Competitive Strategy and Investing Framework: Industry Economics and Competitive Position

Part II: A Jump Down Deep - Industry Analysis and Applied Wisdom to Investing.

Welcome to Neel’s Newsletter by me, Neel Chhabra. If you aren’t subscribed and are curious about the Craft of Investing and Living Life in a Multidisciplinary way, join this insatiably curious community by subscribing here:

If you think your friends would like to read the newsletter, please share it with them.

Hi friends,

Greetings from Delhi!

Happy New Year!

This is the second part of the three-part series on Competitive Strategy and Investing Framework.

“If I have seen a little further it is by standing on the Shoulders of Giants,” wrote Isaac Newton. Let’s climb on the shoulders of Giants and hope to see a little further.

In Part I: Competitive Strategy and Investing Framework: Value Creation versus Value Capture, we had a helicopter view, in this part, we’ll jump down deep discussing industry economics.

Let’s jump off then!

Competitive Strategy and Investing Framework: Industry Economics and Competitive Position

In Part I: Competitive Strategy and Investing Framework: Value Creation versus Value Capture, we began by, that investors need to understand innovation because the value is created through innovation, it’s the shaping mechanism of which companies will win and lose. To capture the value created, an understanding of competitive strategy is essential.

In his excellent book, The Origin of Wealth, Eric Beinhocker offers a scientifically rigorous definition of the creation of economic value, based upon the work of the Economist Georgescu-Roegen:

A pattern of matter, energy, and/or information has economic value if the following three conditions are jointly met:

1) Irreversibility: All value-creating economic transformations and transactions are thermodynamically irreversible.

2) Entropy: All value-creating economic transformations and transactions reduce entropy locally within the economic system, while increasing entropy globally.

3) Fitness: All value-creating economic transformations and transactions produce artifacts and/or actions that are fit for human purposes.

Value is created through an irreversible process that gives a resource’s ‘order’ greater usefulness to other humans.

Economist Paul Romer says that we have progressively learned how to rearrange raw materials to make them more and more valuable. Whereas control over physical resources was the primary source of wealth one hundred years ago, today the ideas and formulas to manipulate raw materials form the engine of wealth creation. Romer distinguishes between two parts of the value-creation process: the discovery of new instructions, ideas, or formulas and the carrying out of those instructions. New instructions are of no value unless someone can effectively execute them.

Jack Hughes in What Value Creation Will Look Like in the Future says:

The value of products and services today is based more and more on creativity — the innovative ways that they take advantage of new materials, technologies, and processes. Value creation in the past was a function of economies of industrial-scale: mass production and the high efficiency of repeatable tasks. Value creation in the future will be based on economies of creativity: mass customization and the high value of bringing a new product or service improvement to market; the ability to find a solution to a vexing customer problem; or, the way a new product or service is sold and delivered.

Because of the flexibility of digital language, we can now identify and manipulate building blocks like never before. Combine this with the growing inventory of building blocks, and the conclusion is that the rate of innovation is likely to accelerate. Wealth in the future is likely to follow those who create useful ideas instead of those who execute those ideas.

In 1996, W. Brian Arthur wrote a seminal article Increasing Returns and the New World of Business in which he introduced the concept of increasing returns. Increasing returns are the tendency for that which is ahead to get further ahead, which loses advantage to lose further advantage. They are mechanisms of positive feedback that operate—within markets, businesses, and industries—to reinforce that which gains success or aggravates that which suffers the loss. Increasing returns generate not equilibrium but instability: If a product or a company or a technology—one of many competing in a market—gets ahead by chance or clever strategy, increasing returns can magnify this advantage, and the product or company or technology can go on to lock in the market. More than causing products to become standards, increasing returns cause businesses to work differently, and they stand many of our notions of how the business operates on their head.

In the market of diminishing returns, the more you get ahead, by increasing your market share or your market, the sooner you run into difficulties, with increased costs or lower profits. Products or companies that get ahead in a market eventually run into limitations, so that a predictable equilibrium of prices and market shares is reached. The increasing returns system is growing in relative power. Mechanisms of increasing returns exist alongside those of diminishing returns in all industries. But roughly speaking, diminishing returns hold sway in the traditional part of the economy—the processing industries. Increasing returns reign in the newer part—the knowledge-based industries. Modern economies have therefore bifurcated into two interrelated worlds of business corresponding to the two types of returns. The two worlds have different economics.

The world is divided, we can usefully think of two economic regimes or worlds: a bulk-production world yielding products that essentially are congealed resources with a little knowledge and operating according to Alfred Marshall’s principles of diminishing returns, and a knowledge-based part of the economy yielding products that essentially are congealed knowledge with little resources and operating under increasing returns. The two worlds are not neatly split. Most companies have both knowledge-based operations and bulk-processing operations. But because the rules of the game differ for each, companies often separate them.

The neoclassical equilibrium-based version of macroeconomics appears distant from reality and so does the established microeconomic legacy, which seems unable to explain corporate success and failure today. In particular, the central idea of declining returns to scale seems lacking in explanatory power. The importance of assets and hence Tobin’s Q appears undermined with many physical assets worthless and with dominant companies which have few assets themselves.

Under “Old Economics,” Arthur list investors as identical, rational, and equal in ability. The system is devoid of any real dynamics. Everything is in equilibrium. Economics is based on classical physics under the belief that the system was structurally simple. Under “New Economics,” Arthur says that people are separate and different in ability. They are emotional. The system is complicated and ever-changing. In Arthur’s mind, economics is not simple but inherently complex, more akin to biology than physics.

Dragonflies have two eyes, like humans, but they are very different from ours. They are enormous with the surface covered with a tiny lens, aggregating in some species up to thirty thousand. Each adjacent lens covers a different physical space and thus gives a unique perspective. The vision thus is a synthesis of these unique perspectives. Aggregating perspectives is the key to understanding ideas in a complex adaptive system in which rules are continually changing themselves to better adapt to the impact of changes in the historical environment.

