LTI -The Disruption Enabler

The surfboard to ride the digital transformation wave?

Surfing the Digital Transformation Wave

We have all heard that a rising tide lifts all the boats. But at the same time, one must identify the tide on time. Many times the same rising tide finds some people off guard and instead of lifting, it drowns them. That’s competitive destruction.

Charlie Munger says:

When technology moves as fast as it does in a civilization like ours, you get a phenomenon which I call competitive destruction. You know, you have the finest buggy whip factory and all of a sudden in comes this little horseless carriage. And before too many years go by, your buggy whip business is dead. You either get into a different business or you’re dead—you’re destroyed. It happens again and again and again.

And when these new businesses come in, there are huge advantages for the early birds. And when you’re an early bird, there’s a model that I call “surfing” – when a surfer gets up and catches the wave and just stays there, he can go a long, long time. But if he gets off the wave, he becomes mired in shallows….

But people get long runs when they’re right on the edge of the wave – whether it’s Microsoft or Intel or all kinds of people.

You won’t be able to surf if you don’t catch the wave. And if you do catch it, you can stay on it for long. The trick is catching the one that lasts the longest as early as possible and not getting off.

When it comes to investing, surfing is an indispensable mental model that every investor should be aware of. Because “That’s exactly what an investor should be looking for,” says Charlie, “In a long life, you can expect to profit heavily from at least a few of those opportunities if you develop the wisdom and will to seize them. At any rate, surfing is a very powerful model.”

LTI is surfing the digital transformation wave. And not just LTI, but the entire Indian IT industry. Y2K Boom put Indian IT on the map, Digital Transformation will make the industry claim the territory.

LTI was started by L&T Group’s Chairman AM Naik in 1996 as L&T Information Technology Ltd to retain talented software engineers within the group. It changed its name to L&T Infotech in 2001-02, and Sanjay Jalona, the CEO, rebranded it as LTI in 2017. Before hitting the public markets in 2016, L&T Infotech, as part of a business restructuring, demerged its Product Engineering Services (PES) business into a separate company—LTTS in 2014.

Today, LTI is among the largest global technology consulting and digital solutions companies, helping over 475 clients succeed in a converging world—With operations in over 30 countries across industry verticals—BFSI, CPG & Retail, Life Sciences & Healthcare, Hi-Tech, Energy, Utilities, Media & Entertainment, and Manufacturing.

Everything is Connected

Every company is part of an industry that is part of a sector that is part of a national economy that is part of a global economy. Living systems cannot be fully separated from each other. Nothing exists in isolation. Everything is connected.

The ecosystem lens reveals that the actions of anyone species have consequences for many others in the same environment. Many systems can take care of themselves, possessing abilities to correct and compensate for changes and external pressures. We need to take the time to learn how the components of our system are interconnected, so we can understand how our actions will impact the connections and affect the outcome we are trying to produce. And there are times when the rate of change increases not just in a particular industry, but across the entire global economy.

One of the major events that can increase the rate of change across all industries is the development of major new technology. And so in recent decades, we have seen the emergence of the global internet cause just about every industry to change the way they do business. The frequency with which disruptions are transforming industries has been consistently rising over the past 10-20 years. Innovative technologies, digitization, automation, machine learning, artificial intelligence—all these themes have been a significant source of disruption over the last decade. There are several other areas of disruption which could take place over the next decade.

You can either bet on disruptors or the disruption enablers—which can adapt and stay relevant among dynamic disruptions. Given a choice, I’d place my bet on the latter.

We're entering a digital-first world where digital transformation is a mandate, not a competitive advantage.

The digital transformation of companies will be a mixed bag. Some will hit gold and some will keep digging till they run out of runway. But both will buy shovels. We will see the rise of the ‘shovels’ that capture most of the profits while the rest of the economy scrambles for gold.

People and technologies often act as catalysts, increasing the pace of social change and development. Developments in technology typically act as catalysts for social changes. Catalysts accelerate reactions that are capable of occurring anyway. They decrease the amount of energy required to cause change, and in the process make possible reactions that might not have occurred otherwise. The COVID pandemic might just be one such catalyst—In fact, it is indeed.

If you think this is just rhetoric, listen to what Satya Nadella, CEO of Microsoft, has to say:

The pandemic has “fundamentally accelerated” the process of digital transformation across industries, and companies equipped with digital technology are going to be more resilient and be able to adapt faster to any tail event… “What we were going to think about during 2030 is probably going to be true in 2025.”

Satya Nadella, on why demand remains high for digital transformation:

"Coming out of the pandemic, we are seeing actually a lot of constraints in the economy. And the only resources ... that can help drive productivity while keeping cost down is digital tech."

