The Business of Alcoholic Beverages- A Highly Regulated Industry with a Complex Structure

Want to know how to make money? The answer, it seems, could be resting at the bottom of a glass.

Welcome to Neel’s Newsletter by me, Neel Chhabra. If you aren’t subscribed and are curious about the Craft of Investing and Living Life in a Multidisciplinary way, join this insatiably curious community by subscribing here:

If you think your friends would like to read the newsletter, please share it with them.

The Business of Alcoholic Beverages- A Highly Regulated Industry with a Complex Structure

“Almost anything can be preserved in alcohol, except health, happiness, and money.” - Marry Wilson Little

I don’t know about health and happiness but investors can preserve and grow their money in alcohol. Thanks to an expert called Lindy!

Innovation and change are the lifeblood of progress. The stories that people tell themselves and the preferences they have for goods and services don’t tend to sit still. They change with culture and generation. They’re always changing and always will. Social trends, demographics, disruptive technologies, product innovation, etc, are important factors, that can bring about large shifts in value migration. They require the use of mental models that fall outside the normal use of “spreadsheet” growth rates.

The Lindy Effect is the idea that non-perishable objects, ideas, or technologies are expected to live proportionally to their current age. If something has lived for X years, it can be expected to live for another X years. Because every additional period of survival implies a longer remaining life expectancy, expected mortality decreases with time. If an effective judge of quality is whether it has withstood the test of time, then ‘consumption of alcohol’ certainly has withstood the test of time.

Alcohol is a spin-off from a form of warfare: yeasts use it as a chemical weapon in their competition with other microbes. The sugar-rich environment of ripe fruits is a tantalizing food source for organisms ranging from bacteria to primates. So much so that yeasts use the relatively inefficient process of fermentation to metabolize the sugar, because it produces the waste product ethanol, which poisons competitors.

Humans first consciously exploited this around ten millennia ago: the oldest archaeological evidence of alcohol production is a pot shard dated to that time, from Jiahu in China. For some 9,850 of these years, fermentation must have seemed a mysterious, even mystical transformation — until, in 1857, French microbiologist Louis Pasteur revealed that yeasts are responsible.

Fermented grain, fruit juice, and honey have been used to make alcohol (ethyl alcohol or ethanol) for thousands of years.

Fermented beverages existed in early Egyptian civilization, and there is evidence of an early alcoholic drink in China around 7000 B.C. In India, an alcoholic beverage called sura, distilled from rice, was in use between 3000 and 2000 B.C.

The Babylonians worshiped a wine goddess as early as 2700 B.C. In Greece, one of the first alcoholic beverages to gain popularity was mead, a fermented drink made from honey and water. Greek literature is full of warnings against excessive drinking.

Several Native American civilizations developed alcoholic beverages in pre-Columbian times. A variety of fermented beverages from the Andes region of South America were created from corn, grapes, or apples, called “chicha.”

It is remarkable that where not disallowed by religious beliefs, alcohol consumption has remained prevalent in so many human cultures.

Alcohol use in India—as well as rules and guidelines about who could drink and when—dates back to the pre-Vedic era. Archaeological findings and references in the Vedas indicate that a) the pre-Vedic Harappan civilization was well-versed in the production of toddy from palm trees; b) in the Vedic era (1500-700 BCE) the Gods and humans imbibed alcohol freely, with Some being referred to as a drink of Gods and sura – a form of beer – popular among the general population; c) alcohol was produced from flowers, grains, and fruits; d) women and brahmins were forbidden from drinking; and e) despite the widespread use of alcohol—even by priests and Gods—the Vedas labeled it “one of the seven sins.”

This tradition of drinking as well as the ambivalent attitude to it persists. Alcohol prohibition is one of the Directive Principles of the Constitution of India.

In ‘The Theory of Moral Sentiments’ (1759), Adam Smith showed our moral ideas are the product of our nature as social creatures. Morality is part of our very nature and benefits us and society. We have in-built moral standards to guide us. The state shouldn’t concern about the morality of its citizens. It should focus on rules of justice to protect individuals from harming one another. In its regulation of alcohol, the Indian state does just the opposite. It uses significant state capacity to police the morality of its people while being lax on rules of justice.

