When you look at our stressed assets portfolio, bought from other banks, you might say we are the highest risk-takers in the industry. But we are willing to take risks after understanding them and believe the pricing must justify the risk.”

— Dipak Gupta

Banks exhibit both bicycle and table stability. Both a bicycle at speed and a table are stable items. However, for the bicycle to remain stable it needs to be continually propelled forward, whereas a table is by nature stable. Some banking business models rely more on the bicycle model than one might expect. When a bank is engaged in short-term, high-interest lending (consumer lending, auto lending, construction lending, short-term business lending) they are in continual pursuit of new borrowers as their old borrowers churn off. If the pie of new borrowers doesn’t continually grow, the bank will eventually find itself in a situation where it needs to compromise its lending standards to find growth.

When looking at a bank’s loan portfolio, ask yourself the question, “Is this sustainable?” Is the bank’s lending mixture sustainable in both good times and bad times?

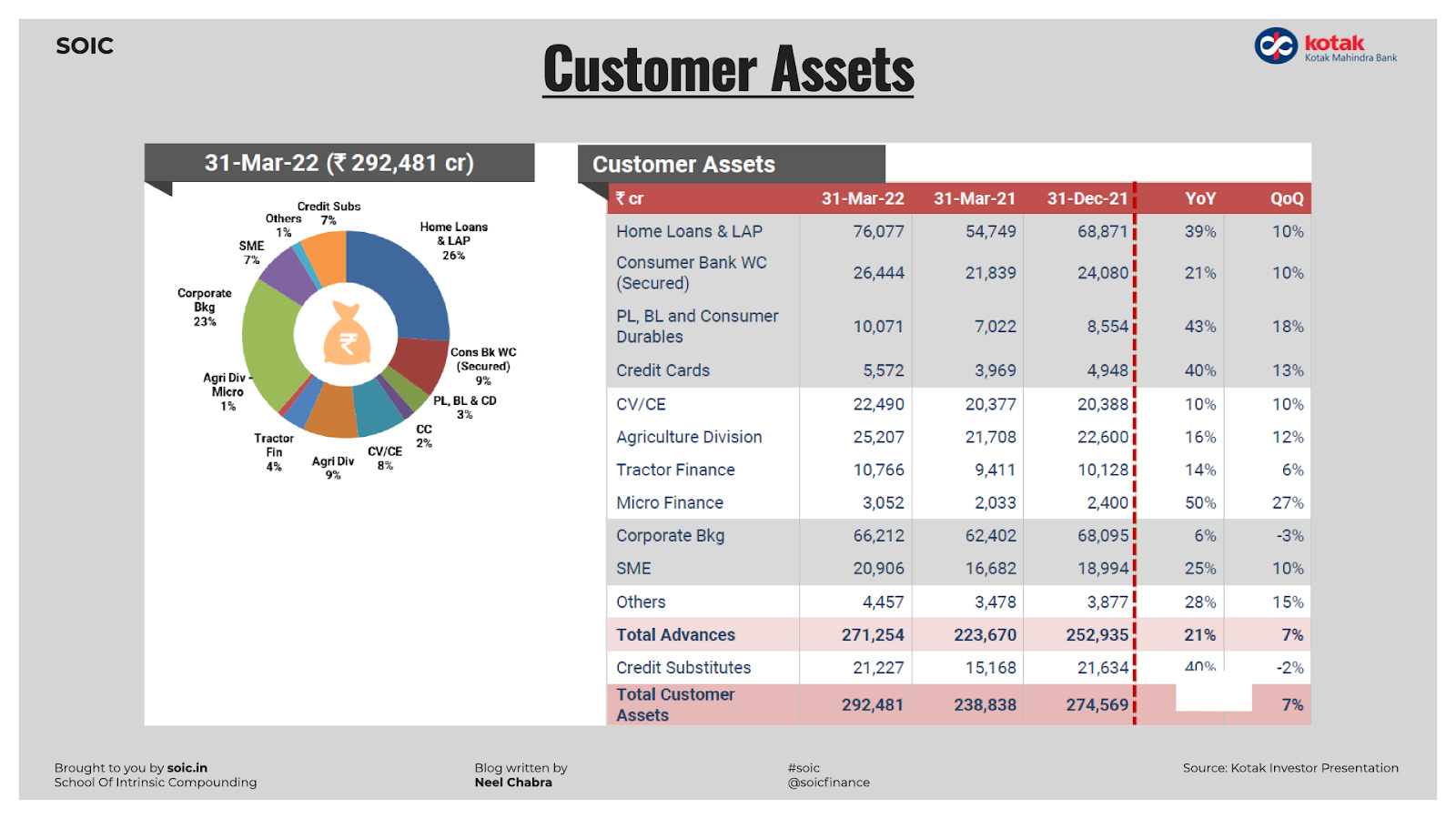

Kotak has proven time and again that its book is sustainable in both good and bad times. It has a well-diversified, sustainable asset book with a balanced mix of Wholesale (Corporates and SMEs), Commercial (Commercial Vehicles, Construction Equipment, Tractor, Agriculture), Secured Retail (Home Loan, LAP), and Unsecured Retail (Consumer Durable, Credit Cards, Personal Loan) with few drips and drabs of other lendings.

The crux of banking is watching what others are doing and then not doing it yourself.

“The 'sound' banker, alas! It is not one who foresees danger and avoids it,” John Maynard Keynes wrote in 1934, “but one who, when he is ruined, is ruined in a conventional and orthodox way along with his fellows so that no one can really blame him.” Warren Buffett calls this the institutional imperative — “the tendency of executives to mindlessly imitate the behavior of their peers, no matter how foolish it may be to do so.”

With the Indian economy booming during the 2000s, corporate banking proliferated as companies went into an expansionary mode. Several fledgling private sector banks such as ICICI Bank and Axis Bank were gaining heft lending to corporates during the bullish years till 2008, but Kotak Bank displayed little aggression. Unlike others, Kotak adopted a prudent and cautious approach, targeting only high-rated customers and sectors. It avoided riskier longer-term project finance in favor of shorter duration loans and secured working capital loans, given its conviction of taking only lenders’ risk and not equity-type risks for lending returns. This allowed it to build scale in its corporate banking business in a healthy manner.

Return-of-investment is more important for us than only return-on-investment, Hence, we avoided riskier longer-term project finance in favor of shorter duration loans and secured working capital loans in order to ensure taking only lenders’ risk and not equity-type risks for lending returns.