An essential element of complex adaptive systems is the feedback loop. That is, agents in the system first form expectations or models and then act based on predictions generated by these models. But over time these models change depending on how accurately they predict the environment. If the model is useful, it is retained; if not, the agents alter the model to increase its predictability. The accuracy of predictability is a paramount concern to participants in the stock market, and we may be able to achieve a broader understanding if we can learn to view the market as one type of complex adaptive system. In the markets, each agent’s predictive models compete for survival against the models of all other agents, and the feedback that is generated causes some models to be changed and others to disappear. It is a world, says Arthur, that is complex, adaptive, and evolutionary.

"Visionaries are not people who see things that are not there, but who see things that others do not. As Einstein quipped, ‘Why do some people see the unseen?’" - Bennett Goodspeed

In any dynamic and non-linear domain, you can not succeed if you have what psychologists call functional fixedness, the idea that when we use or think about something in a particular way we have great difficulty in thinking about it in new ways. “It's extraordinary how resistant some people are to learning anything,” said Charlie Munger. What's astounding, Warren Buffett added, “is how resistant they are even when it's in their self-interest to learn.” Then in a more reflective tone, Warren continued, “There is just an incredible resistance to thinking or changing.” To quote Bertrand Russell: “Most men would rather die than think. Many have.” And in a financial sense, that's very true.

Max Stirner, a German philosopher wrote the book Der Einzige und sein Eigenthum (1844). This book is usually known as The Ego and Its Own in English, but a more literal translation would be The Unique Individual and their Property. Stirner contended that people do not have ideas. Rather, their ideas have them. These “fixed ideas” then rule over their thinking. Stirner wrote that thought was your own only when you “have no misgiving about bringing it in danger of death at every moment.” He looked forward to having his ideas tested and knocked down: “I shall look forward smilingly to the outcome of the battle, smilingly lay the shield on the corpses of my thoughts and my faith, smilingly triumph when I am beaten. That is the very humor of the thing.”

Negative space (or the shape that lies beyond that is visible), in art, is the space around and between the subject(s) of an image. Negative space may be most evident when the space around a subject, not the subject itself, forms an interesting or artistically relevant shape, and such space occasionally is used to artistic effect as the “real” subject of an image. In the graphic design of printed or displayed materials, where effective communication is the objective, the use of negative space may be crucial. What lies beyond the numbers is more interesting than the numbers themselves. Investing in businesses is part art, part science. Businesses cannot be understood without numbers, nor can they be understood with numbers alone. Numbers cannot model trust, integrity, reputation, management execution. Nuanced judgment of the non-numerical unquantifiable is required.

And in this process, when one is dealing in shadows, one can go wrong. British Philosopher and Logician Carveth Read remind us that we’d rather be vaguely right than exactly wrong. Remember the words of John Maynard Keynes: “It is better to be roughly right than precisely wrong.”

While margins, return on invested capital are visible in numbers, what is not easily visible in numbers—the moat is what gives the business defensibility. ROIC and Margins are “effects” of having a competitive advantage or economic moat, not the “causes”—They are reflections of moats, they are not the moat themselves.

Innovation and change are the lifeblood of progress. The stories that people tell themselves and the preferences they have for goods services don’t tend to sit still. They change with culture and generation. They’re always changing and always will. Social trends, demographics, disruptive technologies, product innovation, etc, are important factors, that can bring about large shifts in value migration. They require the use of mental models that fall outside the normal use of “spreadsheet” growth rates. The growth here cannot be easily predicted. The evolution of technology, consumer preferences, and the ever-changing competitive landscape renders most of today’s winners ineffective in confronting tomorrow’s challenges.

“The essential point to grasp is that in dealing with capitalism we are dealing with an evolutionary process…

“…The fundamental impulse that sets and keeps the capitalist process engine in motion comes from the new consumer goods, the new methods of production and transportation, the new markets, the new forms of industrial organization that capitalist enterprise creates.

“…This process of Creative Destruction is the essential fact about capitalism. It is what capitalism consists in and what every capitalist concern has got to live with….”

— Joseph Schumpeter

The central point of Joseph Schumpeter's whole life work is that capitalism can only be understood as an evolutionary process of continuous innovation and 'creative destruction.’ Schumpeter came to believe economic growth occurred over a series of long cycles, what he called waves, with each picking up speed through time. According to Schumpeter, the "gale of creative destruction" describes the "process of industrial mutation that continuously revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one"

Adrian Slywotzky defines value migration as a flow of economic and shareholder value away from obsolete business models to new, more effective designs that are better able to satisfy customers’ most important priorities. It reflects changing customer needs that will be satisfied with new competitive offerings. Value migration occurs when there is a disconnect between customer priorities and existing business designs.

Essentially, value migration has three stages:

Value inflow: In this phase, a company or an industry captures value from other industries or companies due to a superior value proposition. The market share and profit margins of the company or industry expand. Naturally, this is the most desirable phase for any company. Early-stage innovators, pioneers of new technology, companies offering unique value propositions are the habitants of the value inflow stage.

Stability: In this phase, the competitive equilibrium is established. Growth rates moderate. Market shares also settle down and a certain comfort zone is established for incumbents. This typically paves way for the next phase. The bulk of the business models reside in this phase – well-developed segments with limited penetration and per capita consumption opportunities, oligopolies, and industries with regulatory barriers.

Value outflow: Value starts to move away towards companies or industries meeting evolving customer needs. In this phase, market share declines, margins contract, and growth stops. The heavy competitive intensity with price wars and battles for customer retention characterize this phase. Mature business models with saturation, industries with stagnant innovation typically are in the value outflow stage.

Michael Mauboussin asks us to think of sustainable value creation in two dimensions—how much economic profit a company earns and how long it can earn excess returns. Business quality is about defensibility—defensibility comes from moats. The test of whether a moat exists is quantitative, although the factors that creating moats are qualitative.

Species tend to adapt to their surroundings to survive, given the combination of their genetics and their environment – an always-unavoidable combination. However, adaptations made in an individual’s lifetime are not passed down genetically, as was once thought: Populations of species adapt through the process of evolution by natural selection, as the most-fit examples of the species replicate at an above-average rate. The evolution-by-natural-selection model leads to something of an arms race among species competing for limited resources. When one species evolves an advantageous adaptation, a competing species must respond in kind or fail as a species. Standing still can mean falling behind. This arms race is called the Red Queen Effect for the character in Alice in Wonderland who said, “Now, here, you see, it takes all the running you can do, to keep in the same place.”