Pandemic has ignited a new light into the IT industry for which obituaries started pouring in in 2016. I still remember the headlines floating around that time such as “Gloom in India’s IT sector”…“Indian software dies at 17 from failure to grasp future”… “Indian IT is a dead man walking”… “If you’re in your 30s and in IT, you might lose your job”… “Indian IT is dead!”.

Pandemic ne ekdum see waqt badal diya, jazbaat badal diye, zindagi badal di!

Dawn of the Inevitable

Sanjeev Jalona, CEO of LTI, says that if we zoom out and look at our lives during the last 100 years, there have been three mega economic events with a lasting global impact – the Great Depression in the first half of the 20th century, the Great Recession in the early 21st century, and the pandemic-led, the Great Restructuring.

This Great Restructuring is comprehensive, and every enterprise must adapt or cede its position. Retail and CPG companies must rethink go-to-market channels, Banking and Insurance companies must reassess risk, manufacturing companies must reconfigure supply chains, Healthcare companies must reinvent customer engagement, and every company in every sector must reimagine community responsibility. For an enterprise to capitalize on the post-pandemic boom in this decade, they need to understand and effectively leverage the Great Restructuring.

While there have been fundamental changes in the economic landscape in the last 100 years—There has been a fundamental change in computing from the 20th to the 21st century as well.

In the 20th century, computers existed in a purely digital world, and humans acted as the input and output devices, translating the analog world into digital and feeding it to the computer, and then taking its digital output and interpreting it to act on the real, analog world. In the past 15 years, computers have begun to sense and interact directly with the analog world, without relying on humans for input and output, accelerating processes by millions of times. This has made thousands of times more applications viable, leading to the accelerating invasion of our personal and business lives by technology.

We are in the middle of a dramatic and broad technological and economic shift, in which software companies are poised to take over large swathes of the economy.

Embracing Digital Transformation

“Software eating the world” has catapulted the tech industry’s total available market (TAM) from “IT” to the global economy. The software has moved from being a cost center to a profit center. Before the 2000s, tech companies typically sold digital tools to help companies improve productivity. Today, they compete with mature companies in the media, retail, financial, and automotive industries, among others, forcing incumbents to modernize and embrace digital transformation and, in turn, creating demand for software.

“Digital transformation” is the process of using digital technologies to create new—or modify existing—business processes, culture, and customer experiences to meet changing business and market requirements.

Digital transformation is the successor to digitization.

Digitization helped companies move their workflows from pen and paper to computers and software. With the internet at its core, digital transformation has been and is more profound.

While “Digital Transformation” sounds like yet another buzzword (I mean of course—“digital” “transformation”) but the truth is, it’s a generational shift and would last for at least a decade till it becomes “legacy” and something else takes over.

When it comes to IT companies, everyone is infatuated with dissecting revenue between “digital” and “legacy”. But what is legacy? Well, it is what “digital” will be in a decade or two.

A legacy system is outdated computing software and/or hardware that is still in use. The system still meets the needs it was originally designed for but doesn’t allow for growth. A legacy system’s older technology won’t allow it to interact with newer systems. When technology becomes obsolete it doesn't stop working, and, generally, it retreats to its core customers and their core use cases and puts up prices. That can be a great business, for a while. The old systems are good at the old things.

Around 55% of the revenue of LTI comes from these old things. This part of the business is growing relatively slowly.

In the 60s and 70s, giant companies bought mainframes, and in the 80s and 90s, the center of gravity of enterprise IT moved from mainframes to client-server, Oracle, Windows, and PCs. Now the center of gravity is shifting again, to cloud and SaaS, and a bunch of other technologies (AI, ML, Data Analytics, and so on…) that come with that. To generalize, anything related to all this new-age stuff is digital.

Around 45% of the revenue of LTI comes from this new-age stuff. This part of the business is relatively growing faster than the legacy and gaining more share of the overall revenue. The distinction is blurring though between legacy and digital—The reason why TCS has stopped reporting it as a separate segment a few quarters back.

Moving from mainframes to client-server didn't just mean you went from renting one kind of box to buying another—it changed the whole way that computing worked. In particular, software became a separate business, and there were all sorts of new companies selling you new kinds of software, some of which solved existing problems but some of which changed how a company could operate. SAP made just-in-time supply chains a lot easier. New categories of software-enabled new ways of doing business.

The same shift is happening now, as companies move to the cloud - you go from owning boxes to renting them, but more importantly, you change what kinds of software you can use. Now, enterprises can have a lot more software from a lot more companies.

Information technology has grown into a multi-trillion-dollar industry thanks to continuous improvements in costs and ease of use. The simpler it is to buy, deploy, maintain, and use computer systems, the greater the addressable market.

Just like economic decentralization, cloud-based software removes friction, opens up wallet share, and accelerates time to adoption.