— Uday Kotak

Uday Kotak did not succumb to temptation even as peer banks, especially foreign ones, were aggressively offering derivatives products to corporate clients and taking away business. After the tide went out, we all knew who was swimming naked. When the cycle turned and banks started going slow on corporate lending given stress in their books, Kotak sensed an opportunity and started targeting market share to ramp up its corporate book. Over the past few years, corporate assets have consistently grown by over 20% and their proportion to the overall advances has increased to 39%. Kotak continues to differentiate itself in its strong understanding of risk, helping it to deliver healthy and profitable growth. The use of Risk-Adjusted Return on Capital models has assisted pricing optimization and helped to better judge the risk-return metrics. Risk-Weighted Assets as a percentage of total assets have consistently declined, and the book enjoys industry-low NPAs even at the time of COVID.

In corporate banking, in addition to the spread in the lending business, we make significant flows on foreign exchange, transaction banking, deeper customer engagement, translating into our broader relationships, including with our investment bank. So there are a whole host of linkages in the corporate banking business beyond just the lending products. Trade is another very major part, current account growth, all that is deeply interconnected and integrated to the lending piece in the corporate banking, and therefore I would request look at some of these as engines for customer returns.

— Uday Kotak

If risk return tradeoffs work well we are always open to growing the corporate book, at a pace that the market offers the opportunity at. Our key metrics has always been the right risk return tradeoffs, our relationships are fairly wide, we have fair presence in most corporates. Right from the top end to medium sized corporates, our coverage and presence is fairly wide and we’re fairly confident that if the secular growth in the corporate credit requirement goes up, we will be able to capitalize on that. And as I mentioned, our transaction banking franchise is also growing very well.

In the corporate we have used our new digital products, new online portal, new CMS platform, all of that is making a lot of difference. And we are quite confident that we can grow this franchise if the market opportunity allows us to do that.

— KVS Manian

From 2010-to 2012, Kotak had shied away from infrastructure financing, even as other banks and financial institutions had dived in. “These projects promised higher yields, but it was a space we did not understand and has been known to often cause asset-liability mismatches,” explains Jaimin Bhatt. For those who did lend to the sector, time and cost overruns showed up in a few years, resulting in huge non-performing assets (NPAs) that they are still struggling to recover from.

