Competitive Strategy and Investing Framework: Business Strategy in the New World of Business

Part III: The Fundamental Framework of Business Strategy—Firm-Specific Analysis and Applied Wisdom to Investing.

Welcome to Neel’s Newsletter by me, Neel Chhabra. If you aren’t subscribed and are curious about the Craft of Investing and Living Life in a Multidisciplinary way, join this insatiably curious community by subscribing here!

If you think your friends would like to read the newsletter, please share it with them!

Hi friends,

Greetings from Delhi!

This is the third and final part of the three-part series on Competitive Strategy and Investing Framework.

“If I have seen a little further it is by standing on the Shoulders of Giants,” wrote Isaac Newton. Let’s climb on the shoulders of Giants and hope to see a little further.

In Part I: Competitive Strategy and Investing Framework: Value Creation versus Value Capture, we had a helicopter view, and subsequently in Part II: Competitive Strategy and Investing Framework: Industry Economics and Competitive Position, we jumped down deep discussing industry economics. In this part, we’ll build up by introducing the fundamental framework for value creation and then considering the various ways a company can add value, discussing firm-specific economics.

Competitive Strategy and Investing Framework: Business Strategy in the New World of Business

At the base of a mountain, we cannot get our bearings or map out our surroundings in a thick forest. We see only what is before our eyes. If we begin to move up the side of the mountain, we can see more of our surroundings and how they relate to other parts of the landscape. The higher we go, the more we realize that what we thought further below was not quite accurate, was based on a slightly distorted perspective. At the top of the mountain, we have a clear panoramic view of the scene and perfect clarity as to the lay of the land. This visual phenomenon tells us that we gain more information over time and see more of the truth; what’s invisible in the present becomes visible and obvious in retrospect; time is the revealer of reality—Businesses are no different.

Tom Gayner offers a thoughtful metaphor: it's the difference between a snapshot, which freezes one specific moment, and a full-length movie, which unfolds over time. Gayner calls quantitative investing “spotting value.” It is like a camera that takes a snapshot. In that snapshot, time is standing still. The evolution of value investing, can be seen as a segue from spotting value with a snapshot to understanding that value unfolds over time like a movie. Charlie Munger concurs: “The days of locating stocks selling at a 25%–50% discount to some liquidating value, a price that someone else would pay to buy the business when it was easy as moving your Geiger counter over low multiple stocks is over. The world has wised up. The game has gotten harder.”

Investing is more art than science because it involves thinking about the facts of the past and the possibilities of the future. There is always an ongoing need for judgment, refinement, patience, and reflection. It is about being roughly right than precisely wrong. There are fundamental flaws in using the backward-looking stuff—At the end of the day, 100 percent of the value of any equity depends on the future, not the past. Qualitative investing is not as easy as taking a snapshot—Financial missteps can be made if an investor's version of how they think their movie will turn out differs from reality.

Gaddis on Continuity and Contingency

“The trouble with the future is that it so much less knowable than the past. Because it lies on the other side of the singularity that is the present, all we can count on is that certain continuities from the past will extend into it, and that they will encounter uncertain contingencies. Some continuities will be sufficiently robust that contingencies will not deflect them: time will continue to pass; gravity will continue to keep us from flying off into space; people will still be born, grow old, and die. When it comes to the actions people themselves choose to take, though when consciousness itself becomes a contingency forecasting becomes a far more problematic exercise.”

— John Lewis Gaddis, The Landscape of History: How Historians Map the Past

One must have an elevated perspective to be able to look far into the future of the business. Since the future is uncertain and unknown, all knowledge about the business degenerates into probability. One must not disregard probability in decision-making under uncertainty. Hindsight bias is a common result of the tendency to neglect probability—it’s the tendency of overestimating one’s ability to have predicted an outcome that could not possibly have been predicted. Hindsight bias is dangerous because it hinders one from learning from past mistakes. If we feel like we knew it all along, it means we won’t stop to examine why something happened.

Probabilities are the rules of the world, and thus probabilistic thinking is one of the most critical traits and skills to espouse. The method of updating a probability estimate for a hypothesis as new evidence or information becomes available. It’s hugely in line with how the world works because Bayesian updating is closely related to subjective probability.