The pandemic has created a reason to accelerate all of this. For example, a big CPG company might be perfectly happy with its ERP, except that it can't ship less than 1,000 units per order and now they want to do direct-to-consumer. A huge retailer that was perfectly happy with its point of sale system, but discovered that it can't be extended to do ‘buy online pick up in store’.

These are multi-year infrastructure migration projects; a muti-horizon transformation journey; a decade-long generational shift; a gradual, then suddenly shift; a generational shift that in some ways is as fundamental as the consumer internet’s shift from PCs to smartphones.

We’ve got another decade or two of ‘digital transformation’, and then it’ll be called something else.

Change of Guard

The IT and business process industry has fundamentally changed in the digital world, pivoting from value based on labor arbitrage to platforms to produce new value. With that pivot, leadership changes occur; while leadership changes are not always directly linked to the business model, a change in the business model inevitably creates leadership changes.

LTI appointed Sanjay Jalona as the CEO of the company in 2015 before its IPO in 2016. Since then, there has been stability in LTI management, which had seen material churn with three CEO exits over the prior five years. The only senior management exit that had been seen since is of their COO in November 2018.

Sanjeev Jalona joined after a 15-year stint with Infosys where he was the Global Head of the Hitech, Manufacturing, and Engineering business. Under his leadership, LTI perked up the leadership bench through the induction of talent from larger companies. These appointments had the experience of handling scale. Head of Sales was hired from NIIT Tech (prior experience at Infosys), Head of Manufacturing, Retail/CPG & Hitech/Media, Europe (ex-Nordic) all have backgrounds in Infosys, COO/Head of Nordics & Denmark was hired from Cognizant, CFO (Ashok Sonthalia) moved from the parent L&T group and some leaders were hired from Capgemini/Atos. Heads of Banking and Insurance have been LTI veterans, having joined the company in 2002 and 1997 respectively.

LTI has also been able to attract senior recruits, who have helped LTI deepen its capabilities and land large contracts. A senior executive in France who came on board recently is leading the charge to start a new relationship with a global 500 company in the energy and utilities vertical. The executive in France is positioning LTI as a strategic supplier for multi-year engagements on IT-led business transformation.

Another recent senior recruit is in the oil and gas vertical, with decades of industry experience at companies like Accenture, IBM, and Infosys. A third is an expert in the insurance vertical who joined LTI less than a year ago with more than two decades of insurance sector experience, including strategy and digital operations. Such hires are helping LTI win contracts, such as a $124-million engagement with a large multinational company, and a multi-million-dollar contract to provide services around cloud software for insurance companies from Duck Creek Technologies.

Sanjeev Jalona was attracted by the chance to leave a legacy and transform an operation that had started as the IT unit of a better-known engineering group into a world-class tech services provider in its own right.

“The dream and the vision is, all of us together will create a highly valued, highly profitable next-generation IT company,”

— Sanjeev Jalona

Since joining LTI, Sanjay Jalona has focused on positioning the firm for digital leadership.

Sanjay Jalona has carved out Friday afternoons for himself to reflect on what he calls “basic things”, which translates to thinking about what more LTI can do for its customers and how well it is doing by its people. Success in the former depends on success with the latter.

Such reflections are what have translated to investments in cloud initiatives, data products, and software-as-a-service platforms. Sanjeev Jalona spearheaded LTI’s digital services journey by aligning its existing areas of expertise and developing capabilities in emerging digital technologies. LTI has its focuses on scaling up digital services, including artificial intelligence (AI), cognitive intelligence, analytics, SaaS, cloud-related services, IoT, blockchain, and enterprise mobility amongst others.

LTI's offerings in Digital services

Apart from building capabilities organically, acquisitions have also helped add some of these capabilities. Sanjeev Jalona has done six ‘tuck-in’ acquisitions at LTI, spending a total of about $100 million on them.

MOSAIC, for example, was built on intellectual property developed by a Pune-based company AugmentIQ that LTI acquired in November 2016. MOSAIC is a converged platform, which offers data engineering, advanced analytics, knowledge-led automation, IoT connectivity, and improved solution experience to its users. MOSAIC was adopted by LTI as a service delivery method for analytics, Internet of things (IoT), automation, experience, artificial intelligence (AI), and blockchain to help its clients stay relevant in the digital world. MOSAIC recently has been made a part of Fosfor (a suite of 5 product offerings), which is a Data Products unit of LTI.

Syncordis, which LTI acquired a year down the line, opened up opportunities in banking software consulting and implementation—specifically, software from Switzerland-based Temenos AG. The acquisition also brought LTI the capabilities to provide banking software from Temenos in an as-a-service model and positioned LTI as a strong tech services provider around banking in the Nordic region.