Over the past year, instead of direct lending, Kotak saw a greater demand for credit substitutes, a type of lending wherein the bank subscribes to corporate bonds or non-convertible debentures of top-rated corporates. “As an alternative to lending as loans, we have frequently invested in bonds of companies. In terms of risk management, it is better when you have bonds as you can manage exposures by selling them any time you want, unlike loans,” says KVS Manian. As of March 2022, the credit substitutes portfolio stood at ₹21,227 crores.

“Lending is usually the least RoE (return on equity) product in a relationship. We keep the RoE on our corporate banking business higher through cross-selling multiple products such as transaction banking, cash management, payments, collections, trade finance, investment banking, equity brokerage, wealth management, and so on. This also helps us in building a comprehensive corporate franchise. For instance, the bank on the investment banking side caters to conglomerates such as the Tatas, Bharti, Aditya Birla Group, Godrej Group and the likes. There are three ways to grow — make very large loans, but they are low on pricing and don’t augur well for RoE, second, go slower in the corporate portfolio, and third, be selective on loans but build a comprehensive multi-product relationship with a focus on client-level profitability. “Being selective is the game we play…

We measure risk adjusted return on capital in each relationship and make sure that we make the right profits in the relationship. It is easy to lend ₹5,000 crore more by lending very cheap for a 15-20 year tenure. But we don’t like very long loans because we don’t like to take that kind of asset-liability mismatches. So, we want to make RoEs within those risk management principles that we follow.”

— KVS Manian

The Bank’s maxim that ‘return of capital is more important than ‘return on capital’ has manifested itself many times in its history, and one such example is its Commercial Vehicle/Construction Equipment (CV/CE) loan book. When the CV/CE financing business was going very strong, the Bank foresaw the danger of over-heating in the market and that the industry was prone to overcapacity. Kotak had its ears to the ground and chose to be contrarian by consciously reducing its exposure to CV/CE financing from December 2012. As a result, Kotak’s CV/CE book came down to ~ 5,000 crores in December 2014 from its high of ~ 8,000 crores in September 2012. During that period, the Bank reduced its monthly disbursement by 80% and largely catered to its existing good customers. The CV/ CE book came down, but there was no shutting down of branches, and Kotak chose to take the operating expenditure pain rather than capital pain – a strategy that proved to be beneficial amid the peaking NPAs and defaults in the industry. By September 2015, however, on regaining comfort in the segment, the Bank again started increasing disbursements, bringing its book back to 8,000 crores in June 2016 and is standing at 22,490 crores as of March 2022.

Over the last 2 years, Kotak has barely grown its loan book. Uday Kotak was the first one to warn about stress in unsecured retail. He now says: “We have undertaken a mindset shift to make retail and commercial lending our focus, in addition to the corporate and deposit franchise. For example, we are leveraging our low cost of funds to offer a competitive interest rate on home loans. Home loans give us an opportunity to build longer-term relationships with customers. And we will get bolder in unsecured retail finance too, for which we’ve kept our powder dry over the last two years.”

For home loans, we think home loans is one of the most sticky products in a customer journey. And the ability to cross-sell a variety of products to a home loan customer is also a significant opportunity. A home loan customer who has got a core mortgage is a much safer customer to add a credit card or a personal loan, a home loan customer who has an engaging bank account, that again gives us a deeper engaging relationship with that customer. So we look, we are getting significantly more focused on customer engagement and customer returns, in addition to making sure that the product makes economic sense.

— Uday Kotak

“While distribution width and low-cost funds are important in the mortgages business, in today’s digital world, how you leverage technology to scale business and think differently matters. Also, the home loan market is a deep and wide market with sub-segments between ₹10 lakh and ₹10 crores. Within unsecured retail, the bank is building its credit card business by leveraging its upgraded tech platform. We had one of our best quarters with the acquisition of 3.9 lakh credit cards in Q3. The bulk of the sourcing has come from existing customers.”