Uncertainty and “The Convention”

“The outstanding fact is the extreme precariousness of the basis of knowledge on which our estimates of prospective yield have to be made . . . If we speak frankly, we have to admit that our basis of knowledge for estimating the yield ten years hence of a railway, a copper mine, a textile factory, the goodwill of a patent medicine, an Atlantic liner, a building in the City of London amounts to little and sometimes to nothing; or even five years hence….

“In practice we have tacitly agreed , as a rule, to fall back on what is, in truth, a convention. The essence of our convention…lies in assuming that the existing state of affairs will continue indefinitely, except in so far as we have specific reasons to expect a change. This does not mean that we really expect the existing state of affairs to continue indefinitely. We know from extensive experience that this is most unlikely. The actual results of an investment over a long period of time seldom agree with the initial expectation….

“Nevertheless the above conventional method of calculation will be compatible with a considerable measure of continuity and stability in our affairs , so long as we can rely on the maintenance of the convention ..”

— John Maynard Keynes, The General Theory of Employment

Knowing what you can know and knowing what you can’t are both vital ingredients of deciding well. Good decision-makers are content with the world being an uncertain and unpredictable place. Instead of focusing on being sure, they try to figure out how unsure they are. Most people think that intelligence is about noticing things that are relevant (detecting patterns); in a complex world, intelligence consists of ignoring things that are irrelevant (avoiding false patterns). Avoiding stupidity is easier than seeking brilliance; we should focus more on not doing stupid things than on doing smart things.

By ‘uncertain’ knowledge…I do not mean merely to distinguish what is known from what is merely probable ….The sense in which I am using the term is that in which the prospect of a European war is uncertain, or the price of copper and the rate of interest twenty years hence, or the obsolescence of a new invention, or the position of private wealth owners in the social system in 1970. About these matters, there is no scientific basis on which to form any calculable probability whatever. We simply do not know.

— John Maynard Keynes, The General Theory of Employment

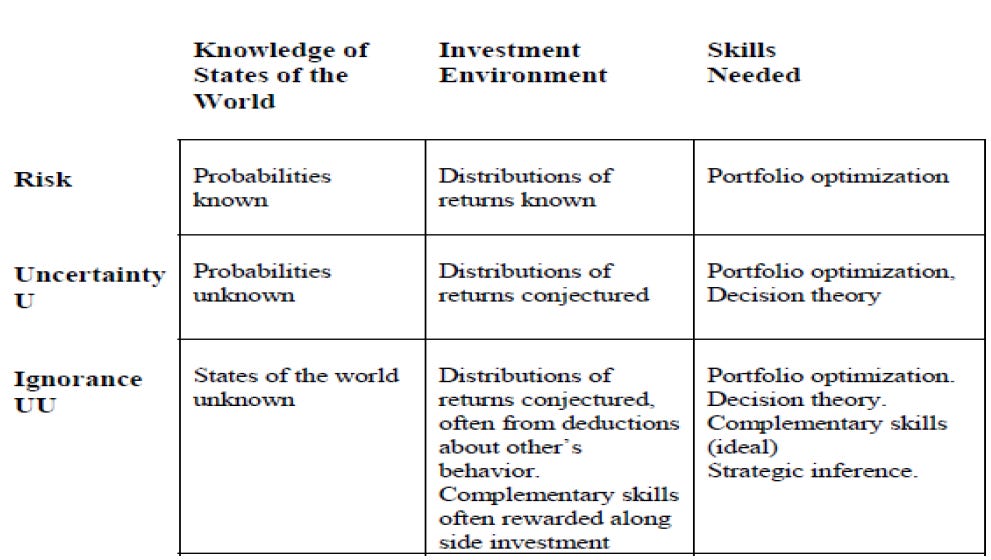

Risk, Uncertainty, and Ignorance

“Risk, which is a situation where probabilities are well defined, is much less important than uncertainty. Casinos, which rely on dice, cards and mechanical devices, and insurance companies, blessed with vast stockpiles of data, have good reason to think about risk. But most of us have to worry about risk only if we are foolish enough to dally at those casinos or to buy lottery cards….” “Uncertainty, not risk, is the difficulty regularly before us. That is, we can identify the states of the world, but not their probabilities.” “We should now understand that many phenomena that were often defined as involving risk – notably those in the financial sphere before 2008 – actually involve uncertainty.” “Ignorance arises in a situation where some potential states of the world cannot be identified. Ignorance is an important phenomenon, I would argue, ranking alongside uncertainty and above risk. Ignorance achieves its importance, not only by being widespread, but also by involving outcomes of great consequence.” “There is no way that one can sensibly assign probabilities to the unknown states of the world. Just as traditional finance theory hits the wall when it encounters uncertainty, modern decision theory hits the wall when addressing the world of ignorance.”