PowerupCloud, added in October 2019, brought LTI a partnership with Amazon Web Services, the world’s biggest cloud provider, and related intellectual property.

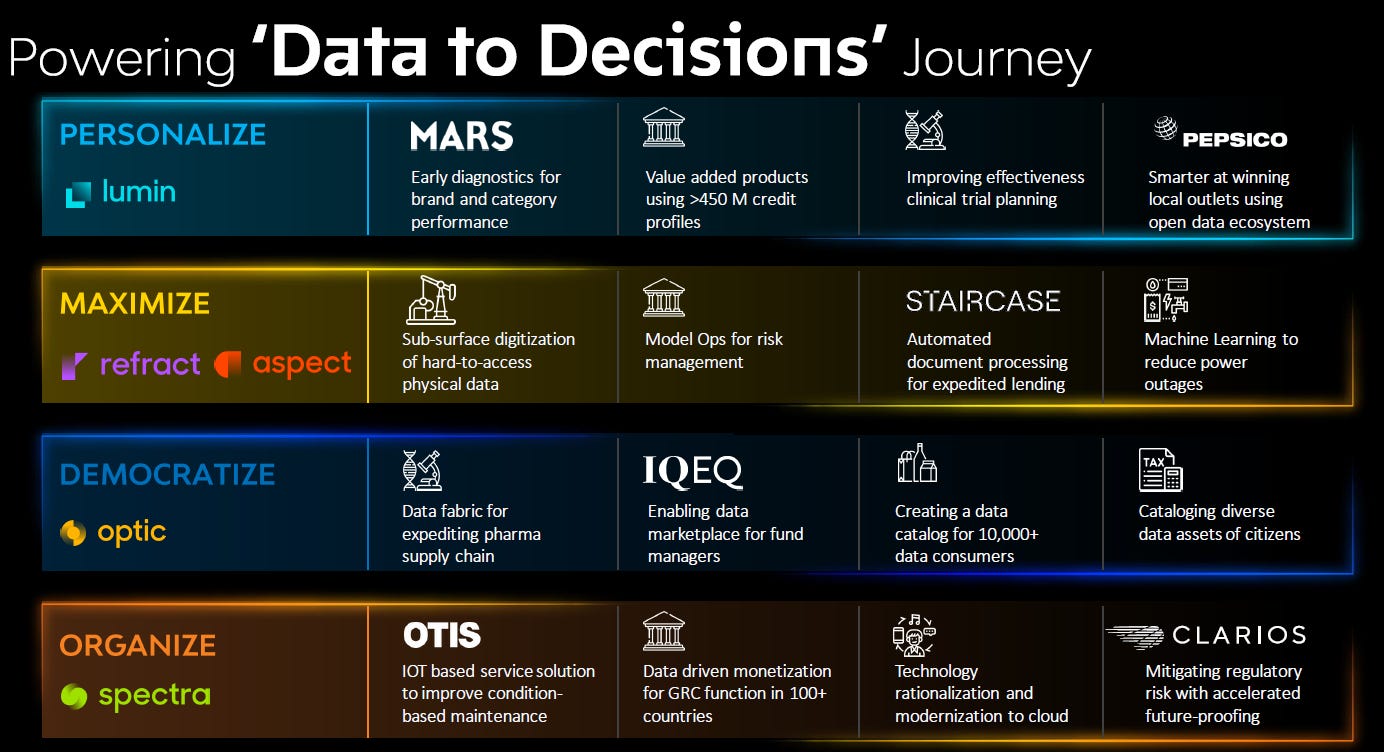

Unleashing the Value of Hidden Data

“Data is the new oil”. It’s valuable, but if unrefined it cannot be used. Oil has to be changed into gas, plastic, chemicals, etc to create a valuable entity that drives profitable activity; so must data be broken down, and analyzed for it to have value.

For most enterprises, over 80% of their data is unstructured. For some enterprises, it can be closer to 90% of their total data. Some call this unstructured data "dark data" because much of the value remains to be extracted. The true value, therefore, lies in extracting not only the value of structured information but also that of unstructured data.

Typically, 60–70% of companies’ total spending is towards organizing unstructured data. ‘Aspect,’ one of the five products under Fosfora—a Data Products unit of LTI, is built to address this.

The convergence of Big Data and Artificial Intelligence is the single most important development that is shaping the future of how firms drive business value from their data and analytics capabilities.

Artificial intelligence and Machine Learning are very data-hungry. Huge amounts of data are needed to train AI models. The challenge comes from turning big data assets into valuable machine learning training models. Unlike oil, big data-powered AI is available to any organization that can create a strategy for collecting quantities of unstructured and structured data suitable for machine learning and appropriately refining that data to extract increasingly more value from it over time. Doing this right is part of what will power companies to the next evolution in their digital transformation strategies.