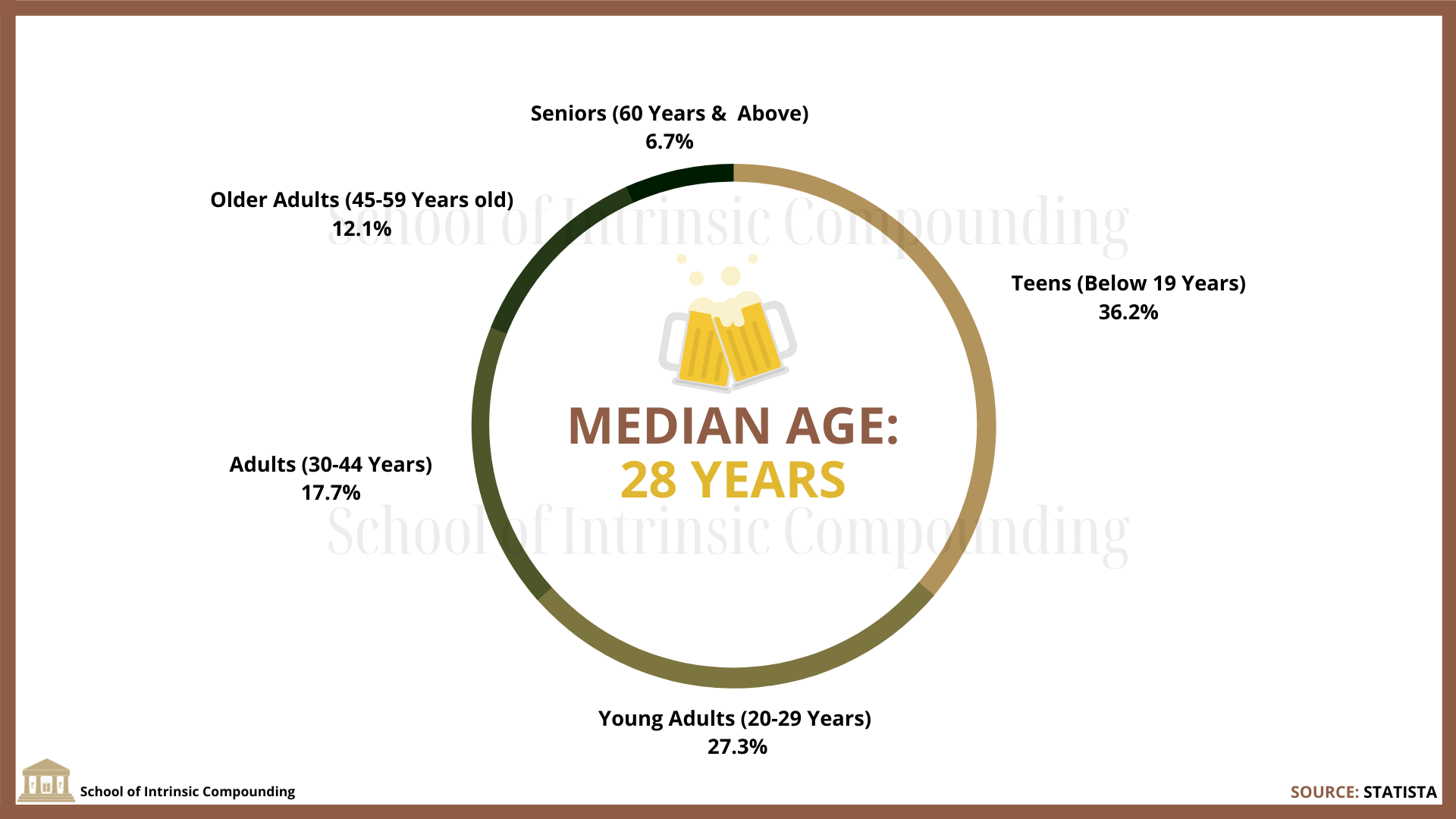

Absence and presence have very primal effects upon us. Too much presence suffocates; a degree of absence spurs our interest. We are marked by the continual desire to possess what we do not have—the object projected by our fantasies. The more distant and unattainable the object, the greater is our desire to have it. In general, the mind operates by contrast. We can formulate concepts about something by becoming aware of its opposite. The brain is continually dredging up these contrasts. What this means is that whenever we see or imagine something, our minds cannot help but see or imagine the opposite. If we are forbidden by our culture to think a particular thought or entertain a particular desire, that taboo instantly brings to mind the very thing we are forbidden. Every no spark a corresponding yes. We cannot control this vacillation in the mind between contrasts. This predisposes us to think about and then desire exactly what we do not have. Alcohol is something that is somewhat forbidden in Indian culture. With around 42-45% of the Indian population still below the age of 25, this phenomenon will aid the alcohol beverage industry growth to gallop as 17-19 million new consumers come into the legal alcohol drinking age (21 years) every year. But, that’s just the legal drinking age, ask 16-21 years young adults, and they couldn’t care less about such a thing called “Legal Drinking Age”.

The result is that alcoholic beverage brands are not just looking at what is; they are investing based on what can be.

India has a young working population which will continue to drive both income and consumption in the long run. Unlike many aging nations in the West and East, India will remain a nation of the young with a median age of 31 in 2030.

“With social barriers to enjoying a drink being discarded, increasing economic prosperity and 19 million new consumers entering the legal drinking age each year (in India), the overall economic and demographic opportunity is extremely attractive." - Amrit Thomas, former chief marketing officer, Diageo India

Okay but, “Show Me The Money!”

Living systems cannot be fully separated from each other. Every company is part of an industry that is part of a sector that is part of a national economy that is part of a global economy. Nothing exists in isolation. Everything is connected. The ecosystem lens reveals that the actions of anyone species have consequences for many others in the same environment. Many systems can take care of themselves, possessing abilities to correct and compensate for changes and external pressures. We need to take the time to learn how the components of our system are interconnected, so we can understand how our actions will impact the connections and affect the outcome we are trying to produce.

“Understanding our relationship with alcohol is about understanding our relationship with everything—with the chemistry of the universe around us, with our own biology, with our cultural norms, and with each other. The story of booze is one of intricate research and lucky discoveries that shape, and are shaped by, one of our most universal shared experiences. The human relationship with alcohol is a hologram for our relationship with the natural world, the world that made us and the world we made.” - Adam Rogers

I guess I should explain what Alcohol is before I do anything else…

In chemistry, alcohol is an organic compound that carries at least one hydroxy-functional group (−OH) bound to a saturated carbon atom. (Sighs!) The word “alcohol” derives from Arabic al-kuhul and is applied to the many members of the family of alcohol. The type found in beverage alcohol is called ethanol or ethyl alcohol and is the result of the natural process of fermentation of fruits, grains, vegetables, plant matter, and even dairy products. Its three main classifications are wine, beer, and distilled spirits. Other classifications abound and are often related to culture, content, production method, and legality.

Thanks for the etymology, Aristotle. So, how is alcohol made?

The alcohol found in wine, beer, and hard liquor is ethanol, the same stuff that powers alternative-fuel vehicles. To make ethanol (alcohol), all you need is a sugary (high carbohydrate) feedstock like grapes, corn, or malted barley, plus water and yeast. Yeasts are microscopic organisms that metabolize the carbohydrates in the feedstock and produce two by-products: ethanol and carbon dioxide. The carbon dioxide produced by yeast is what makes bread dough rise. To encourage ethanol production, brewers cover vats of fermenting material and allow only the carbon dioxide to escape. Wine, beer, and other fermented brews—like the grain mash that’s used to make whisky – can be distilled to concentrate their alcohol content, creating more potent spirits like gin, vodka, brandy, and rum.

What’s brewing?

Beer is the fermented, alcoholic product of the careful combination of water, malt, hops, and yeast. That’s it. And put simply, “brewing” is the practice of regulating the interactions between water, starch, yeast, and hops so that the result is what is called beer. In a sense, “brewing” is really about doing as much as possible to influence the results of a process that’s entirely hands-off: fermentation. We can brew beer for one reason: single-celled organisms called yeast, most often the Saccharomyces cerevisiae or Saccharomyces pastorianius variety, like to metabolize starch-derived sugars into ethyl alcohol and CO2. When we brew a beer, we are preparing a certain amount and variety of grain to produce those sugars, and then adding yeast so they can feast and create alcohol. Alcohol in a beer is often recorded on the label as “ABV,” alcohol by volume.

Talking of ABV, Spirits are the highest ABV products of the yeast-based fermentation of a liquid brewed to have fermentable sugars. Unlike beer or wine, however, spirits are the product of a second step called “distillation” that further fortifies them.

But why do we have to distill hard liquor? Why can’t we just keep fermenting it to higher and higher ABVs?

The basic concept of distilling is simple: making harder alcohol from a lower alcohol base. As often happens in the science of booze, it’s all about the yeast. As the yeast eats up the sugars (to make beer or wine, e.g.), they create alcohol and CO2, delightful waste products. But the more alcohol and CO2 they create, the less sugar there is for them to feed on. And at a certain point (around 14 to 18% ABV), the alcohol levels become toxic for the yeast. To create anything substantially “hard,” we can’t rely on yeast. To get high ABV alcohol, we have to physically separate alcohol from water using evaporation and condensation—distilling.

Because alcohol has a lower boiling point than water (173 F vs. 212 F), distillers can evaporate the alcohol (mostly) by themselves, collect the vapors into a tube and use cold temperatures to force the alcohol to condense back into liquid. The art of distilling is making sure you get the right amount of alcohol and any desirable congeners or flavoring compounds into the final product.

What is the sequence of activities that most of the companies in the industry perform?

For that, we’ll have to create a map of the industry’s value chain.

The alcoholic beverage industries have important backward and forward linkages. The backward linkages include the use of agricultural raw materials, capital equipment, transportation, and energy, while the forward linkages relate to access to markets, that is, distribution via retailers, wholesalers, and hotels, restaurants, and cafes.