— Richard Zeckhauser

Most aspects and decisions in your life are uncertain rather than risky. What you do is rarely similar to the action on a roulette wheel, which is a risk. In addition, the events that often have the biggest impact on what you do are often part of the domain of ignorance. Wisdom is partly about understanding the implications of the connections as much as it is about the process of making connections. Once you internalize Zeckhauser’s mental model you should naturally start to value a margin of safety more highly. You may not always be able to predict, but you can prepare.

Unknown, Unknowable, and Unique

“Unknown and unknowable [UU] refers “to situations where both the identity of possible future states of the world as well as their probabilities.” “The first positive conclusion is that unknowable situations have been and will be associated with remarkably powerful investment returns. The second positive conclusion is that there are systematic ways to think about unknowable situations. If these ways are followed, they can provide a path to extraordinary expected investment returns. To be sure, some substantial losses are inevitable, and some will be blameworthy after the fact. But the net expected results, even after allowing for risk aversion, will be strongly positive.”…

“Many UU situations deserve a third U, for unique. If they do, arbitrageurs who like to have considerable past experience to guide them will steer clear. So too will anybody who would be severely penalized for a poor decision after the fact. An absence of competition from sophisticated and well monied others spells the opportunity to buy underpriced securities.”…

“People feel that 50% is magical and they don’t like to do things where they don’t have 50% odds. I know that is not a good idea, so I am willing to make some bets where you say it is 20% likely to work but you get a big pay-off if it works, and only has a small cost if it does not. I will take that gamble. Most successful investments in new companies are where the odds are against you but, if you succeed, you will succeed in a big way.” “David Ricardo made a fortune buying bonds from the British government four days in advance of the Battle of Waterloo. He was not a military analyst, and even if he were, he had no basis to compute the odds of Napoleon’s defeat or victory, or hard-to-identify ambiguous outcomes. Thus, he was investing in the unknown and the unknowable. Still, he knew that competition was thin, that the seller was eager, and that his windfall pounds should Napoleon lose would be worth much more than the pounds he’d lose should Napoleon win. Ricardo knew a good bet when he saw it.”…

“Most great investors, from David Ricardo to Warren Buffett, have made most of their fortunes by betting on UUU situations. Ricardo allegedly made 1 million pounds (over $50 million today) roughly half of his fortune at death on his Waterloo bonds. Buffett has made dozens of equivalent investments.”

— Richard Zeckhauser

In part of this quotation immediately above Zeckhauser is describing what Michael Mauboussin calls “The Babe Ruth Effect.” Mauboussin writes:

“…in any probabilistic exercise: the frequency of correctness does not matter; it is the magnitude of correctness that matters…. even though Ruth struck out a lot, he was one of baseball’s greatest hitters…. Internalizing this lesson, on the other hand, is difficult because it runs against human nature in a very fundamental way.”

Venture capital is a classic example of a business that profits from the Babe Ruth effect. Chris Dixon writes in a blog post:

“The Babe Ruth effect is hard to internalize because people are generally predisposed to avoid losses. …What is interesting and perhaps surprising is that the great funds lose money more often than good funds do. The best VCs funds truly do exemplify the Babe Ruth effect: they swing hard, and either hit big or miss big. You can’t have grand slams without a lot of strikeouts.”

Many other situations involve a big upside and a small downside. They are common if you know where to look and how to find them.

Financial returns higher than a market benchmark are most likely to be found in UUU situations. These returns are caused by the fact that investments in UUU environments are much more likely to be mispriced. The domain with the most UUU based opportunity is the world of business. The markets in which a business operates are often not liquid and information hard to obtain. The more you know about a given business the better you will be as both an operator and a financial investor in that business. Howard Marks describes the opportunity in this way: “The investor’s time is better spent trying to gain a knowledge advantage regarding ‘the knowable’—industries, companies, and securities. The more micro your focus, the great the likelihood you can learn things others don’t.” Focusing on the simplest possible system (an individual business in a local market) is often the greatest opportunity for an investor since it is understandable in a way that may reveal a mispriced bet. Market efficiency is lower and potential returns are often higher if you are willing to do the necessary work to retire uncertainty and ignorance.