Many decisions across enterprises are still being made based on instincts, rather than data-driven insights. With the Great Restructuring, LTI believes democratization of data, and democratization of decisions will be the top priority for every enterprise to be a Data-driven Enterprise.

LTI with its Data Products enables enterprises to undertake quantum leaps in business transformation and bring an insights-driven approach to decision-making. It helps deliver pioneering Analytics solutions at the intersection of the physical and digital worlds.

By 2025, there will be over 100 zettabytes of data stored in the cloud. To put this in perspective, a zettabyte is a billion terabytes (or a trillion gigabytes).

In the same year, the total global data storage will exceed 200 zettabytes of data, meaning that around half of it will be stored in the cloud. By comparison, only 25 percent of all the computing data was stored this way in 2015.

In the information economy, data is the byproduct of our advancement. Data is both the inputs and the outputs of our technology organism. Like oil, data can be dirty, but unlike oil, it can be cleansed with more data.

The full potential of data and other such transformative technologies cannot be realized on legacy mainframe infrastructure, hence the need for Cloud Migration—Cloud migration is the process of relocating an enterprises’ data, applications, and workloads to a cloud infrastructure. An enterprise may choose to relocate all of its computing assets to a cloud; however, in most cases, some applications and services remain on-premise. Enterprises typically migrate workloads to a cloud to improve operational performance and agility, workload scalability, and security.

Cloud—The Mitochondria of Digital Transformation

While the cloud is not a prerequisite, it does act as a force multiplier.

Just taking legacy applications and moving them to the cloud—“lift-and-shift”—will not automatically yield the benefits that cloud infrastructure and systems can provide.

Enterprises are turning to cloud infrastructures to accelerate their digitization plans to spur innovation, hone go-to-market strategies, and enhance customer experience. Companies are leveraging the elasticity of the cloud to accelerate development projects to introduce new services and products in their respective markets.

Another major driver of cloud migration is the Internet of Things (IoT), which aims to connect devices with other devices and humans to collect, review, and act on data in myriad ways. As it expands, the IoT will depend heavily on cloud infrastructures to process, store, and analyze the massive volumes of data captured by sensors, trackers, and monitoring devices in a wide variety of settings. Enterprises looking to kickstart their IoT implementations naturally are turning to the cloud to accelerate their deployment plans.

To enable cloud migration, LTI has a dedicated unit —aLTus. aLTus powers LTI’s end-to-end cloud transformation solutions and services that help organizations implement complex global-scale transformation programs.

LTI has built strong Tier-1 partnerships with AWS, Azure, Google Cloud, IBM, Snowflake, and ServiceNow. The company has built dedicated GTM and competency teams for each of these partnerships. LTI believes it now has industry-leading capabilities in both the Cloud and Data spaces, which now account for 40% of its revenues.

LTI has productized its service offerings across the life cycle of cloud transformation. These offerings are platform-enabled. LTI’s Infinity platform is a complete suite of modern engineering tools and processes, which helps clients with cloud lifecycle assessment and management to devise the right cloud migration strategy and provide agility to accelerate cloud adoption and transformation journey. The platform is equipped with efficiency kits that deliver plug-n-play capabilities, supporting heterogeneous tools available in the enterprise ecosystem. This platform is built to provide speed, scale, and consistency to enterprises’ cloud migration.

When it comes to the cloud, we have barely scratched the surface—less than 1/3 of the workloads are on the cloud. Some tend to focus on current IT spending which is over $2 trillion and how much of it will migrate to the cloud. That understates the cloud's potential. It’s the new workloads that don’t yet exist today that will power the growth of the cloud.

Just as the Roaring 1920s led to a rise in living standards, the advances in the 2020s from the Cloud, constructed from silicon building blocks, will do the same.

The confluence of three key technology spheres—machines, information, and materials—is behind the innovation of new products and services. In the 20th century, after policy-driven setbacks due to the Great Depression and World War II, people benefited from machines such as automobiles, power plants, and manufacturing plants. Radio, television, and telephones gave them information. Materials such as plastics and high-strength concrete enabled new products.

These same technological spheres are working in the Roaring 2020s to produce innovations. For machines, the world has 3-D printers, semiconductor chips, and nanotechnology, For information, we have microprocessors and vast data centers. For materials, we have algorithms that design new pharmaceuticals and bioelectronics to be customized to individual needs. All these are essential components of the Cloud.