So how does a business survive in constantly changing environments? When change hits, a common response is denial or trying to adapt with a business model that no longer works. We can influence the outcome in changing environments more rapidly by first recognizing that we actually need to survive and then moving to survive with new ideas.

- Roberta Bondar

Competitive Advantage is rare and short-lived in the Darwinian world. Indeed, it is precisely what one would expect in an evolutionary system. In biological systems, species are locked in a never-ending co-evolutionary arms race with each other. A predator species might evolve faster-running speed, its prey might evolve better camouflage, while the predator might then evolve a better sense of smell, and so on, indefinitely, with no rest for evolutionary weary.

The Red Queen Effect applied to business, is an argument against complacency. Complacency will kill you. The stronger we are relative to others, the less willing we generally are to change. We see strength as an immediate advantage that we don’t want to compromise. However, it’s not strength that survives, but adaptability. Strength becomes rigidity. Eventually, your competitors will match your strength or find innovative ways to neutralize it. Real success comes from being flexible enough to change, letting go of what worked in the past, and focusing on what you need to thrive in the future. Your competitors are always working to get ahead, and thus you must as well. Your customers’ needs are always changing, and you need to be able to identify and meet these. Considering the actions of your competitors and the desires of your customers are part of the core, daily functions that your business must always perform. Overall, when applied in business, this principle can promote an environment where there is an infinite capacity for innovation.

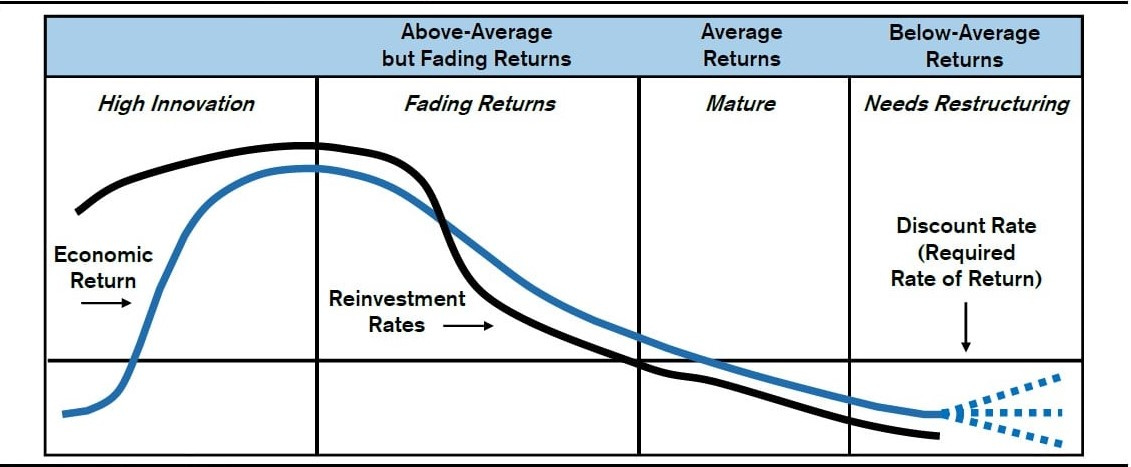

Companies must create and capture the most value possible during the Competitive Advantage Period (CAP) also known as Fade Rate, which is the time during which a company generates returns on investment that exceed its cost of capital. The growth Advantage Period (GAP) is the time during which the pace of cash flow growth in a company is highest. I prefer to consider both in conjunction.

Regression toward the mean says that an outcome that is far from average will be followed by an outcome that has an expected value closer to the average. There are aspects of running the business within management’s control, including selecting the product markets it chooses to compete in, pricing, investment spending, and overall execution. Call that skill. There are also aspects of the business that are beyond management’s control, such as macroeconomic developments, customer reactions, and technological change. Call that luck. Whenever luck contributes to outcomes, there is regression toward the mean. The second explanation for regression toward the mean is that competition drives a company’s return on investment toward the opportunity cost of capital. This is based on microeconomic theory and is intuitive. The idea is that companies that generate a high economic return will attract competitors willing to take a lesser, albeit still attractive, return. Ultimately, this process drives industry returns toward the opportunity cost of capital.

The occurrence happens when several observations follow the law of large numbers. If a random variable is extreme on its first measurement, regression to the mean suggests that it will be closer to the mean or average on its subsequent measurements.

It’s easy to understand the concept. But not understanding its limitations or where it’s applicable can prove very dangerous. For example, large amounts of money have been subject to opportunity cost in the stock market by erroneously buying below-average price-to-book companies believing their values will follow the regression to the mean principle. That is until the investor realizes that the price is just the numerator and the book value – the denominator – starts to turn on the thesis.

Since stock markets typically value companies on the not unreasonable assumption that their returns will regress to the mean, businesses whose returns do not do this can become undervalued. Therein lies our opportunity as investors.

The businesses we seek to invest in do something very unusual: they break the rule of mean reversion that states returns must revert to the average as new capital is attracted to business activities earning super-normal returns.

- Terry Smith

Companies must find a way to defy these powerful competitive forces to achieve sustainable value creation. In effect, CAP is a measure of the longevity of a company’s Moat. Value capture is important to ongoing survival because it allows for reinvestment in the business to create a stronger competitive advantage.

Warren Buffett buys businesses with “high returns on capital” (returns over the cost of capital) that have “deep and wide moats” (sustainable CAPs) and holds them “forever” (hoping that the CAPs stay constant).

Represented graphically, the competitive advantage period (CAP) is the duration of excess returns. In other words, how long a company can earn returns over the opportunity cost of capital is the competitive advantage period.

Drosophila, a common fruit fly goes from embryo to death in about two weeks. This rapid rate of reproduction allows scientists to study hundreds of generations of the fly’s development and mutations in a relatively short time. Drosophila’s fast evolution provides scientists with important clues about evolution in other species, which generally evolve at a relatively glacial pace.