There is a direct relationship between the agriculture sector and the alcoholic beverages industry as it provides relevant raw materials for the manufacture of all varieties of alcoholic drinks. For instance, beer is made with grains that are unfit for human consumption, such as barley and wheat, and is mixed with hops to add flavor. When the grains and sugar have been malted and brewed for a certain time, additional grains and other ingredients are added for color, flavor, and clarity. Wine is usually made from grapes, but other fruit or vegetables can be used too. As the sugar in the fruits or vegetable ferments, the resulting liquid is wine. Distilled spirits can be made by fermentation of the widest variety of ingredients to produce food-grade alcohol, commonly referred to as Extra Neutral Alcohol (ENA). These include grains for whiskey, sugarcane syrup and molasses for rum, and different fruit and vegetables for vodka and gin. The exact recipes for alcoholic drinks vary according to the alcoholic content, flavor, and texture.

The bulk of ENA being produced in India is from sugarcane molasses (74%) because molasses prices are lower and the process of conversion is also simpler. It is also made from grains (26%) which primarily comprises broken rice, millets (baajra), ground wheat flour (atta), jowar, etc.

The movement of ENA, which is 96 percent ethyl alcohol, is the most heavily regulated raw material. The process of procurement involves taking a series of permissions and approvals from the excise department.

The process of conversion of raw material into the final product that finds its way to the final consumer, involves many procedures.

Molasses-based products and grain-based products have different models of production and operation; therefore, there are two kinds of distilleries for the respective raw materials.

Molasses-based ENA may be produced at the sugar mill where there is an integrated distillery or molasses generated after sugar production may be transported to a distillery elsewhere for producing ENA. The alcohol manufacturers procure molasses-based ENA from these distilleries as a raw material for making their products, at the bottling plants. Usually, Distilleries attached to the sugar mills manufacture molasses-based ENA and sell it to the bottling and blending units for making the final products.

The other kind of ENA used for making alcoholic beverages is made from the fermentation of grains that are unfit for direct consumption. The distilleries may be standalone (without the bottling facility) or integrated (with a bottling unit). Grains are procured from the open market directly. Grain-based distilleries typically operate in the major grain-producing states, like Punjab, Andhra Pradesh, and Telangana. Manufacturers using grain-based ENA for their products usually have an integrated distillery and bottling plant.

This is how an Integrated Manufacturing Process looks like.

Irrespective of the source and raw material of ENA, the next step in the production chain is blending the ENA with different substances and water (The choice of substances required for blending with ENA depends on the desired final product. For instance, whiskey requires an ENA blend with malts or flavors, brandy is ENA plus grape spirit or flavors, rum is ENA and sugarcane juice or rum spirit or flavors, and gin is ENA plus flavors. Vodka is just ENA diluted with water., to bring it to the required flavor and strength depending on the final product.)

This is followed by bottling, labeling, and packaging, which happens on the assembly line. Once the bottles are packed in cartons, they are stored in bonded warehouses, meaning, excise duty is yet to be paid on the manufactured products. State excise mandates that the final products are allowed to leave the bonded warehouses (usually located within the factory premises) for the market only upon paying excise duties in full. The production process is similar for beer and wine as well, except that breweries and vineries respectively have integrated manufacturing units with the entire process happening in the same premises.

The next leg is the distribution of the final products, which happens through distributors in all the states. The distribution channels are different across states in India, but broadly of three types. The first type of channel involves only private distributors or wholesalers like in Maharashtra and Haryana. The second, where the distributor is a state government-run corporation like in Karnataka. The third, where private distributors and government corporations coexist, like in Delhi. The distributors are responsible for routing the final products from manufacturers to domestic retailers and for exports. Domestic retailers are of two types – off-premise (retail shops) and on-premise (hotels, restaurants, and pubs). Canteen Stores Department (CSD), a central government enterprise, is a distributor of alcoholic beverages as well. It caters specifically to the Armed Forces, which includes officers, defense personnel, their families, and ex-servicemen. This is the general supply chain of alcoholic beverage products, from the manufacturers to the consumers.

Online Liquor Sales – A New Route To Market Opportunity

In the context of the COVID pandemic and to make up for the loss of sales with consumers refraining from going for liquor purchase, many state governments have allowed home delivery of liquor. Home delivery is made by retailers directly and also through agencies like food aggregators and standard technology platforms. In long run, this may help in increasing industry revenues as many consumers, particularly women, are not comfortable going out to buy liquor from shops.

Alcoholic Beverages in Consumeristaan

India represents one of the largest consumer markets globally with significant growth opportunities due to its low current per capita consumption. Income growth will transform India from a bottom-of-the-pyramid economy to a truly middle-class-led one, with consumer spending growing from $1.5 trillion today to nearly $6 trillion by 2030.

One of the key reasons for this growth is the expansion of the high middle-class income groups and the decline in the number of households below the poverty line. Given the large domestic consumption propensity, the economy is relatively resilient to the external disruptions and down cycles of public investments.

There is a dramatic income churn currently underway: the proportion of those with incomes in excess Rs. 25 lakh has increased from 1% of the Indian population in 2005 to around 3% a couple of years ago and likely to be 7% by 2030. But there is a bigger movement happening below this population segment: the middle segment of India’s population (often referred to as the ‘bulge’) which earns between Rs. 2.5 lakh and Rs. 25 lakh per annum, has increased from 30% to 54% and likely to grow to 78% in a decade from now.

Internet access will be democratized by 2030 (perhaps earlier) with more than 1 billion Indians – rural and urban, old and young – on the internet, a truly remarkable achievement in terms of inclusion. With the access to internet and mobility, this young population is well-informed and is aspirational. Growing exposure to the internet and other forms of media has resulted in a higher influence of western culture leading to a growing acceptance of alcoholic beverages in social gatherings. All this supports the case for strong consumption growth in India and presents significant opportunities to consumer products like Alcoholic Beverages.