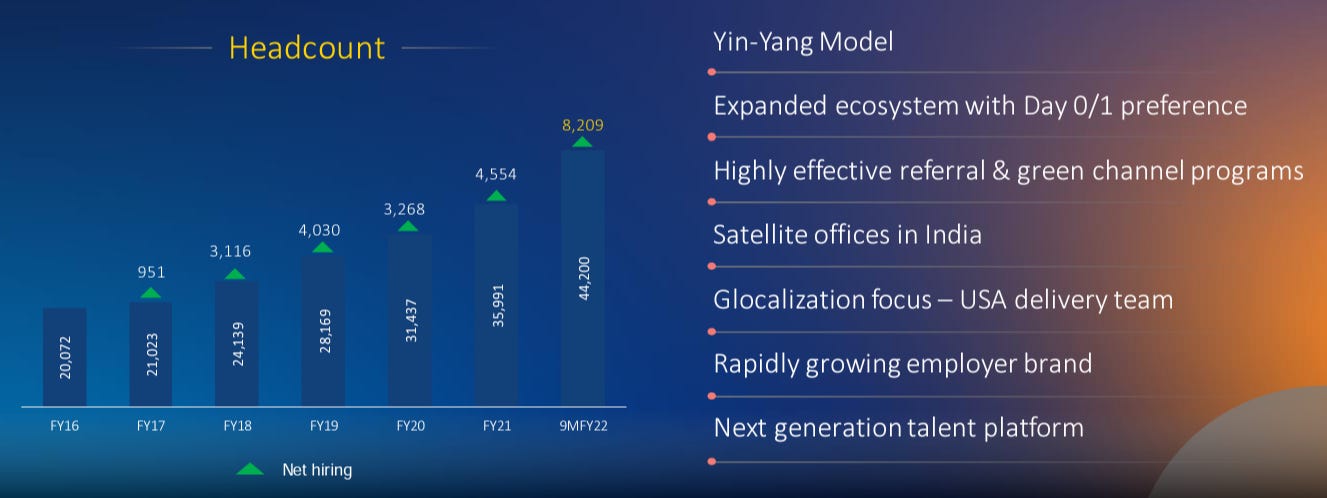

Winning the Battle of Talent

With great demand comes great challenges. One such challenge for IT companies is talent. There is an ongoing battle of talent. Attrition is going to the moon! Though many IT companies are indicating it will stabilize soon!

When there is humongous demand, whichever company can mobilize the largest and high-quality talent will capture the most value.

LTI claims that they are well prepared to win the battle. They have a strong parentage that they can leverage. They have taken other initiatives as well such as AI-based tools to match skills with job requirements. LTI has designed an enhanced talent management system that uses intelligent algorithms to retain and expand the talent pool. In addition, they have recently launched a comprehensive learning platform for its employees, called ‘Shoshin School’—the Japanese term means ‘beginner’s mind’ in Zen Buddhism—with an emphasis on having an open mind and avoiding preconceptions.

LTI’s utilization levels (proportion of staff doing billable work) are at an all-time high and they continue to hire to support their industry-leading growth.