The average speed of evolution is accelerating in the business world. Just as scientists have learned a great deal about the evolutionary change from fruit flies, investors can benefit from understanding the sources and implications of accelerated business evolution. The most direct consequence of more rapid business evolution is that the time an average company can sustain competitive advantage—that is, generate an economic return over its cost of capital—is shorter than it was in the past. The quality of the entry barriers and the life-cycle of the entry barriers are subject to enormous change, sometimes over short periods emanating from circumstances and industries over which the investor may not have sufficient awareness or knowledge. The speed of change and disruption possibilities have never been greater in many industries. Assessing how strong entry barriers are has become the biggest challenge for investors. This trend has potentially important implications for investors in areas such as valuation, portfolio turnover, and diversification.

The future is not only risky and uncertain but contains the potential to reveal ignorance. By adopting a margin of safety approach one can be wrong, make a mistake, and still have an acceptable result. Awareness of ignorance is a great strength. Ignorance more often begets confidence than knowledge, says Charles Darwin. Only when you know something about a subject can you be aware of what you don’t know. Warren Buffett has often stated that investors must know when they are operating well within their circle of competence and when they are approaching the perimeter. What needs to be thought about should be important and knowable, by which I mean to some extent predictable within a reasonable narrow band of high probabilities. What needs to be avoided is the “circle of illusory competence” which deals with a whole bunch of things that are not knowable by which I mean predictable within a narrow band of high probabilities. It is easy to migrate from the good circle to the other one because of all the cognitive biases that we are prone to and the tendency to confuse luck and skill.

If super-talented people will be your competitors in an investment arena, perhaps it is best not to invest. Warren Buffett believes: “The secret of life is weak competition.” In other words, life is best approached with opportunity cost in mind. Why would you decide to invest in an area where you don’t have a significant advantage, particularly when there are areas where you may have a significant advantage? Charlie Munger puts it this way: “You have to figure out what your aptitudes are. If you play games where other people have the aptitudes and you don’t, you’re going to lose. And that’s as close to certain as any prediction that you can make. You have to figure out where you’ve got an edge. And you’ve got to play within your circle of competence.” “The amazing thing is we did so well while being so stupid. That’s why you’re all here: you think that there’s hope for you. Go where there’s dumb competition.”

“The game of investing is one of making better predictions about the future than other people. How are you going to do that? One way is to limit your tries to areas of competence. If you try to predict the future of everything, you attempt too much.” - Charlie Munger

A company’s CAP is determined by a multitude of factors, both internal and external. On a company-specific basis, considerations such as industry structure, the company’s competitive position within that industry, and management strategies define the length of CAP. The structured competitive analysis framework set out by Michael Porter can be particularly useful in this assessment. The key determinants of CAP can be largely captured by a handful of drivers. The first is the company’s current return on invested capital. Generally speaking, higher ROIC businesses within an industry are the best positioned competitively (reflecting scale economies, entry barriers, and management execution). As a result, it is often costlier and/or more time-consuming for competitors to wrest competitive advantage away from high-return companies. The second is the rate of industry change. High returns in a rapidly changing sector (e.g., technology) are unlikely to be valued as generously as high returns in a more prosaic industry (e.g., beverages). The final driver is barriers to entry. High barriers to entry—or in some businesses, “lock-in” and increasing returns—are central to appreciating the sustainability of high returns on invested capital.

“Marathon’s experience suggests that the stock market is often poor at pricing superior fade characteristics. Mis-pricing stems from a number of sources. One is the under-estimation of the durability of barriers to entry. Another is the under-appreciation of the scale and scope of the addressable market. Management’s capital allocation skills are also often overlooked.” - Marathon Asset Management

Industry Structure—Five Forces Analysis

Michael Porter, a giant in the field of competition and strategy, is well known for his Industry Structure—Five Forces Analysis. The five forces framework explains the industry’s average prices and costs, and therefore the average industry profitability you are trying to beat. Porter recommends using industry analysis to understand “the underpinnings of competition and the root causes of profitability.” Porter argues that the collective strength of the five forces determines an industry’s potential for value creation. The five forces framework applies in all industries for the simple reason that it encompasses relationships fundamental to all commerce. But the industry does not seal the fate of its members. An individual company can achieve superior profitability compared to the industry average by defending against the competitive forces and shaping them to its advantage.

The Fundamental Equation: Profit = Price – CostAt its heart, business competition is about the struggle for profits, the tug-of-war over who gets to capture the value an industry creates. As complex and multidimensional as competition typically is, the math of profitability is simple. Porter reminds us to stay focused on the ultimate goal—profit—and its two components, price and cost:

Unit Profit Margin = Price – CostCosts include all the resources used in competing, including the cost of capital. These are the resources that the industry transforms to create value. Prices reflect how customers value the industry’s offerings, what they are willing to pay as they weigh their alternatives. Note that if an industry doesn’t create much value for its customers, prices will barely cover costs. If the industry creates a lot of value, then structure becomes critical in understanding who gets to capture it. Industries can, and often do, create a lot of value for their customers or suppliers while the companies themselves earn very little for their efforts. Within a given industry, the relative strength of the five forces and their specific configuration determine the industry’s profit potential because they directly impact the industry’s prices and costs.

Supplier power

It is the degree of leverage a supplier has with its customers in areas such as price, quality, and service. An industry that cannot pass on price increases from its powerful suppliers is destined to be unattractive. Suppliers are well-positioned if they are more concentrated than the industry they sell to, if substitute products do not burden them, or if their products have significant switching costs. They are also in a good position if the industry they serve represents a relatively small percentage of their sales volume or if the product is critical to the buyer. Sellers of commodity goods to a concentrated number of buyers are in a much more difficult position than sellers of differentiated products to a diverse buyer base. Powerful suppliers will charge higher prices or insist on more favorable terms, lowering industry profitability.

Buyer power

It is the bargaining strength of the buyers of a product or service. It is a function of buyer concentration, switching costs, levels of information, substitute products, and the offering’s importance to the buyer. Informed, large buyers have much more leverage over their suppliers than do uninformed, diffused buyers. Powerful buyers will force prices down or demand more value in the product, thus capturing more of the value for themselves.