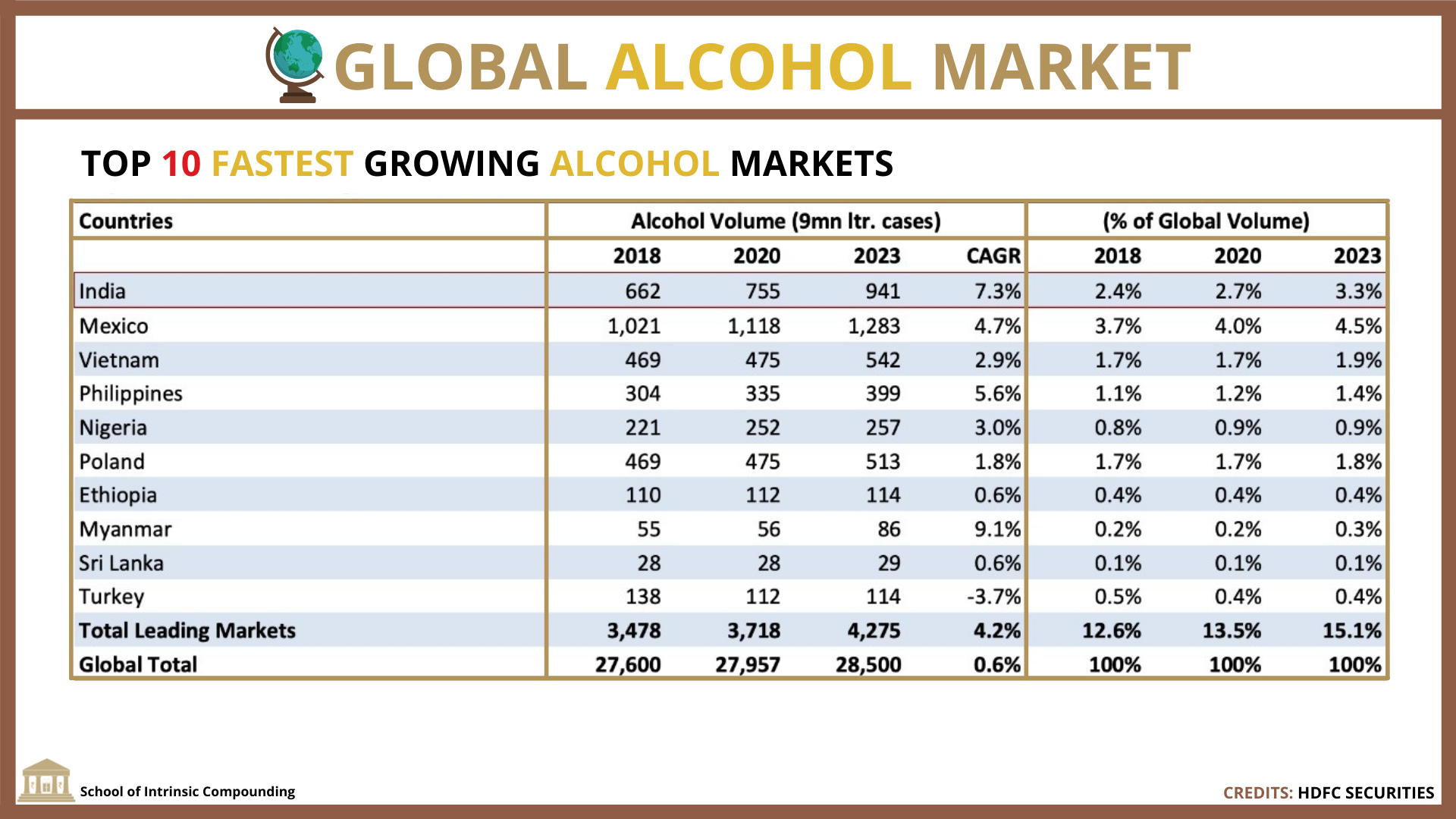

India is one of the fastest-growing alcohol markets in the world.

Alcohol consumption in India amounted to about 6.5 billion liters in 2020.

The steady increase in consuming these beverages can be attributed to multiple factors including the rising levels of disposable income and a growing urban population among others.

While metros and emerging boom towns continue to drive economic growth, rural per capita consumption will grow faster than in urban areas mimicking consumption patterns of urban counterparts. India is the fastest urbanizing country. Nearly 34% of the country’s population is urban; even as the country’s population base will continue to broad-base, the urban growth in percentage terms is likely to relentlessly increase to an estimated 40% by 2030. This increase is likely to strengthen the offtake of alcoholic beverages in India.

India is the world’s ninth-largest consumer of all alcohol by volume. After China, it is the second-largest consumer of spirits. India consumes more than 663 million liters of alcohol (spirits). It is fair to expect that per capita consumption will increase with changes in the lifestyle and aspirations of the population.

An average Indian male drinker consumes three times more alcohol than an average female drinker. More women in the workforce should lead to more consumption spending from women. The incidence of more working women—from 98.7 mn women in 2012 to 112.6 mn in 2018—is likely to catalyze alcohol consumption. This indicates that economic, lifestyle and social realities are converging to create an opportunity related to alcoholic beverage consumption in India.

While volume growth in the industry will be driven by rising per capita consumption, a strong premiumization trend will lead to value growth faster than volume growth.

Market Segmentation

Alcoholic beverages contain ethanol or ethyl alcohol, which is made by fermentation of natural sources of sugar like fruits, grains, vegetables, plant matter, and dairy products, with a catalyst that is usually yeast. As it ferments, the carbohydrates (starch and sugar) in the main source turn into carbon dioxide and ethyl alcohol. The final products can be broadly classified into distilled spirits, wine, and beer. Further classifications vary across cultures and geographies and are based on the method of production, raw materials, alcoholic content, and legality.

In India, for all practical purposes, alcoholic beverages can be classified into Indian Made Foreign Liquor (IMFL), Country Liquor or Indian Made Indian Liquor (IMIL), Foreign Liquor Bottled in Origin (BIO), Wine and Beer segments.