– Shanti Ekambaram

On the unsecured side there are two separate sides, one is your unsecured which is really the personal loan, and the consumer durable financing and the business loan. That’s one type of unsecured, the other side is really the credit cards and that’s a very different opportunity because that is not just a pure lending opportunity it’s a very significant payment engagement and for some of them unsecured opportunity, but it’s a very significant engagement opportunity. So we’ll drive all of that and we are using a fair amount of analytics combined with some amount of experimentation to drive that…

Given our small base it is pretty comfortable to grow from that small base. And like I said earlier, we are really looking at the whole unsecured piece, essentially from our existing customer base. And within our existing customer base, our penetration on the unsecured side is practically negligible. So it basically means that we don’t really have to go out to get the growth, which we are talking about.

— Dipak Gupta

Kotak Mahindra Bank has now “pressed the accelerator” on unsecured products and is confident that credit cards as a product will continue to stay, although form factors may change due to technology developments and changes in consumer behaviour.

The idea of individuals wanting a credit line will stay. They may or may not use the plastic. That does not matter. The application has already gone digital. The card business is here to stay and is something we are invested in.

We would like to replicate our home loan strategy where we have dramatically increased market share in recent days and will gradually achieve Kona Kona Kotak Credit Card (Kotak card in every corner) in days to come.

Going forward, Kotak Mahindra Bank also plans to invest more in Buy Now Pay Later (BNPL) given the potential in that area.

— Ambuj Chandna

Net interest income is the difference between the amount of interest income the bank receives and the amount of interest expense the bank pays or incurs. Perhaps the most popular way of calculating this measure of profitability is by looking at a bank’s net interest margin (NIM) which is the difference between the income earned on interest-earning assets (i.e. loans) and interest expense incurred on liabilities (i.e. deposits and borrowed funds) to carry those assets, expressed as a yield.

NIMs shouldn’t be looked at in isolation. You have to look at NIMs along with the operating cost. While retail loans have higher NIMs, the operating cost is also high. And while on the corporate side, NIMs are less, the operating cost is relatively low.

Kotak had a NIM of 4.78% as of 31st March 2022. This is despite having a lot of assets in treasuries during the year, which yields less.

Over the past 8-9 years, Kotak has focused on getting its liability engine in place. Going ahead, they will focus on getting its assets' engine to start firing. “Asset business is an outcome of the head (logical customer thinking), whereas the liability franchise comes from the heart, as there is a lot of emotion, trust, and comfort involved,” says Dipak Gupta.

We are not constrained by the market size or the credit growth in the marketplace, we will be constrained by what we think is the right parameters and therefore as long as those parameters of our matrix gets met, we will go to whatever it takes to grow our loan book and assets.

If we believe we are getting the price for the risk we are taking, we’ll lend and are not obsessed by a number which is 20%, 25%, 30% growth. We are obsessed by the fact that the trouble with stress is it never comes at the time when you lend, it comes two years later.

Our template for growth as always will revolve around risk-adjusted returns. We don’t look at either – returns or risk - in isolation. Today we have a much lighter balance sheet and with sufficient capital in our hands, we are ready to grow substantially faster, but on our terms.

— Uday Kotak

A bank’s capital is best viewed in light of its loans and asset quality. It’s when those contexts are understood that a capital ratio makes sense.

Banks with too little capital should be given extra time for investigation, but banks with too much capital should as well. A bank that has too much capital has an inefficient and lazy balance sheet and isn’t maximizing its earnings. This is because too much cash is sitting on the sidelines and isn’t being lent out and used to make a profit. A bank’s purpose is to take insured deposits and invest those deposits into loans, not take deposits and invest them in a bond portfolio or simply hold them as cash.

A bank should have a pyramid structure to their assets, with their loans forming the base and being the largest item. The next layer in the pyramid is investment securities. The amount of securities should be less than the loans, but more than cash on hand. Finally, at the top of the pyramid is cash. When a bank doesn’t have a pyramid with its assets, they are conducting business inefficiently.

Kotak has a Capital Adequacy of 24%, among the highest in the Indian banking industry, and has a pyramid with their advances at 2,71,254 crores, investments at 1,00,580 crores, and 42,924 crores in cash as of 31st March 2022.

An easy litmus test for any bank is how it performed through the crisis.

Well-run banks embody the idea of antifragility. They underperform by a little in good times but outperform by a lot when times get tough.

Kotak has proven time and again that it is antifragile among fragile.