Substitution threat

It addresses the existence of substitute products or services, as well as the likelihood that a potential buyer will switch to a substitute product. A business faces a substitution threat if its prices are not competitive and if comparable products are available from competitors. Substitute products limit the prices that companies can charge, placing a ceiling on potential returns.

The threat of new entrants, or barriers to entry

It is arguably the most important of Porter’s five forces. Entry barriers protect an industry from newcomers who would add new capacity and seek to gain market share. The threat of entry dampens profitability in two ways. It caps prices because higher industry prices would only make entry more attractive for newcomers. At the same time, incumbents typically have to spend more to satisfy their customers. This discourages new entrants by raising the hurdle they would have to clear to compete.

It is important to understand the history of entry and exit for the specific industry you are analyzing. These rates vary widely based on where the industry is in its life cycle and on the industry’s barriers to entry and exit. Research shows that the number of firms in new industries follows a consistent path. The market is uncertain about the products it favors in the early stage of industry development, which encourages small and flexible firms to enter the industry and innovate. As the industry matures, the market selects the products it wants and demand stabilizes. The older firms benefit from economies of scale and entrenched advantages, causing a high rate of exit and a move toward a stable oligopoly.

What influences the decision of a challenger to enter in the first place? On a broad level, potential entrants weigh the expected reactions of the incumbents, the anticipated payoffs, and the magnitude of exit costs. neglect the high base rates of business failure, leading to overconfidence and a rate of entry that appears higher than what is objectively warranted.

Four specific factors predict the likely ferocity of incumbent reaction: asset specificity, the level of the minimum efficient production scale, excess capacity, and incumbent reputation.

Asset specificity: It’s not the quantity of assets that matters but how specific those assets are to the market. A firm that has assets that are valuable only in a specific market will fight vigorously to maintain its position. Asset specificity takes several forms, including site-specificity, where a company locates assets next to a customer for efficiency; physical specificity, where a company tailors assets to a specific transaction; dedicated assets, where a company acquires assets to satisfy the needs of a particular buyer; and human specificity, where a company develops the skills, knowledge, or know-how of its employees.

Production scale: For many industries, unit costs decline as output rises. But this only occurs up to a point. This is especially relevant for industries with high fixed costs. A firm enjoys economies of scale when its unit costs decline with volume gains. At some point, however, unit costs stop declining with incremental output and companies get to constant returns to scale. The minimum efficient scale of production is the smallest amount of volume a company must produce to minimize its unit costs. The minimum efficient scale of production tells a potential entrant how much market share it must gain to price its goods competitively and make a profit. It also indicates the size of an entrant’s upfront capital commitment. When the minimum efficient scale of production is high relative to the size of the total market, a potential entrant is looking at the daunting prospect of pricing its product below average cost for some time to get to scale. The steeper the decline in the cost curve, the less likely the entry. The main way an entrant can try to offset its production cost disadvantage is to differentiate its product, allowing it to charge a price premium versus the rest of the industry.

Excess capacity: Assuming that demand remains stable, an entrant that comes into an industry that has too much capacity increases the excess capacity of the incumbents. If the industry has economies of scale in production, the cost of idle capacity rises for the existing companies. As a result, the incumbents are motivated to maintain their market share. So the prospect of a new entrant will trigger a price drop. This prospect deters entry.

Incumbent reputation: Firms usually compete in various markets over time. As a consequence, they gain reputations as being ready to fight at the least provocation or as being accommodating. A firm’s reputation, backed by actions as well as words, can color an entrant’s decision.