The interaction between an Industry’s Economics and a specific Company’s Competitive Position is Fundamental to Potential Value Creation.

In Part II: Competitive Strategy and Investing Framework: Industry Economics and Competitive Position, we discussed how industry attractiveness can be a powerful lever for potential value creation. In which industry you play matters. About half of your company’s position on the Power Curve is driven by its industry. Industry’s impact is so substantial that you would be better off as an average company in a great industry than a great company in an average industry. Industry matters a lot in your ability to outperform. When you realize that success is largely defined by your company’s and your industry’s movements on the Power Curve, your perspective changes. Your horizon gets broadened. You’re looking at a new map, a new reference point where you’re no longer comparing the business with last year or their closest rival, but the full universe of companies competing for capital and economic profits.

Success for your strategy becomes moving up on the Power Curve, and your main competitor is the Darwinist force of the market that squeezes your profitability. In the end, it’s you versus the world. Competitive Advantage is rare and short-lived in the Darwinian world. Competition is a driving force of the biological world. All living things are out to survive and breed as much as possible. This puts them in competition for finite resources like food, status, territory, and mates. This may be between whole species or individuals. The fight for resources is a zero-sum game. The more one individual receives, the less there is for others. So competition is inherently harmful to the losers. If a species cannot attain the resources it needs, it will go extinct. The availability of resources dictates the type and intensity of competition. The scarcer the resource, the more aggressive the competition. The upside of competition is that it forces improvements. Companies are constantly fighting for market share. This process is beneficial for consumers because it forces companies to keep prices low and quality high whenever possible. Monopolies—when one company dominates an entire market and customers have no other option—are discouraged because they allow for abuse and create stagnation.

Joseph Schumpeter, an Austrian political economist, identified innovation as the critical dimension of economic change. He argued that economic change revolves around innovation, entrepreneurial activities, and market power. He sought to prove that innovation-originated market power can provide better results than the invisible hand and price competition. He argued that technological innovation often creates temporary monopolies, allowing abnormal profits that would soon be competed away by rivals and imitators. These temporary monopolies were necessary to provide the incentive for firms to develop new products and processes. Competition doesn’t impede innovation—on the contrary, it even increases the innovation efforts of firms that are the closest to the technology frontier. This has particular consequences in the digital economy, where increasing returns contribute to even higher pressure on competing firms. Some among them seize that extra pressure as an opportunity to innovate even more, thus sustaining even higher increasing returns and eventually consolidating their dominant position on the market. Others are simply left behind and have to relinquish their position. In capitalistic competition, the absence of innovation does not result in stasis. It results in decay.

“Economic systems are, of course, complex structures, in which the pattern of interactions resembles a web. This means that the dominant party in one interaction may well be the subordinate in another. Control thus diffuses through the ecosystem, generally from entities with high energy demands to those with more modest requirements. The ability to adapt to, or at least to accommodate, the power structure remains the ticket to success for all players—dominants and subordinates alike— regardless of how much influence an entity wields.”

— Geerat Vermeij

Living systems cannot be fully separated from each other. Every company is part of an industry that is part of a sector that is part of a national economy that is part of a global economy. Nothing exists in isolation. Everything is connected. The ecosystem lens reveals that the actions of any one species have consequences for many others in the same environment. Many systems can take care of themselves, possessing abilities to correct and compensate for changes and external pressures. We need to take the time to learn how the components of our system are interconnected so we can understand how our actions will impact the connections and affect the outcome we are trying to produce. And there are times when the rate of change increases not just in a particular industry, but across the entire global economy. One of the major events that can increase the rate of change across all industries is the development of major new technology. And so in recent decades, we have seen the emergence of the global internet cause just about every industry to change the way they do business. The frequency with which disruptions are transforming industries has been consistently rising over the past 10-20 years. Innovative technologies, digitization, automation, machine learning, artificial intelligence—all these themes have been a significant source of disruption over the last decade. There are several other areas of disruption which could take place over the next decade.