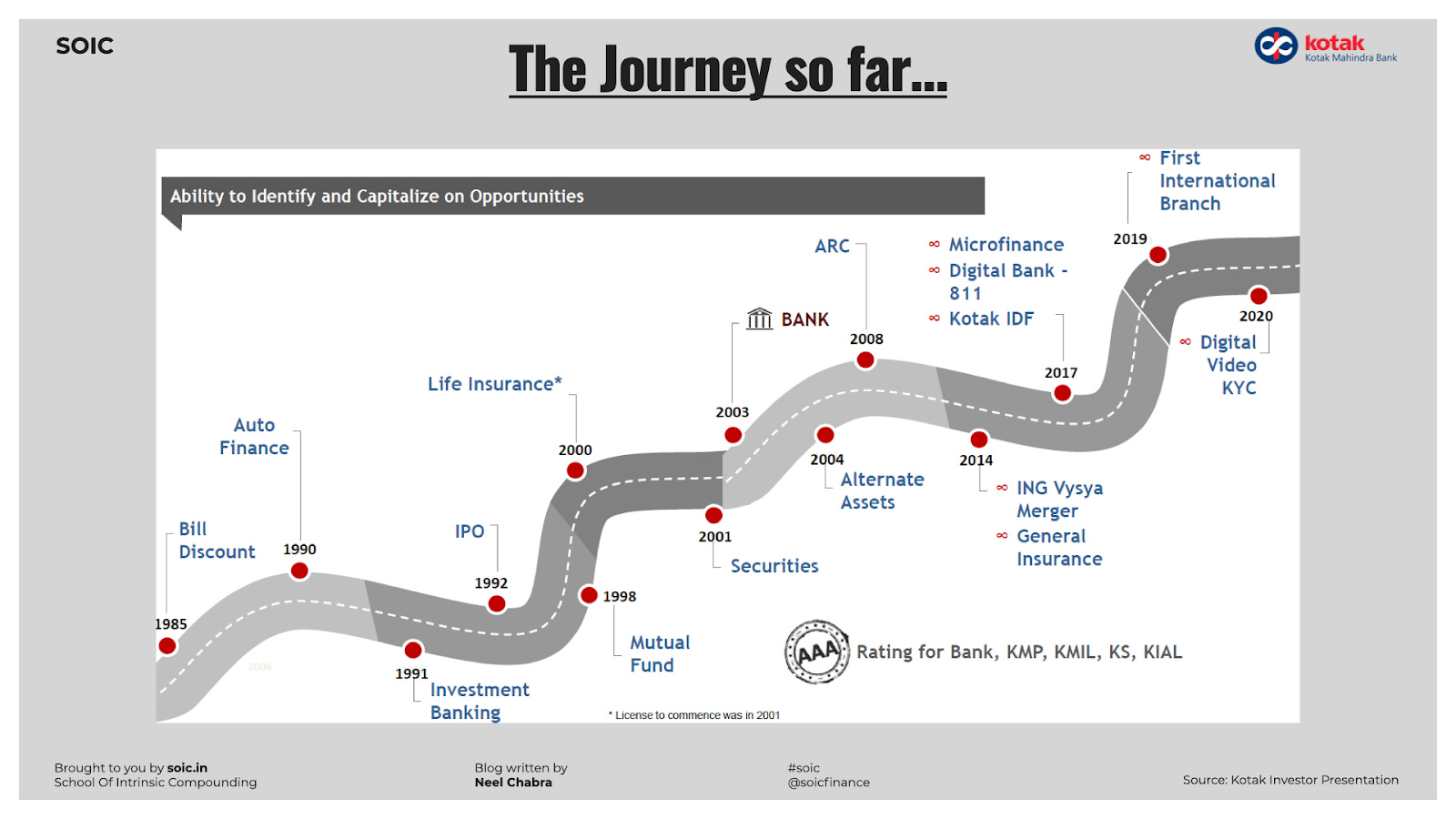

By the late 1990s, NBFCs were the flavor of the season and there were over 4,000-odd players spread across the country. But Uday Kotak was able to see the big picture quite early.

The nineties saw non-banking finance companies (NBFCs) mushrooming across the country. However, the Southeast Asian crisis of 1997-98 became a major testing point. Before the crisis, there were 4,000 NBFCs in India. Within the next couple of years, 99 percent went under. We were one among the two dozen-odd that survived, learning valuable lessons along the way.