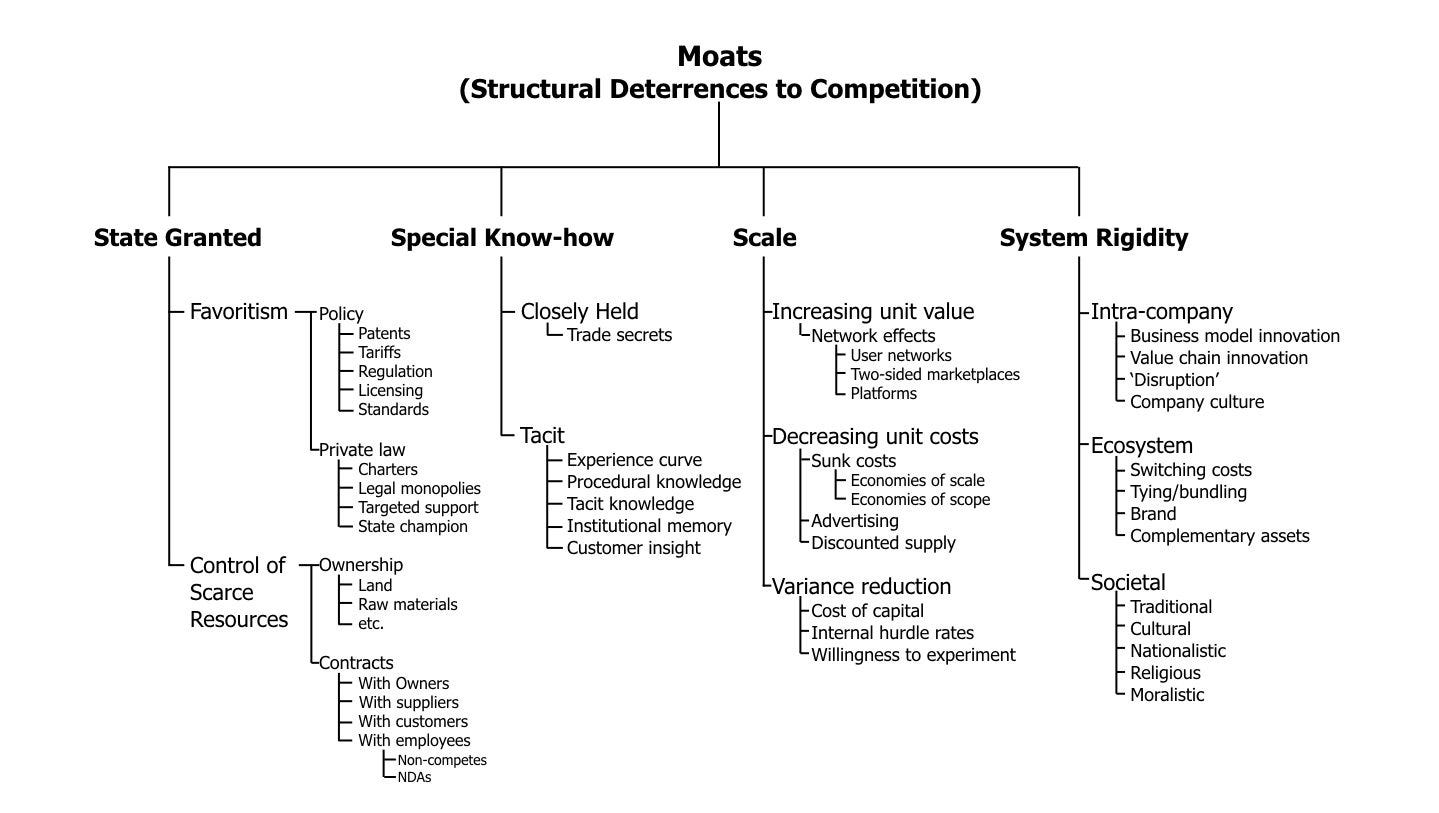

Another important shaper of barriers to entry is the magnitude of the entrant’s anticipated payoff. An entrant cannot be sure that it will earn an attractive economic profit if the incumbent has an insurmountable advantage. Incumbent advantages come in the form of pre-commitment contracts, licenses and patents, learning curve benefits, and network effects. Jerry Neumann in his excellent blog post A Taxonomy of Moats gives us a taxonomy of the most common moats.

State Granted Advantages

The conceptually simplest barriers to entry are those that are state granted. In these, the government is, directly or indirectly, protecting a company from the competition. Governments choose to restrict competition for a range of reasons, from encouraging a certain type of behavior (patents, for instance) to economic protectionism (tariffs, national champions) to politics itself (a quid pro quo, the fear of displeasing a powerful constituency, or even just simple political favoritism.)

Licenses and patents also shape a potential entrant’s payoff for reasons that make common sense. Several industries require a license or certification from the government to do business. Acquiring licenses or certifications is costly, hence creating a barrier for an entrant. Patents are also an important entry barrier. But the spirit of a patent is different from that of a license. A patent intends to allow an innovator to earn an appropriate return on investment. Most innovations require substantial upfront costs. So a free market system needs the means to compensate innovators to encourage their activities. Patents do not discourage innovation, but they do deter entry for a limited time into activities that are protected.

Ideally, the state’s enforcement of a moat is a non-market system. This means the durability of the moat is whatever the government says it is. In some cases, this leads to a lack of predictability, and in others quite a bit of predictability.

Because these moats are transferable, once the moat is created it can’t create excess value: it could be sold now for the amount of value it would create in the future (if that were known). It is the creation of the moat that creates the value, not the ownership of it.

Special Know-How

Having the knowledge that no one else has is an excellent way to prevent imitation and earn specialist profits—Lower costs because of better knowledge, higher price because of better knowledge, and stronger reputation. It restricts access to a scarce but needed resource. A more enduring advantage is tacitly held knowledge. Tacit knowledge is the knowledge that can’t be easily communicated; it can’t be easily transferred, e.g. verbally or through writing.

Individual tacit knowledge, while always valuable, is a weak competitive advantage as an organization gets larger because it is hard to scale. It is also only sustainable until a competitor hires the individual who has it. Some tacit knowledge is not contained within the head or hands of individuals but embodied in an organization. All companies have undictated and undocumented means and paths to get things done. Two people may have tacit knowledge about how to work most effectively with each other’s role, or three people, or whole organizations. The organizational routines of these companies are difficult to replicate advantage because they are not describable in words, in any deep sense, and they are not held within the head of a single person. While individual tacit knowledge goes down the elevator every day, collective tacit knowledge is more durable and harder for competitors to obtain or imitate.

Returns to Scale

Returns to scale are advantages that appear or increase as a company gets bigger. They are a powerful barrier to entry because, by definition, they are not available to any entrant that starts small (as most would have to). They take several forms but generally either the cost per unit product decreases or the quality of the product increases as more units are produced, sold, and used.

Learning curves can also serve as a barrier to entry. The learning curve refers to an ability to reduce unit costs as a function of cumulative experience. A company can enjoy the benefits of the learning curve without capturing economies of scale and vice versa. But generally, the two go hand in hand.

While many investors get excited about the first-mover advantage, they tend to ignore that it can be a disadvantage. Though learning curve effects benefit a first mover as its variable costs decline with cumulative production volume, the plants or technology built later are more efficient than earlier ones, the first mover has the overhang to get rid of the vintage effects which count against the first mover.

In addition to lowering costs, the scale can also increase the value of a product. This is often called network effects (regardless of whether there is a ‘network’ or not.) Telephone service is worthless if you are the only one with a telephone. It becomes valuable when someone else also has one, and more valuable as more and more people get them. The key is that it becomes more valuable not just to you but to everyone on the network. This dynamic lends itself to monopolization, so long as different companies can’t interconnect. Even when they can, competition is limited by the cost of interconnection. The current crop of large social media companies primarily uses the size of their user networks as a way to maintain their dominance.

Network effects are the important incumbent advantage that can weigh on an entrant’s payoff. Network effects exist when the value of a good or service increases as more members use that good or service. As an example, Uber is attractive to passengers precisely because so many riders and drivers congregate on the platform. In a particular business, positive feedback often ensures that one network becomes dominant. Size, network structure, and connectivity contribute to network strength. Other examples today are the online social networks, including Facebook and Instagram, which become more valuable to a user as more people join. We also see network effects in the smartphone market between the dominant operating systems and application developers. Because the vast majority of users own devices operating on Android or iOS, application developers are far more likely to build applications for them than for other operating systems. This creates a powerful ecosystem that is daunting for aspiring entrants.