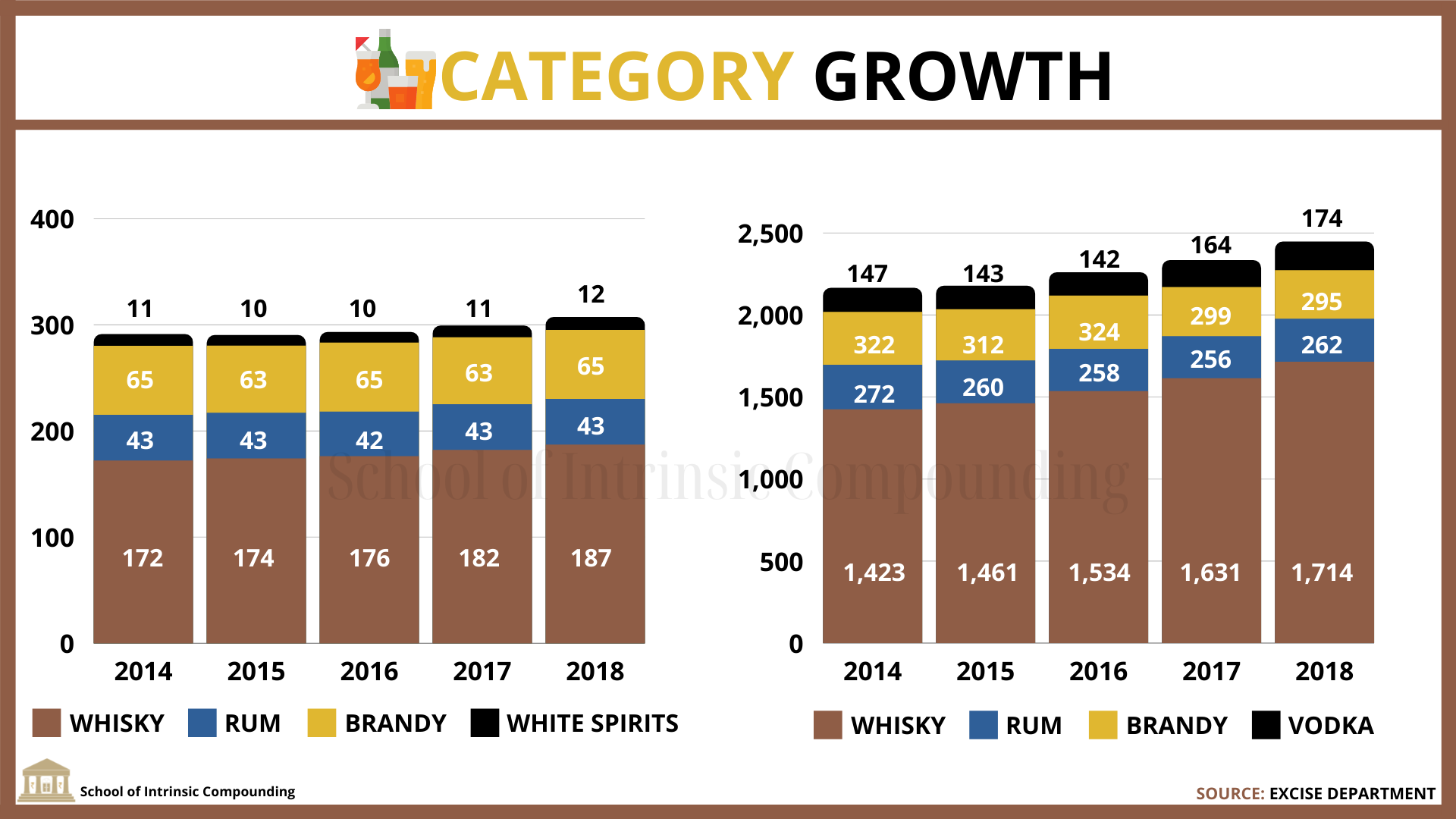

Indian Made Foreign Liquor (IMFL) constitutes the largest segment of the Indian liquor industry in terms of value, due to the price per bottle, making up ~72% of the total market by value. It is further bifurcated into Whisky, Rum, Brandy, Vodka, and Gin. 42.8% IMFL is made from Extra Neutral Alcohol (ENA; higher purity 96%).

IMFL category is dominated by brown spirits (whisky, rum, and brandy), with a combined market share of 95%. IMFL starts from Rs. 80 per nip (economy brands). Brand loyalty is high with the multiplicity of purchase options (Standalone retail outlets, department stores, and Government-owned shops in some states like Delhi) and has more affluent consumers. I have observed that brand loyalty tends to intensify as one moves up the premiumization ladder.

Whisky is decidedly the spirit of choice in India. We consume almost half the whisky produced worldwide. From the cheapest Indian-made foreign liquor (IMFL) variant—whisky makes for almost 60% of IMFL—to limited-edition single-malt Scotch, people are drinking more whisky today than ever, spending anywhere between Rs50 per 25ml peg for a McDowell’s at a Paharganj bar in Delhi to Rs 1,500 for a small Johnnie Walker Blue Label at a five-star hotel.

“The whisky category is large and in growth. Consumers are increasingly opting for quality over quantity and prefer blends that appeal to the Indian palate,” - Neeraj Kumar, Managing Director, Beam Suntory India, which recently launched Yamazaki, Hibiki, Oaksmith Indian whisky and Roku gin. Suntory, the world’s third largest spirits producer, said these new brands will benefit from the distribution and customer partnerships serviced by Teacher’s and Jim Beam for the past many years.

India consumes 48% of the world's whisky. It is the fastest-growing market and the largest producer of the spirit.

“Though the entire alcobev (alcoholic beverage) industry has grown steadily over the last decade, whisky is the flag-bearer in India… The majority of consumers choose IMFL, rather than beer or wine, This is the segment that is largest in India." - Thrivikram G. Nikam, executive director at Bengaluru-based Amrut Distilleries Pvt. Ltd.

The importance of the Indian whisky market to the global well-being of the whisky category cannot be overstated: nearly one in every two bottles of whisky bought around the world is now sold in India, and seven of the top ten global whisky brands are Indian. India consumes more whiskey than any other country in the world – about three times more than the US, which is the next biggest consumer.

Per capita value consumption of alcohol is correlated to per capita GDP, which will lead to a premiumization trend in the alcoholic drinks industry driven by rising consumer demand for more authentic flavors, new experiences, and products that have fewer after-effects. Furthermore, manufacturers are also expected to expand their premium portfolios by introducing foreign brands or new brand extensions to India.

Similar to food and personal care categories, premiumization is a fairly large trend even in the Indian alcoholic beverage category. Where it differs, is in Route To Market (RTM)- total outlet reaches in India is limited only to 75,000-80,000 outlets on account of regulatory curbs and state interferences whereas any fast-moving consumer goods company will have it in millions. Consumers can trade up or down fairly easily, depending upon the macro environment. Millennials and GenZ consumers are also increasingly mindful of their choices and therefore demand for low or no alcohol beverages is fairly strong. Companies are leveraging this trend to the hilt with innovation and significant portfolio expansion in the value plus and premium segments. Trend such as occasion-based drinking where experience sits at the heart of the occasion is also leading to growth in the premium segment. In the spirits segment, several companies enjoy significant sales in the premium segment with market leader Diageo India (United Spirits) already enjoying sales over 65%.

93% of all whisky traded in India falls into the ‘value’ segment, and that leaves plenty of scopes to develop the higher-end segments. These new affluent consumers prefer premium products. Premium-priced variants give a better sensorial experience and are markers of aspiration for consumers. This is a long-term trend, with the average price of whisky in India nearly doubling in ten years to US$7.18 for a liter. This shows just how early in the premiumization cycle the market is in.

Among listed entities, Diageo-controlled United Spirits, the company which sells local whiskey, McDowells as well as Johnnie Walker, is the biggest player in the spirits market and holds 34% of the Indian scotch and whiskey market by volume. French rival Pernod Ricard commands 30% of the market with brands such as Royal Stag and Glenlivet. Even within the premium segment, Diageo and Pernod Ricard control more than 70% of the whiskey segment.

Three global spirits giants – Beam Suntory, Brown-Forman, and Bacardi – are collectively introducing more than a dozen new brands in the premium whiskey segment in India, which is the world’s largest whiskey-consuming nation. These three companies are among the biggest distillers globally.

Attempts are also being made to create a buzz around the use of whiskey in cocktails, making the category more relevant not just to younger drinkers, but also to the female market. Many of these new ‘young brands’ are helping to contemporize the category and broaden the appeal away from the 35-year-old plus core users to the rapidly expanding younger age segments. There is already evidence that in the higher echelons of Indian society, women are developing a taste for top-end whiskies.

White spirits, i.e. clear alcohol, are the fastest-growing segment in the IMFL category. White Spirits such as vodka and gin account for 3.6% of the total IMFL volumes and 6.2% of the value. Vodka is the most preferred alcohol among Indian youngsters. Vodka - originated in the Eastern European regions, namely Russia and Poland is a colorless and odorless drink that is usually crafted from potatoes or grains. It contains 35%-50% alcohol by volume and is typically consumed ‘clear’ or by itself. A few brands in India produce Vodkas, such as Magic Moments (Radico Khaitan), Absolut (Pernod Ricard), and Smirnoff (Diageo India). The industry’s focus on premium brands has enabled manufacturers to identify relatively less price-sensitive consumers that ultimately drive value growth. The young and aspirational working population forms the core of this segment. Vodka industry growth indicates a strong premiumization trend. Increasing conversion from country liquor to branded IMFL given health issues associated with country liquor consumption present a growth opportunity.