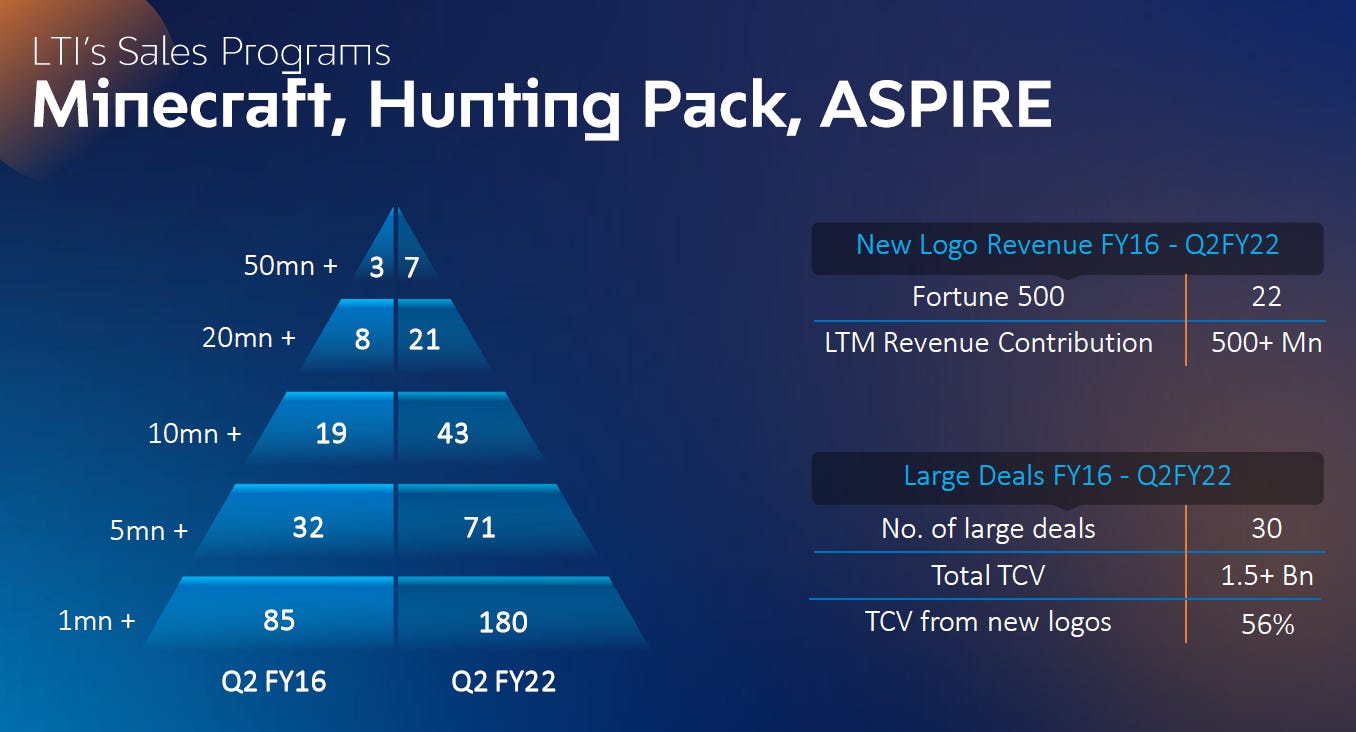

Sell it like wolves!

Contrary to the industry sales strategy of ‘2 in a box’ (sales & delivery) or ‘3 in a box’ (sales, delivery & a consultant) to drive sales, LTI focused on a ‘hunting pack strategy’. This involved practice sales, business units, delivery units, large deal teams, and alliances teams to collectively drive growth across existing and new logos. Sales & Marketing process automation and decision science were applied to measure pipelines and conversions accurately. Adequate flexibility, measurement, and control were exercised to drive sales discipline in focusing only on strategic accounts, penetrating through digital & analytics, and maintaining margin discipline while doing deals.

When Life (Industry) gives you Lemons (High ROCE), Make Lemonade (Grow)

Despite a highly competitive and fragmented market—the IT industry is blessed with high ROCE and high cash flow conversion. Almost everyone in the industry generates returns far exceeding their cost of capital. When this is the case, a company creates far more value if it grows faster than being able to operate more efficiently. A change in growth rate from 15% to 20% will create a lot more value than ROCE moving from 30% to 40%.