Network effects are important because they are the best form of defensibility and value creation in the digital world. Brian Arthur recognized the capital-light nature of technology businesses meant they could become entrenched in a winner-take-most scenario. High upfront costs, network effects, and customer lock-in all serve to increase business sustainability over time.

Two-sided marketplaces and platforms are often lumped into network effects, though they don’t create networks. Marketplaces create more value from scale because scale creates more supply and demand for the products sold through the marketplace. This creates a virtuous cycle—sellers want more buyers rather than fewer, buyers want more sellers rather than fewer—so a small advantage in scale can become self-reinforcing. Similarly, platforms garner value from other companies creating uses for them, and those companies would prefer to create uses for large platforms rather than smaller ones. The users of those platforms, meanwhile, prefer more uses to fewer. This makes it difficult for competing platforms to get a foothold.

System Rigidity

These are advantages that arise because change is hard in a complex or highly interlinked system. If changing from one product to another also requires changing other things—other products, routines, skills, etc.—the total cost of the change may outweigh the benefits so the product already embedded in the system can maintain an advantage over similar entrant products that are not (or not yet) interconnected.

Often, companies secure future business through long-term contracts. These contracts can be efficient in reducing search costs for both the supplier and the customer. A strong incumbent with a contract in place discourages entry. Precommitment also includes quasi-contracts, such as a pledge to always provide a good or service at the lowest cost. Such pledges, if credible, deter entry because new entrants rarely have the scale to compete with incumbents. System rigidity can be a quite durable source of advantage in an environment of incremental change. Products that are the same as existing ones, or even somewhat better, will not give the customer enough additional value for them to switch if the switching costs are high.

The Link between Barriers to Entry and Barriers to Exit.

High exit costs discourage entry. The magnitude of investment an entrant requires and the specificity of the assets determines the size of exit barriers. Low investment needs and non-specific assets are consistent with low barriers to entry.

The learning curve, advertising, and R&D/patents—create high entry costs. Reputation, limited pricing, and excess capacity— influence judgments of post-entry payoffs.

Behavioral factors also play a role in the decision to enter a business. Overconfidence of the entrants attributed by researchers as “reference group neglect”, is the idea that the entrants focused on what they perceived to be their unique skills while ignoring the abilities of their competitors and the high failure rate of new entries as reflected in the reference group. The failure to consider a proper reference class pervades many of the forecasts we make. In the business world, reference class neglect shows up as unwarranted optimism for the length of time it takes to develop a new product, the chance that a merger succeeds, and the likelihood of an investment portfolio outperforming the market.

Competitive Rivalry

Rivalry among firms addresses how fiercely companies compete with one another along dimensions such as price, service, new product introductions, promotion, and advertising. In almost all industries, coordination in these areas improves the collective economic profit of the firms. If rivalry is intense, companies compete away the value they create, passing it on to buyers at lower prices or dissipating it at higher costs of competing.

Coordination is difficult if there are lots of competitors. In this case, each firm perceives itself to be a minor player and is more likely to think individualistically. Naturally, the flip side suggests that the existence of fewer firms leads to more opportunities for coordination.

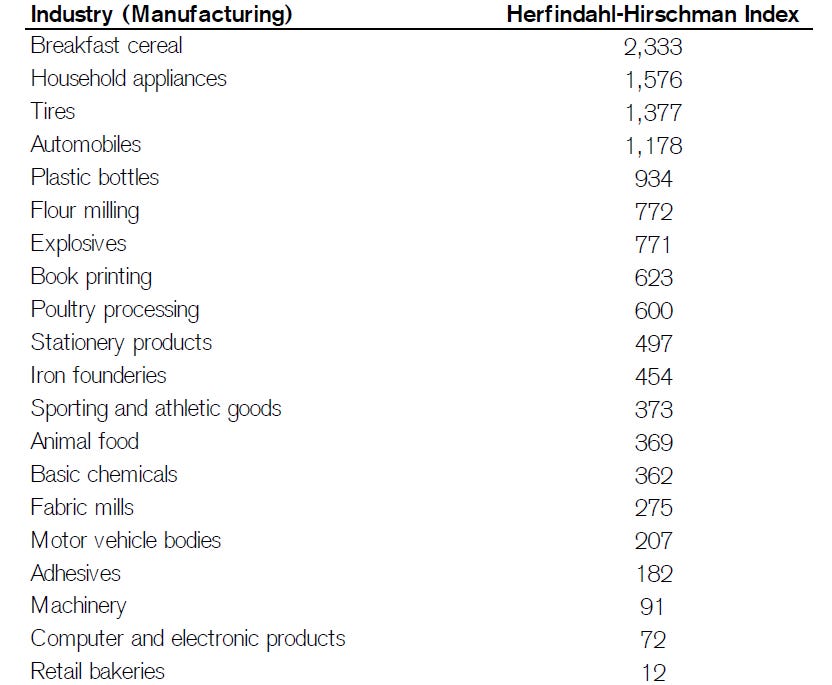

A concentration ratio is a common way to measure the n’ number and relative power in an industry. The Herfindahl-Hirschman Index (HHI) is a popular method to estimate industry concentration. The HHI considers not only the number of firms but also the distribution of the sizes of firms. A dominant firm in an otherwise fragmented industry may be able to impose discipline on others. In industries with several firms of similar size, rivalry tends to be intense. Many economists characterize readings above 1,800 as industries with reduced rivalry. The index is equal to 10,000 times the sum of the squares of the market shares of the 50 largest firms in an industry. If there are fewer than 50 firms, the amount is summed for all firms in the industry.

Generally, concentrated industries earn above-average profits and less concentrated industries earn below-average profits. This is why as we discussed in Part I: Competitive Strategy and Investing Framework: Value Creation versus Value Capture, Warren Buffet loves buying companies in concentrated industries.

Another influence of rivalry is firm homogeneity. Rivalry tends to be less intense in industries with companies that have similar goals, incentive programs, ownership structures, and corporate philosophies. But in many instances, competitors have very different objectives. The strategies that companies within an industry pursue will reflect the heterogeneity of objectives.

Asset specificity plays a role in rivalry. Specific assets encourage a company to stay in an industry even when conditions become trying because there is no alternative use for the assets.