We were getting very uncomfortable with the macro scene then — rates were high, companies were struggling to repay and the economy was slowing down. So we started to bring down our book dramatically. Only 1% of NBFCs survived that downturn and we were lucky to be one of those.

— Uday Kotak

Just a year before Asian Crisis, Uday Kotak saw the pain and pulled back to shrink the balance sheet from 1,800 crores to 1,000 crores. He could see that the financial sector was likely to go into serious defaults. So, he pruned his balance sheet by design. Thus keeping non-performing assets (NPAs) in check. Between 1997 and 1999, net NPAs were down to 3% of total assets from the earlier 5.51%. More importantly, it had healthy capital adequacy of 25% as of March 31, 1999. The learning from that phase has since stuck with Uday Kotak —“There is a very thin line between conviction and foolhardiness. If you are ready to back your conviction, go for it, but the risk is that if you are foolhardy, your conviction will hit you back. Making that distinction is very important.”

We were saved because we cut down our exposure. We still lost about 10% of our portfolio, which was large, but imagine the loss if we had expanded our portfolio from 1800 crore, as others did. Nobody saw it coming, not even financial institutions like IDBI, IFCI, etc. We hunkered down in our lending book. I told my people just to focus on equity and not the return on equity, meaning keep your capital in place. That's why we survived that phase with our net worth intact.

— Uday Kotak

Faced with the Asian crisis, several companies in India ended up defaulting, triggering a liquidity crisis for NBFCs, including some of the established ones. Over 3,000 NBFCs were impacted, and many collapsed. Kotak’s extreme prudence and conservatism, as an NBFC back then, not only helped it sail through the crisis but placed it in the enviable position of having other NBFCs approach it for their recoveries. Kotak saw this as an opportunity to pioneer the purchase of NPA portfolios. Starting with an MNC bank, it bought many portfolios from private and public banks, and along the way, the SARFAESI Act, of 2002 catalyzed business momentum. Kotak’s bold conviction, driven by its uncanny long-term vision, resulted in big business, generating high IRRs, commensurate with the risks taken. Kotak, at that time an NBFC, focused on strong capital reserves and prudent risk management. Once safe, it applied to the RBI for a banking license and began a new phase of growth in 2003.

As the credit crunch post, the collapse of Lehman Brothers went global in 2008. Sectors such as power and infrastructure were badly hit, and overall economic growth was plummeting. With the entire banking sector paralyzed by bad loans, Kotak had a field day. The bank’s bad loans, including stressed assets, stood at 2.39% in crisis-ridden FY09 but were down to 1.73% by FY10. Its advances grew 25% to 20,800 crores that year, and the bank clocked its then highest consolidated profit of Rs.1,300 crores.

Until FY09, KMB’s loan book primarily comprised retail loans (auto loans, CV loans, personal loans, home loans, etc.) with the share of retail loans being as high as 89% in FY08. However, the bank’s loan mix altered significantly post the financial crisis as the bank increased its focus on the corporate segment and cut down its exposure to the high-risk personal loan segment. Corporate loan book growth outpaced overall loan book growth in the coming few years, as KMB capitalized on its relatively well-capitalized balance sheet and superior asset quality to lend to blue-chip corporates during the 2008-09 financial crisis. While the bank’s overall advances grew by 2% in FY09, the corporate loan book growth was 20%. Similarly, overall advances grew 32% in FY10, while the corporate book doubled during that year. As other lenders became risk wary or faced the heat of the financial crisis, it gave KMB the opening it was looking for to enter the balance sheets of large Indian corporates. By the end of FY10, a quarter of KMB’s loan book comprised corporate loans vs. 11% in FY08, making it a much more stable bank with a balanced loan book mix.

The 2008 crisis hit home the importance of retail deposits. So, after the deregulation of savings rates in 2011, the bank went on the offensive wooing savers with a higher rate. Having protected itself through the crisis, Kotak saw an opportunity to grow and took the bold move of offering a rate of up to 6% to its savings account customers. The Bank backed this decision with 10 years of conviction, during which its savings deposits have grown from 3,330 crores as of 31st March 2011 to over 1,60,313 crores as of 31st March 2021.