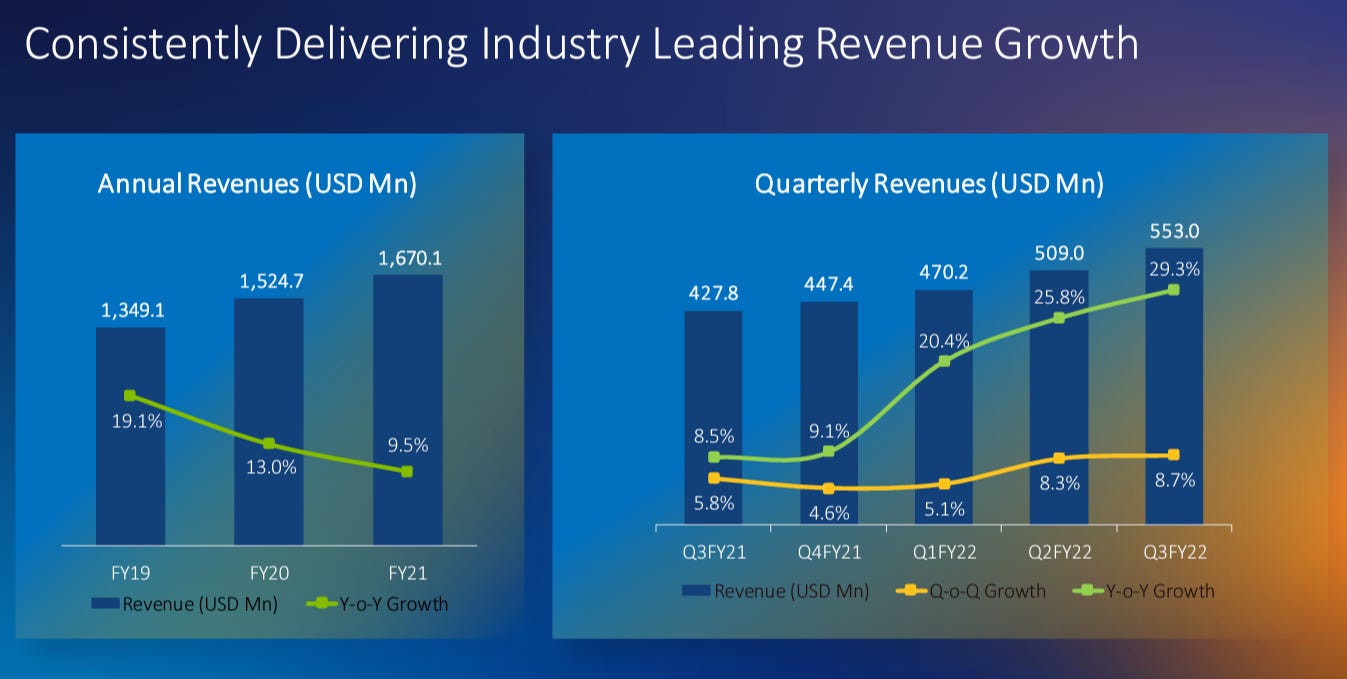

LTI has grown its revenue in the last 5 years at a CAGR of 13.5%, while industry growth was in the high single digits; EBIT at 23% CAGR; Net Profit at 18.3% CAGR.

Even now when the industry growth has accelerated to the low-mid double digits, LTI is growing at 18-20% which is above the industry average. Along with this growth, they have maintained an industry-leading ROCE of 40-45%.

LTI can continue to grow faster than the IT sector average because it has been more nimble and it comes from a “build” culture. Many customers are seeking new entrants and they seek the digital DNA. The more LTI enables its clients to compete with digital giants, the more it will be successful.

Pretty much every large contract that LTI wins today competes with bigger companies. The opportunities are quite promising for smaller service providers as they can be faster, and offer more cost efficiency compared with their bigger competitors. Many of them are even able to bring decision-making closer to their customers, thereby providing a better experience. LTI can offer similar capabilities and geographical presence as the larger companies. Hence on several occasions, they are more preferred than their larger competitors.

“I might not have the balance sheet to bid for a billion-dollar deal, but I have the capability to bid for a $200-300 million deal because now we are a $1.6 billion revenue company.”

— Sanjeev Jalona

There has been a recent trend in the IT industry of multiple smaller deals rather than single large ones. This opens up the market for relatively smaller firms like LTI. LTI’s sweet spot—orders ranging from $25 million to $200 million. And they have been winning a fair bit of it.

LTI along with several large IT services firms have earned economic moats due to switching costs and intangible assets. Given the intimate and often mission-critical nature of work performed by IT service providers. In addition, an established relationship frequently enhances an IT service provider’s insight into the client’s operations and emerging technology trends that will most affect the client. This dynamic leads to decades-long relationships given the relevance and timeliness of solutions. A trusted IT service partner can also gain additional business via word of mouth, and brand is very important in this respect. A successful track record reinforces repeat business and ongoing, sticky relationships.

Scale begets scale. The size of a company’s global delivery model can have a significant bearing on the scale and value of contracts it secures. There are only a few global players that can provide full end-to-end IT services solutions for the world’s largest multinational corporations. LTI has a presence in over 30 countries. The ability to change global processes in a fast and efficient manner generally translates into higher-end client engagement and better financial performance.

LTI has a clear sales strategy going forward… They call it—the CHIP Framework. The first strategic program of which is to consolidate and grow existing areas of strength.

Next, is to harvest existing high-growth engines—Cloud, Data, Digital led Cross Sales.

And the last one is to Incubate new growth engines—Digital Solution (Green Energy, EVs, Metaverse)—Next Generation Alliance with companies such as Freshworks, Lookr, and Xceptor.

Going ahead, growth does not seem to be a hindrance for LTI. If they can manage the supply side well, they’d be just fine.

Worth the Wave?

LTI has a market capitalization of a little over 1,00,000 crore as I write this. With sales of around 14,500 crores, which I believe can grow by around 15% for the next 5-7 years, with operational efficiency—operating profit growth a little faster than revenue, say, around 17%. Currently, they re-invest around 50% of their profits back into the business which I see declining as they scale and mature—which means they will compound free cash flow at a faster rate than operating profit, say, around 18-19%.

L&T’s Group acquisition of more than 60 percent stake in Bengaluru-based IT services provider Mindtree in 2019 has raised the expectation that LTI could add over a billion dollars in revenue in one stroke. Built by former Wipro executives, Mindtree is a respected brand, with a strong portfolio of global customers. Many expect that it will be folded into LTI at some point.

The group has stated that these companies will continue to operate independently at this point, so we remain focused on creating value for our stakeholders….

Technology is a mega-billion-dollar opportunity, with ample room for growth for all group companies. The markets and capabilities of these companies are highly complementary and we don’t compete in the same space. Instead, we collaborate synergistically wherever needed.

— Sanjeev Jalona

In your judgment, is LTI the surfboard to ride the digital transformation wave? Let me know.

Thank you for reading, see you soon!