Demand variability shapes coordination costs and hence influences rivalry. When demand variability is high, companies have a difficult time coordinating internally and have little opportunity to effectively coordinate with competitors. Variable demand is a particularly important consideration in industries with high fixed costs. In these industries, companies often add too much capacity at points of peak demand. While companies use this capacity at the peak, the capacity is excessive at the trough and spurs even more intense competition at the bottom of the cycle. The conditions of variable demand and high fixed costs describe many commodity industries, which is why their rivalry is so bitter and consistent positive economic returns are so elusive.

Industry growth is a final consideration. When the pie of potential excess economic profits grows, companies can create shareholder value without undermining their competitors. The game is not zero-sum. In contrast, stagnant industries are zero-sum games and the only way to increase value is to take it from others. So a rise in rivalry often accompanies a decelerating industry growth rate.

Disruption and Disintegration

Most strategy frameworks focus primarily on figuring out which industries are attractive and which companies are well-positioned. Clayton Christensen developed a theory to explain why great companies fail and how companies succeed through innovation. Christensen wondered why it was common for companies with substantial resources and smart management teams to lose to companies with simpler, cheaper, and inferior products. His theory of disruptive innovation explains that process.

Disruptive innovation describes a process by which a product or service powered by a technology enabler initially takes root in simple applications at the low end of a market — typically by being less expensive and more accessible — and then relentlessly moves upmarket, eventually displacing established competitors. Disruptive innovations are not breakthrough innovations or “ambitious upstarts” that dramatically alter how business is done but, rather, consist of products and services that are simple, accessible, and affordable. These products and services often appear modest at their outset but over time have the potential to transform an industry. Robert Merton introduced the concept of "obliteration by incorporation" in his landmark work, Social Theory and Social Structure in 1949, where a concept becomes so popularized that its origins are forgotten. In the process of "obliteration by incorporation", both the original idea and the literal formulations of it are forgotten due to prolonged and widespread use, and enter into the everyday language (or at least the everyday language of a given academic discipline), no longer being attributed to their creator. That has happened to the core idea of the theory of disruption, which is important to understand because it is a tool that people can use to predict behavior. That’s its value—not just to predict what your competitor will do but also to predict what your own company might do. It can help you avoid choosing the wrong strategy.

Disruption does not mean “breakthrough” or “new and shiny,” far too many people assume that a disruption is an event. Rather, disruption is a process. It’s intertwined with the resource allocation process in the firm, the changing needs of customers and potential customers, and the constant evolution of technology.

Christensen starts by distinguishing between sustaining and disruptive innovations.

Sustaining innovations foster product improvement. They can be incremental, discontinuous, or even radical. But the main point is that a sustaining innovation operates within a defined value network—the “context within which a firm identifies and responds to customers’ needs, solves problems, procures input, reacts to competitors, and strives for profit.”

A disruptive innovation, by contrast, approaches the same market with a different value network. Christensen distinguishes between the two types of disruptive innovation: low-end disruption and new-market disruption. A low-end disruptor offers a product that already exists. A new-market disruption, on the other hand, competes initially against “non-consumption.” It appeals to customers who previously did not buy or use a product because of a shortage of funds or skills. A new-market disruptive product is cheap or simple enough to enable a new group to own and use it. Disruptive innovations initially appeal to relatively few customers who value features such as low price, smaller size, or greater convenience. Christensen finds that these innovations generally underperform established products in the near term but are good enough for a segment of the market.

One of the key insights of the model is that innovations often improve at a rate faster than the consumer demands. Established companies, through sustaining technologies, commonly provide customers with more than they need or more than they are ultimately willing to pay for. When innovation drives performance for a sustaining technology past the needs of mainstream customers, the product is “overshot.” Indications that a market is overshot include customers who are unwilling to pay for a product’s new features and who don’t use many of the available features. When the performance of a sustaining innovation exceeds the high end of the consumer’s threshold, the basis of competition shifts from performance to speed-to-market and delivery flexibility. The trajectory of product improvement allows disruptive innovations to emerge because even if they fail to meet the demands of mainstream users today they become competitive tomorrow. Further, disruptive innovations end up squeezing the established producers because the disruptors have lower-cost structures.

A crucial point of Christensen’s work is that passing over disruptive innovations may appear completely rational for established companies. The reason is that disruptive products generally offer lower margins than established ones, operate in insignificant or emerging markets, and are not in demand by the company’s most profitable customers. As a result, companies that listen to their customers and practice conventional financial discipline are apt to disregard disruptive innovations.

Christensen has also done insightful work on understanding and anticipating the circumstances under which the industry is likely to shift from vertical to horizontal integration. This framework is relevant for assessing the virtue of outsourcing. While outsourcing has provided some companies with great benefits, including lower capital costs and faster time to market, it has also created difficulty for companies that tried to outsource under the wrong circumstances.

Firms that are vertically integrated dominate when industries are developing because the costs of coordination are so high. But as an industry develops, various components become modules. The process of modularization allows the industry to flip from vertical to horizontal.

Each industry has strong and weak points compared to other industries. Thus, the industry's relative attractiveness that a company belongs has an important bearing on the company’s fortunes.

It’s always helpful to consider industry-level factors and ask questions such as—Is the industry’s competitive landscape favorable?—Do players enjoy superior bargaining power/terms of trade with customers and/or suppliers?—Does the industry enjoy a large profit pool that can be effectively tapped into by a company with a unique value proposition or strategy?—Is the industry showing trends of value migration? Or does it offer the opportunity for the same in the future?—Is the industry fairly stable i.e. less prone to destabilizing factors like business cyclicality, high production innovation, and regulatory controls?—Is it a new industry strategic opportunity with huge potential?

Understanding the nature, quantum, and longevity of growth drivers of an industry is an integral part of research on a company operating in that industry. These aspects evolve as demographics, customer tastes, and preferences, technology, etc changes over time. Industry analysis provides important background for understanding a company’s current or potential performance.

We’ll jump down deep, discussing Firm-Specific Analysis, Business Strategy in the New World of Business, and a lot more in the next part.

Thank you for reading, see you soon!

Neel Chhabra

Great Article

A very good article