Indian Made Indian Liquor (IMIL) or erstwhile ‘country liquor’ is an alcoholic beverage with ~30% alcohol content usually produced locally. Starts from Rs. 30-40 per nip (smallest size). IMIL is a flavored drink influenced by regional taste preferences. Popular flavors are fruit flavors, masala flavors, etc. This unbranded liquor is produced locally by micro/home distilleries and is available for sale in those regions. Feni, made from cashew or coconuts, is produced completely in Goa. Palm wine, made from the sap of palm trees, is popular in India. Arrack is another prevalent alcoholic drink made from coconut, sugarcane, or fruit sap. Consumption of this type of liquor is mostly among the blue-collar and lower-middle-class workers. Brand loyalty is low with high distributor power and price-sensitive consumer. The growth in this segment is expected to be driven by a growing consumer base, rising rural incomes, and consumption/conversion from illicit/toddy to IMIL.

Entry-level whisky is the most volatile space in the market. Those people who were consuming country liquor will slowly move up to entry-level IMFL.

Foreign Liquor Bottled in Origin (Imported Alcohol). Imported alcohol has a meager share of around 1% in the Indian market. The heavy import duty and taxes levied to raise the price of imported alcohol to a large extent. Alcohol is exempted from the taxation scheme of GST.

The pricing structure of imported liquor is contrived as it is the costliest category. Import of alcohol is subject to Open General Licence (OGL); anyone can import alcohol. Suppose one bottle of foreign-made liquor (750 ml) is imported into the country, it lands in India at Rs. 350. Import duty of Rs. 525 is paid to the central government for importing foreign liquor. After clearing the customs procedures, the bottle reaches Delhi at an excise bonded warehouse. The importer will now have to register a label for this bottle based on Delhi's excise rules. The importer will then bill it to a distributor-wholesaler, making a margin of INR 900 on the bottle, to cover his costs and profit on the bottle. The wholesaler will add his margin of Rs. 200-300 and the Delhi government will charge an excise duty of 65 percent on this distributors’ price. The retailer (off-premise consumption) makes Rs. 100 per bottle and pays a VAT of 20 percent at the time of sale. Therefore, the total price for a bottle of foreign-made liquor in Delhi comes to Rs. 3,500-4,000. This is the price paid by the consumer for the bottle, which landed in India at Rs. 350 (including the manufacturer’s margin).

Imported Alcohol is usually imbibed by the rich and upper-middle-class in metropolitan cities and is popular among young professionals and entrepreneurs who migrate from local brands to international brands. The number of outbound travelers from India is increasing, being introduced to global alcoholic beverage brands that are refining their consumption preferences. The number of international travelers from India was 14.9 mn in 2012; this increased year-on-year to 22.5 mn by 2018.

Wine is a fermented beverage produced from grapes and sometimes other fruits. Wine involves a longer fermentation process than beer and a long aging process (months or years), resulting in an alcohol content of 9%–16% Alcohol by volume (ABV).

The Wine market in India is small but growing; annual per capita consumption of wine in the country is a mere 9 milliliters, approximately 1/8000th that of France. The main reason for this can be attributed to the fact that Indian’s preference for hard liquor and beer boasts nearly 98% of the market share whereas wine with low Alcohol By Volume (ABV) only has a 2% market share. Wine companies are especially targeting urban women. Though champagne and other sparkling wines are gaining popularity, they are far behind in comparison with red and white wines. The major reasons for this upswing in wine consumption are: increase in the levels of disposable income, lifestyle changes, and exposure to international experiences. India imports wine from many countries, with France being the leading exporter, followed by Australia, the United States, and Italy. India has a small, but growing, production segment in wines. Viticulture in India has a long history dating back to the time of the Indus Valley Civilization when grapevines were believed to have been introduced from Persia.

Winemaking has existed throughout most of India's history but was particularly encouraged during the time of the Portuguese and British colonization of the subcontinent. The end of the 19th century saw the phylloxera (a pest) louse take its toll on the Indian wine industry followed by religious and public opinion moving towards the prohibition. Following the country's independence from the British Empire, the government encouraged vineyards to convert to table grape and raisin production. In the 1980s and 1990s, a revival in the Indian wine industry took place as international influences and the growing middle class started increasing demand for the beverage. By the turn of the 21st century, demand was increasing at a rate of 20-30% a year.

The city of Nashik in the state of Maharashtra is called the "Wine Capital of India." The major domestic players are Sula Vineyards, Grover Vineyard, Chateau d’Ori Vineyards, and Chateau Indage Vineyards. Tourism and marketing have boosted the wine market of India. The middle-class urban people are drawn to wine consumption. The penetration of wine consumption in India is estimated to be just 1–2 million individuals. Mumbai, Bangalore, and Delhi are the top consumers of wine in the country. Maharashtra and Karnataka have the largest vineyards for wine production in India.

There is a great potential in the wine industry, indicated by the per capita consumption of 4.6 ml per annum in India compared to the global per capita consumption of 4 liters per annum.

Beer is a beverage fermented from grain mash. It is typically made from barley or a blend of several grains and flavored with hops. Most beer is naturally carbonated as part of the fermentation process.

"Time stopped. The world pivoted. It seems like a small transaction - a guy walks into a bar, right? -it is the single most important event in human history. It happens thousands of times a day around the world, maybe millions, yet it is the culmination of human achievement, of human science, and apprehension of the natural and technical world. Some archaeologists and anthropologists have argued that the production of beer induced human beings to settle down and develop permanent agriculture - to literally put down roots and cultivate grains instead of roaming nomadically. The manufacture of alcohol was, arguably, the social and economic revolution that allowed Homo sapiens to become civilized human beings." - Adam Rogers on ordering a beer

In the alcohol space, beer is the most popular drink in India after spirits. However, for a variety of socio-economic and religious reasons, India’s current per capita consumption of beer still hovers around 2 liters which is well below the global average of around 30 liters, and Asia's average of about 27 liters. Such average low per capita consumption has a lot of room to grow in years to come given our population, climate, evolving attitude, increasing income, and demography.

Beer comprises about 12% of the total alcohol consumed in India. While the alcohol beverages industry in India has been dominated by spirits, beer remains the preferred alcoholic beverage for young Indians. Beer has registered robust growth in the last one and half decades. From a total industry consumption of about 100 million cases in 2005, the consumption crossed over 300 million cases in 2019. The current industry size is estimated to be over 320 million cases per annum. Three leading players contribute over 85% of the total industry sales with our United Breweries being the market leader having a market share of about 52%.

On basis of alcohol content, beer in India can be categorized into Strong and Mild Beers. Strong beer which has an alcohol content between 6% and 8% dominates the beer market accounting for over 85% of the total beer consumed in India. The Super Premium beer segment within both the Strong and Mild beer categories has been growing faster than the overall beer industry and has grown at a Compounded Annual Growth Rate (CAGR) of almost 30 percent over the last three years.