For instance, the rate at which costs of solar and wind power are falling has made many existing fossil fuel plants unviable. Similarly, a rapid fall in automotive battery costs is likely to accelerate the transition from IC engines (Internal Combustion) to EVs (Electric Vehicles) over the next decade. Formalization of various industries, financial inclusion, the transformation of payment mechanisms used by customers, adoption of telecom as a medium to access products and services—and many more such transformations are underway, particularly in India. People and technologies often act as catalysts, increasing the pace of social change and development. Developments in technology often act as catalysts for social changes. Catalysts accelerate reactions that are capable of occurring anyway. They decrease the amount of energy required to cause change, and in the process make possible reactions that might not have occurred otherwise. The COVID pandemic might just be one such catalyst.

Investors can benefit from understanding the sources and implications of Accelerated Business Evolution. The most direct consequence of more rapid business evolution is that the time an average company can sustain competitive advantage—that is, generate an economic return over its cost of capital—is shorter than it was in the past. Financial markets are like living, breathing beings that transform themselves constantly. They move very fast and I suspect that innovation and speed will continue to be the norm. Financial markets are complex adaptive systems. The speed at which they adapt makes investing challenging, but also creates significant opportunities. If investing was easy, everyone would be rich. Michael Mauboussin describes the challenge here:

“Increasingly, professionals are forced to confront decisions related to complex systems, which are by their very nature nonlinear… Complex adaptive systems effectively obscure cause and effect. You can’t make predictions in any but the broadest and vaguest terms… Complexity doesn’t lend itself to tidy mathematics in the way that some traditional, linear financial models do.”

Increasing innovation and speed in markets must be matched by increasing innovation and speed by individuals and businesses in responding to that change. As just one example: “The typical half-life of a publicly-traded company is about a decade, regardless of the business sector. Mortality rates are independent of a company’s age.” If a person or organization has processes that prevent a rapid and accurate response to innovation and change, they are inevitably going to feel pain. Charlie Munger’s advice here has never been more important than it is now: “We all are learning, modifying, or destroying ideas all the time. Rapid destruction of your ideas when the time is right is one of the most valuable qualities you can acquire. You must force yourself to consider arguments on the other side.” Most investors who have been successful, but only for a limited period, hold a correspondence theory of truth. They believe their viewpoint corresponds to some deep, well-founded structure of how markets operate. The correspondence theory of truth relies on absolutes. Stubbornness is a medal of honor. Now contrast this to a pragmatic approach. If you are a pragmatist, you typically have a shorter period in which you will hold an ineffectual model. Pragmatists realize a model, any model, is there only to help you with a certain task. They apply the test of usefulness and utility while discounting the infatuation others have for absolutes.

"The secret to successful investing has been understanding change, how it happens, how much happens and its implications over the long term… The refusal to embrace this is probably a reflection of the doomed desire for security but it is also emblematic of a broader crisis in economic thought that is preoccupied with the mathematics of equilibrium… But if we switch our attention to studying deep change then there is less temptation to believe that investing has eternal verities that we can default to as a rule book… It’s not ‘this time it’s different’ that is the cry of danger but the refusal to admit that the world, and its reflection that is investing, is ever the same… The only rhyme is that in the long run the value of stocks is the long-run free cash flows they generate but we have but the barest and most nebulous clues as to what these cash flows will turn out to be… But woe betide those who think that a near term price to earnings ratio defines value in an era of deep change.”

— James Anderson

The quality of the entry barriers and the life-cycle of the entry barriers are subject to enormous change, sometimes over short periods emanating from circumstances and industries over which the investor may not have sufficient awareness or knowledge. The speed of change and disruption possibilities have never been greater in many industries. Assessing how strong entry barriers are has become the biggest challenge for investors. This trend has potentially important implications for investors in areas such as valuation, portfolio turnover, and diversification.

“Portfolio theory built on assumed normal distributions is a beautiful edifice, but in the real financial world, tails are much fatter than normality would predict. And when future prices depend on the choices of millions of human beings and on the way those humans respond to current prices and recent price movements, we are no longer in the land of martingales protected from contagions of irrationality. Herd behavior, with occasional stampedes, outperforms Brownian motion in explaining important price movements.”