It pays to act with alacrity in a crisis. "Run your business knowing it might be sunny, it might be stormy, or in fact, it might be a hurricane,” Jamie Dimon once said. “And be honest about how bad a hurricane might be." When a crisis strikes, it’s best to prepare for the worst.

And that’s exactly what Kotak did when the Covid crisis hit. It was the first bank to do a QIP despite its share price being down 30% to build a fortress balance sheet.

Only the strongest boats will see through the storm. A fortress balance sheet is a must, and this was one of the objectives of the bank’s QIP issue of 7,400 crore in May 2020. I am happy to report that the QIP had an overwhelming response. The Bank’s Tier-1 capital adequacy ratio (CAR) which was about 17% as on 31st March, 2020 has gone up to over 20% post issue, and the bank’s consolidated net worth has gone up from about 67,000 crore as on 31st March, 2020 to over 74,000 crore. This additional capital will support the bank in dealing with contingencies or financing business opportunities (organic and / or inorganic).

— Uday Kotak

Taking risks is an inherent part of the business, but managing risk takes considered judgment, which Uday Kotak has.

History teaches that bankers face nothing new under the sun. “We have been fighting on this planet for ten thousand years,” retired Marine Corps General James Mattis wrote in his memoirs, “it would be idiotic and unethical to not take advantage of such accumulated experiences.” The same is true in banking.

A bank’s profits are derived from its balance sheet.

If something did not create economic value, we would not do it just to boost the next quarter earnings.

If there is red ink on your P&L, it can be cleaned up. But if your balance-sheet is destroyed you are done for ever.

Over the years, I have found banks focusing more on the P&L than on the Balance Sheet. In fact, particularly for banks, the Balance Sheet is more important, and P&L is only a derivative of the Balance Sheet.

— Uday Kotak

For banks, while a profit is certainly important (who doesn’t want to make money?) it all begins and ends with the balance sheet. A bank’s profits are derived from its balance sheet. A bank with a bad balance sheet will have poor results and won’t be able to earn enough to survive a financial crisis. Even if survival isn’t at issue, a bad balance sheet will virtually ensure that a bank can’t earn its cost of capital.

Think of a bank as a machine, a continuous machine that takes in deposits, makes loans with those funds, and receives interest and ultimately the return of principal on those loans. The balance sheet is a snapshot of this machine frozen in place. It reflects the bank’s financial position at a single point in time. The bank’s other financial statements capture the flow of the machine over a given period, but the balance sheet is always as of a single point in time. This is important to remember, and this is why investors can never solely rely on a balance sheet alone for an investment decision.

We have seen that Kotak has its liability engine in place and more than enough capital adequacy to fuel the assets' engine going forward.

Because the majority of a bank’s income statement is derived from their balance sheet there aren’t many things to investigate that we haven’t looked at otherwise. The largest items on the income statement we haven’t seen at this point are non-interest expenses and non-interest income.

In a typical case, the majority of non-interest expenses for a bank are their operating costs. Operating expenses are a large category. In theory, anything that’s needed to operate the business can fall into this bucket. Operating expenses consist of anything and everything related to operating the business from employee salaries, rent, marketing, and information technology costs down to the purchase of branded pens, and tiny calendars.

Kotak’s operating expenditure stands at 11,121 crores as of 31st March 2022. This translates to Opex-to-Net Interest Income of 66% which is fairly high as compared to peers.

Efficiency is more about revenue than expenses. Highly efficient banks aren’t necessarily those with the lowest costs. The typical bank earns twice as much revenue as it pays out in expenses. So if a bank’s goal is to improve efficiency, expressed as a ratio of expenses over revenue, it’ll get twice the bang for its buck by increasing revenue relative to cutting costs. Uday Kotak believes that cost-to-income is an outcome rather than a target.