Modern craft beer came relatively late to India. The first Indian brewpubs opened in Pune (Doolally) and Gurgaon Ahirwal (Howzat) in 2009. Also around the same time, India's first bottled craft beers were launched by Martin Judd's brewery in Maharashtra, and Australian-owned "Little Devils" in Ghaziabad. While the bottling ventures proved short-lived and closed down within a year, brewpubs have since become a successful format and common sight, especially in India's large cities. In 2019, India counts more than 200 brewpubs, of which about 60 each are located in Bangalore and Gurgaon, respectively. There has been a major boom recently for microbreweries in India due to which more brands of beer are coming to India introducing us to its different flavors. The past few years have seen an explosion of craft beer brands in India. There’s Bira—the market leader—White Rhino, Witlinger, White Owl, and more coming up. The competition is fierce. Though it is helping in creating the ‘beer culture’ in India where whiskey dominates; anything that does the job quickly.

“The growing trend of microbreweries help in building beer culture… We are largely a liquor, spirits, whiskey country. So nominal rise in the number of brewpubs helps in creating bigger buzz and activity in the beer space.” - Shekhar Ramamurthy (Managing Director), United Breweries

The beer market in India has evolved from manufacturing usual beers such as strong and lager to flavored beers owing to the adoption of trends and technologies from western markets. Today, there is a presence of more than 140 beer brands in the Indian beer market, to address the palate of each customer segment. The type of yeast used to ferment beer distinguishes its different types. From classic Lagers to funky sour Ales, each type of beer is classified based on its fermenting process. Further, there is differentiation based on the flavor, color, and aroma of the beer. There are probably 1000s of different types of beer as it is brewed all over the world, which makes them nearly as diverse as wine.

In India, the beer sector is at its growth stage with competing companies in the market looking for further market expansion with the introduction of new products and by strengthening their distribution network. The market has been growing mainly because of youth, higher disposable income, rising preference for low alcohol beverages, and gradual social acceptance. Drinking in bars is fast becoming a social phenomenon in cities such as Delhi, Gurgaon, Mumbai, Pune, and Bangalore and with the emergence of craft beers, the growth in beer consumption increased rapidly.

Tom Russo on the Relative Merits of Beer, Spirits, and Wine

“In terms of capital allocation, I’m fairly agnostic between beer and spirits but have almost no direct exposure to wine as a category. I’ve always felt that the value add off of the commodity cost there and the pricing power that they enjoy in the wine industry just hasn’t been as rewarding as you get with spirits and with spirits increasingly where you can tier the pricing so sharply and aspirational consumers are willing to pay substantially more for components in the price hierarchy that don’t cost all that much more. And so there’s the possibility of tiering in a way that you really just don’t get with wine. And then beer compared to wine—the economics of beer at scale with dominant local brewers is just far more attractive than you ever find with wine because of the great production efficiencies and the scale advances that you get with brewing as opposed with a wine gathering and operation. So I prefer spirits and beer over time.”

A Highly Regulated Industry with a Complex Structure

The policies regulating alcohol in India continue to draw their moral inspiration from Bollywood films. Though the ‘taboo perception’ about alcohol is changing in India, ambiguous regulations are likely to keep the industry growth under check. Through the lens of Bollywood, alcoholic beverages have transformed from being a symbol of evil or bad things to being cool and fun! It is no more the drink of the antagonist, even the protagonist is spotted with alcohol, breaking the taboo of negativity around alcohol. Women who were portrayed as admonishers of alcohol have joined the party. Alcohol from being associated with deprivation and solitude has transformed into being associated with togetherness and happiness. Alcohol which was linked to failures and sorrows is now more of a celebration drink. The Bollywood protagonists are no more ashamed or shy of being associated with alcohol, signifying the underlying acceptance of alcohol over the years.

The industry, over the years, has changed from a seller’s market to that of a buyer’s market. With a variety of brands being available, major brand build-ups, media hype, and information flow have influenced the behavioral pattern of the consumers, who are more discerning and see value for money. India, as a nation, has undergone a sea change. At a time in the past when liquor was typically looked down upon, with changing lifestyles and urbanization of our towns and cities, it is no more taboo to be seen drinking. It has rightly or wrongly enhanced the status. Women and teenagers have started indulging in social drinking.

The consumer today has several choices in terms of liquor and brands. The liquor industry itself is highly segmented; depending on how much one can spend. Brands and prices are catering to each class of society. The market is highly competitive with many local and international players vying for a share in the market.

The modus operandi in distribution and sale can be broadly classified into three kinds – free market (license privately owned), auction market, and government-controlled. The distribution patterns and controls vary in each state/UT according to the respective governments' model. The distribution channels of a state also affect the pricing mechanism it follows.

There are primarily three types of markets in the liquor industry.

Government Market: Here the state government is the wholesale distributor of liquor and they purchase directly from the company. Through this kind of system, nearly 70 percent of the national volume is sold.

Auction Market: In an auction market, the state is split into many smaller geographical segments. The government auctions the right to distribute and retail liquor in those areas for a specific period, to private entities. This auction is based on the minimum guaranteed tariff payment to the government over the specified period. Wholesale operations and retail outlets are owned or operated only by those parties that win the auction for that particular area. The private entities that win the auction for a specific area subsequently negotiate with liquor manufacturers to acquire liquor at competitive prices. Typically, all auction winners enter into inter-state arrangements to procure liquor at the most competitive prices and retail the same at relatively higher prices to recover minimum guarantees committed by them to the government during the auction process. Some states like Haryana and Uttar Pradesh follow the auction market system where the state government auctions the wholesale and retail licenses to private players every year. The manufacturers then directly sell to the wholesalers who sell to the retail players; the total volumes sold through auction markets is 13 percent of the national volume.

Open Market: In an Open market, there is no government intervention in the pricing and distribution of liquor. The manufacturers sell liquor to the wholesaler or distributor who in turn sell it to the retail outlets. Market forces determine to price. The government issues wholesale or retail licenses for a fee. In the free market system prevalent in Maharashtra, Assam, and Goa, the private manufacturers are free to choose their distributors, who then have their retail networks for sale. It is estimated that 19 percent of the national liquor sale volume is through the free market system.

The state governments have adopted different combinations of these, based on what suits them (and purportedly the market) best, ease of supervision, and the opportunity to maximize revenue from excise.

For instance, in Jharkhand, the distributor is a government-operated entity while the retail licenses are auctioned to private players in the market. In Haryana, both wholesale and retail licenses are auctioned to the private. The governments have eased the licensing norms to encourage competition by having more market players. In Tamil Nadu, the government controls the distribution and retail and markets liquor through its shops. Karnataka shifted from an open market system and introduced KSBCL, a government-run distributor that controls the movement of all alcoholic beverages within the state boundaries, whether imported or produced domestically. The retail is licensed to the private sector as well as to Mysore Sales International Limited (MSIL), a Government of Karnataka marketing organization, which has liquor outlets in the state.

Factors like different tax regimes, different price determination models, different rules and regulations, and different levels of openness towards easing the business environment, have resulted in making India, not a single market for the alcoholic beverages industry, but 36 (28 states and 8 union territories) different markets. All the stakeholders – manufacturer, distributor, retailer, and consumer – can access products from other markets, though faced with restrictions. A product can be sold within the state market, exported to another state in India, or can be exported abroad.