— Richard Zeckhauser

Part of what Zeckhauser is talking about is the impact of positive and negative Black Swans and why they come into existence. People like Benoit Mandelbrot were pioneers in understanding and increasing awareness of this phenomenon. The Brownian motion concept borrowed by economics from physics increasingly does not map to the real world. Changes in the structure of the world created by technology and networks mean that assuming that outcomes will be normally distributed is increasingly problematic (at least) and potentially dangerous (at worst). In short, there are more Black Swans than ever and fewer bell curves. More and more important investing and other outcomes are moving into UUU domains.

The Industry is Not Destiny

Michael Mauboussin emphasizes, that even the best industries include companies that destroy value and the worst industries have companies that create value. That some companies buck the economics of their industry provides insight into the potential sources of economic performance. Finding a company in an industry with high returns or avoiding a company in an industry with low returns is not enough. Finding a good business capable of sustaining high performance requires a thorough understanding of the conditions for the industry and the firm. Hence, arrives the need for Firm-Specific Analysis.

If you have a competitive advantage, then, your profitability will be sustainably higher than the industry average. You will be able to command a higher relative price or to operate at a lower relative cost, or both. Conversely, if a company is less profitable than its rivals, by definition it has lower relative prices or higher relative costs, or both. This basic economic relationship between relative price and relative cost is the starting point for understanding how companies create competitive advantage.

Bruce Greenwald in his book Competition Demystified says there are only three kinds of genuine competitive advantage:

Supply: These are strictly cost advantages that allow a company to produce and deliver its products or services more cheaply than its competitors. Sometimes the lower costs stem from privileged access to crucial inputs, like aluminum ore or easily recoverable oil deposits. More frequently, cost advantages are due to proprietary technology that is protected by patents or by experience—know-how—or some combination of both.

Demand: Some companies have access to market demand that their competitors cannot match. This access is not simply a matter of product differentiation or branding, since competitors may be equally able to differentiate or brand their products. These demand advantages arise because of customer captivity that is based on habit, on the costs of switching, or on the difficulties and expenses of searching for a substitute provider.

Economies of Scale: If costs per unit decline as volume increases, because fixed costs make up a large share of total costs, then even with the same basic technology, an incumbent firm operating at a large scale will enjoy lower costs than its competitors.

Core to understanding sustainable value creation is a clear understanding of how a company creates shareholder value. A company’s ability to create value is a function of the strategies it pursues, its interaction with competitors, and how it deals with non-competitors.

Much of what companies discuss as the strategy is no a strategy at all. As Michael Porter emphasizes, the strategy is different from aspirations, more than a particular action and distinct from vision or values. To recap, competitive advantage means you have created value for customers and you can capture value for yourself because the positioning you have chosen in your industry effectively shelters you from the profit-eroding impact of Porter’s Five Forces - Developed by Michael Porter in 1979, Porter’s Five Forces is a framework to look at competitive forces in an industry. The five undeniable forces are: 1) threat of new entrants, 2) threat of substitutes, 3) bargaining power of customers, 4) bargaining power of suppliers, and 5) competitive rivalry.

The Art of War teaches us to rely not on the likelihood of the enemy not coming, but on our readiness to receive him—and have a leadership team with (to quote Marc Andreessen), “imperial, will-to-power people who want to crush their competition.”

Further, Porter differentiates between operational effectiveness and strategic positioning. Operational effectiveness describes how well a company does the same activity as others. Strategic positioning focuses on how a company’s activities differ from those of its competitors. And where there are differences, there are trade-offs. The strategy is what creates a Competitive Advantage. Strategy is about knowing when to say no so that when you say yes, you can go all in. Just like in war, the victorious strategist only seeks battle after the victory has been won.

Sun Tzu says strategy without tactics is the slowest route to victory. Tactics without strategy are the noise before defeat. Having the mental orientation to think over long-term is one the most lethal assets one could have; strategists will always prevail over tacticians. The long term is, by definition, an aggregation of short terms. In a complex adaptive system, companies should develop long-term decision rules that are flexible enough to allow managers to make the right decisions in the short term. In this way, the company is managing for the long run even when it has no information about what the future holds. Success for humans in business is not about crunching numbers; it’s about developing strategies to achieve a long-term goal.