Ultimately cost to income will get corrected, but we are very clear at this stage. There are three clear engines which we are growing. First is on retail loans and there are front end acquisition costs. Just think about home loan. If there is a fee for acquisition or distribution to be paid a home loan, which has say average life of six, seven years or eight years though the loan may be 15 years average life is six, seven, eight years, you’re paying the fee cost upfront. And under banking regulation you have to take the full distribution hit at the point of time you underwrite the loan. And that doesn’t bother us because we are driven by underlying value creation, not necessarily what it does to my pre operating profit in a quarter that is not something which is the basis on which we take decisions, if we believe substantively it is going to add value, we are ready to take those costs upfront. But that is one, second you got to keep in mind, we have dramatically increased our customer acquisition from eight lakhs in the last year same quarter to 21 lakhs in this quarter. And we see that engine continuing to fire, again that takes front end cost. And we of course are very focused on unit economics of our acquisition cost on customers. But we think the acquisition cost upfront is not something which is going to deter us as long as we believe the underlying unit economics are strong. Therefore that is point number two. And point number three is, with the opportunity in the marketplace, which is coming in, with our overall balance sheet metrics, we will drive growth and we believe the cost to income ratio will be an outcome rather than a target. Therefore we think about getting the right outcomes, which will improve the cost to income ratio, because a lot of our costs are front end. And also keep in mind that as we get more and more digitized, the actual straight through processing digital lending transactions will ultimately reduce the effective intermediation cost as well. But these three or four parameters are what is going to drive us and in simple language first is really, the front end cost we are ready to take. Second, if we are growing our customer base at a very high speed, keeping in mind unit economics versus front end cost. Digitization will ultimately make straight through journeys, significantly lower operating costs, and fourth cost to income for us is an outcome, not a target.

A bank's non-interest income line item on the income statement encompasses any additional income the bank generates outside of interest from its lending activities (which also includes dividends received on its investment securities book). This could be anything from overdraft fees, fees for investment management services, mortgage servicing fees, credit card lending fees, and any gains (or losses) from sales of securities. Kotak’s other income stands at 6,354 crores as of 31st March 2022.

The Holy Trinity

Uday Kotak believes in the Holy Trinity. This world would not maintain its perfect balance unless Brahma, Vishnu, and Shiva – the creator, preserver, and destroyer co-existed. The same applies to companies too. “You need all three in your ecosystem. Brahma, who is constantly focused on the creation and new opportunities; Vishnu, to ensure continuity and growth; and Shiva, to creatively destroy to stay relevant”.

“Given the complexity of our firm, there are many pieces that may not make sense at some point. Over the past five years, there have been a number of internal divisions that we have merged and also some businesses where we took a tough call.” That’s Shiva’s territory. For example, in the commercial heavy vehicles business, the bank dramatically cut exposure when the risk was high. In the credit card business, the management took a hard call to grow the business internally and not through “agents at the airport giving out credit cards”.

“There are three most important things that will drive future growth for Kotak. The first is customer acquisition and customer experience, the second is significant investment and growth in the technology, and the third and the most important is getting the right talent for a new future in financial services. We are in a sweet spot.”

— Dipak Gupta

“In a marathon if you run too fast, you get exhausted. If you run too slow, you never make it. In today’s fast-paced world of rapid advancements in technology, we need to be ahead of the curve in terms of product offerings to our customers. In the newer normal, we need to keep evolving; however, developing technology involves money and time. Technology is quickly becoming obsolete. What is new today is old tomorrow and therefore at Kotak, we are partnering and investing in promising companies working on innovative and game-changing technologies which will be the backbone for our growth.”

— Jaimin Bhatt

Metamorphosis Into A Concentrated India — Diversified Financial Services Powerhouse

Fortunes can be made in banking, but only by earning consistent returns through multiple cycles. Banking isn’t a get-rich-quick business. There are graveyards full of banks that chased short-term performance at the expense of long-term solvency.

Warren Buffett’s observation: “No matter how great the talent or efforts, some things just take time. You can’t produce a baby in one month by making nine women pregnant” is apt for the financial services industry. As many who have tried and miserably failed have realized, financial services businesses cannot be built in a few years or even a decade. Uday Kotak’s entrepreneurial journey from the founding of Kotak Mahindra Financial Ltd. (KMFL) in his family’s 300-square-foot office to recently claiming the spot for the richest self-made banker in the world has been a journey of 35 years.

Over the last 35 years, Kotak has built up its business to provide the full suite of financial products for its customers.

It commenced operations in 1985 as a non-bank finance company providing bill-discounting services. In 1987, they entered the lease and hire-purchase business. With the opening up of the Indian economy in early 1990, they entered the auto finance (1990) and investment banking (1991) business to capitalize on new opportunities. Kotak completed its initial public offering (IPO) in 1992.