The ease of doing business in the alcoholic beverages industry isn’t meant for the faint-hearted. You might need to fortify yourself with a drink or two before you dive into the byzantine maze of regulations.

Before the reforms of 1991, domestically owned companies dominated the manufacturing of alcoholic beverages. Post liberalization, the government allowed the entry of private foreign players into this segment, which led to increased competition. The manufacturers began focusing on improving their packaging and brand visibility and using better ingredients to make better products to build brand loyalty. Presently, India allows 100 percent FDI through the automatic route in distillation and brewing of potable alcohol. However, as a state subject, the business practices of manufacturers of alcoholic beverages, and the regulatory frameworks within which they operate vary.

Despite the growing significance of the alcoholic beverages sector since the 1990s, for its potential to generate revenues for the states, and the recent importance given to improving ease of doing business in India, the industry is rarely awarded the same importance that other manufacturing sectors receive. Instead, it continues to face a myriad of restrictive policies and complex, excessive regulations. Doing business comprises three stages of a business – starting a business, running a business, and closing a business. In the alcoholic beverages industry, the most difficult of these stages are running a business, and this holds for all the stakeholders including the manufacturers, distributors, and retailers. Every aspect of the value chain is controlled – production, distribution, pricing, taxation, consumption—with an infinite variety of laws across states. The cost of compliance is very high in this industry. [An alcoholic beverages manufacturing unit in Maharashtra is required to obtain over 10,900 licenses (including frequency) annually from different agencies for doing business.]

Governments earn a lot from alcohol. The industry is among the top revenue contributors for most states.

In India, as anywhere else in the world, alcohol is heavily taxed, due to the nature of the product. Owing to the high societal cost of alcohol consumption, especially in low-income nations, the overall tax on alcoholic beverages is kept high. Though the excise duty hikes are largely passed on to the consumer and price increases have been demand inelastic, the probability of a ban by a state government remains a key overhang for the Alcohol beverage sector in India.

In addition to taxes, price determination by state governments continues to be a major roadblock in doing business in this sector. In this respect, India is an outlier—all countries impose regulations on this sector, but barring India, no country imposes price controls where price increases (and decreases) have to be approved and granted by states. In all the states, the government determines the prices through regulatory mechanisms, which vary across states. It is common for states to deny manufacturers price increases intended to offset increases in manufacturing cost due to inflation or even levy changes.

The industry is a bizarre example of being subject to taxation and price controls – excise duties are hiked periodically, and yet it is difficult to get the manufacturers’ price increases to offset normal inflation.

Despite taxes from alcohol being a key revenue generator for a state, a few state governments have imposed a ban as a populist measure. It is to be noted that several states have also rolled back on the imposed ban. It gave rise to the consumption of Illicit liquor, which comprises all kinds of alcoholic beverage products produced and/or traded in an unregulated manner. Alcohol produced and sold illegally outside of government regulation is untaxed, circumvents restrictions around quality standards and availability, and depending on the procedures and ingredients used to make it, can even be potentially toxic.

The states collect more than Rs. 1.5 lakh crores in excise alone every year. If you add sales tax, commercial tax, and various cess, this number would easily double. A strange dichotomy runs through the alcohol economy. It won’t be owned, and it won’t be disowned. State governments, which often punctuate alcohol regulation with moral overtones, have no problem putting alcohol at the front of the queue in terms of priority in a moment of COVID pandemic. As the saying goes, “it is hard to say no to the lighted cigarette and the money coming in.” The reasons are obvious: India’s states, put together, earned about ₹2.25 trillion from taxes on alcohol in the most recent fiscal year. For nearly all state governments, liquor revenues are a cash cow. Five southern states – Andhra Pradesh, Telangana, Tamil Nadu, Karnataka, and Kerala – account for more than 45% of all liquor sold in India. Not surprisingly, more than 10% of their revenues come from taxes on liquor sales. The other six top-consuming states – Punjab, Rajasthan, Uttar Pradesh, Madhya Pradesh, West Bengal, and Maharashtra – mop up between less than five to 10% of their revenues from liquor.

Regulatory oversight of both central and state governments encompasses a slew of restrictions on the production, movement, and sale of alcoholic beverage products.

Alcohol beverage also falls under the purview of the Food Safety and Standards Authority of India (FSSAI). The Food Safety and Standards Authority of India (FSSAI) is an autonomous body under the Ministry of Health and Family Welfare, Government of India (GoI). It has drafted a set of regulations known as the Food Safety and Standards (Alcoholic Beverages Standards) Regulations, 2018, aimed at specifying the standards for all types of alcoholic beverages – distilled spirits, wines, and beer. It also lays down the specific requirements for labeling alcoholic beverages, in addition to the labeling requirements of Food Safety and Standards (Packaging and Labelling) Regulations, 2011. The specific labeling requirements include the declaration of alcohol content, labeling of standard drink, barring the display of any nutritional information, barring health claim, restriction on words ‘non-intoxicating or words implying similar meaning on labels of beverages containing more than 0.5 percent alcohol by volume, labeling of wine, allergen warning, statutory warning, and many more. These standards and labeling requirements are applicable for both domestically produced and imported products and their enforcement began from 1st of April, 2019.

Besides, direct advertising of alcoholic beverage products is not permitted in India. This means that brands launched and heavily promoted before then generally enjoy much better recall than more recent launches. However, surrogate advertising continues in India, with sports tournaments, events and surrogate brands in mineral water being offered under alcoholic drinks brand names.

This creates an entry barrier in the industry as it will be extremely tough for a new player to enter and build a brand. Besides, the alcohol industry requires a license or certification from the government to do business (Licenses are required to produce, bottle, store, distribute, or retail all alcoholic beverage products.) Licenses shape a potential entrant’s payoff for reasons that make common sense. Acquiring licenses or certifications is costly, hence creating a barrier for an entrant.

Entry barriers protect an industry from newcomers who would add new capacity and seek to gain market share. The threat of entry dampens profitability in two ways. It caps prices because higher industry prices would only make entry more attractive for newcomers. At the same time, incumbents typically have to spend more to satisfy their customers. This discourages new entrants by raising the hurdle they would have to clear to compete. High regulation acts as a state-granted advantage to the alcohol industry. The government is, directly or indirectly, protecting a company from the competition.

To conclude…

The industry is bottled with attractive opportunity size, packaged with ambiguous regulations, and labeled with “regulations can derail your quantitative models”.

Industry attractiveness can be a powerful lever for potential value creation. In which industry you play matters. Industry’s impact is so substantial that you would be better off as an average company in a great industry than a great company in an average industry. But, the industry is not destiny. As Michael Mauboussin emphasizes, that even the best industries include companies that destroy value and the worst industries have companies that create value. That some companies buck the economics of their industry provides insight into the potential sources of economic performance.

Thank you for reading, see you soon!

Neel Chhabra

Hello I am Soic tribe member. Thank you for writing such insightful tweets and Substacks. wanted to interact with you. How can one connect with you? ThankYou.