Firm-Specific Analysis

We must understand the fundamental framework for value creation before we consider the various ways a company can add value. Adam Brandenburger and Harborne Stuart, professors of strategy, offer a very concrete and sound definition of how a firm adds value. Their equation is simple:

Value Created = Willingness-to-Pay – Opportunity Cost The equation says that the value a company creates is the difference between what it gets for its product or service and what it costs to produce that product (including the opportunity cost of capital).

Brandenburger and Stuart then go on to define four strategies to create more value: increase the willingness to pay of your customers; reduce the willingness to pay of the customers of your competitors; reduce the opportunity cost of your suppliers; and increase the opportunity cost of suppliers to your competitors. This framework also fits well with Porter’s generic strategies to achieve competitive advantage—cost leadership (production advantage) and differentiation (consumer advantage).

The value net fits comfortably into Michael Porter’s traditional analyses but adds an important element: strategy is not only about risk and downside but also about opportunity and upside.

Understanding sustainable value creation is of first importance for both business operators and investors. Michael Mauboussin asks us to think of sustainable value creation in two dimensions—how much economic profit a company earns and how long it can earn excess returns. Business quality is about defensibility—defensibility comes from moats. The test of whether a moat exists is quantitative, although the factors that creating moats are qualitative. For sustainable value creation, a business must have an economic moat.

The concept of 'Economic Moat' has its roots in the idea of a traditional moat. A moat is a deep, wide trench, usually filled with water, that surrounds the rampart of a castle or fortified place. In many cases, the waters are also infested with sharks and crocodiles to further keep enemies at bay, and the inhabitants safe. Akin to a moat, an Economic Moat protects a company's profits from being attacked by a combination of multiple business forces. Traditional management theory terms such as "Sustainable Competitive Advantage" or "Entry Barriers" essentially connote the idea of an Economic Moat. Companies with "deep, dangerous moats" outperform those without such moats, both in terms of financial performance and stock returns.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage. The products or services that have wide, sustainable moats around them are the ones that deliver rewards to investors.” — Warren Buffett

Here’s Buffett again at the 1995 meeting, where he underlines the importance of the castle’s vitality:

“But we are trying to figure out what is keeping — why is that castle still standing? And what’s going to keep it standing or cause it not to be standing five, 10, 20 years from now. What are the key factors? And how permanent are they?”

Factors Determining an Economic Moat

Economic Moat arises from the weave of Industry Structure and Corporate Strategy. A favorable industry structure can create an Economic Moat. For instance, it is almost impossible for new entrants in the cigarettes business in India, as cigarettes can’t even be advertised. However, where the sector structure is neutral or unfavorable, the only way companies can build an Economic Moat is by having a sharp Corporate Strategy.

The Elements of Porter’s Corporate Strategy Framework are:

Distinctive Value Proposition (to customers)

Customers comprise the heart of any business model. Without (profitable) customers, no company can survive for long. Leaders recognize that they should manage their businesses to maximize the value of the customer base. But too often, earnings pressures result in cost-cutting measures that hurt customers. Loyalty-leading companies operate differently. They create systems for measuring customer value and invest in the necessary enabling technology; they use design thinking methods to build customer loyalty; they organize the business around customer needs; and they engage the organization and stakeholders—employees, board members, investors—in the transformation. And they report on their results in formats that allow investors and other stakeholders to make informed judgments.

The true purpose of a business, Peter Drucker said, is to create and keep customers. Most managers understand this, but few behave as if they do. Under relentless earnings pressure, they often feel cornered, obliged to produce quick profits by compromising product quality, trimming services, imposing onerous fees, and otherwise shortchanging their customers. This short-termism erodes loyalty, reducing the value customers create for the firm.

To better satisfy customers, a company may group them into distinct segments with common needs, common behaviors, or other attributes. A business model may define one or several large or small Customer Segments. An organization must make a conscious decision about which segments to serve and which segments to ignore. Once this decision is made, a business model can be carefully designed around a strong understanding of specific customer needs. Customer groups represent separate segments if:

• Their needs require and justify a distinct offer

• They are reached through different Distribution Channels

• They require different types of relationships

• They have substantially different profitabilities

• They are willing to pay for different aspects of the offer

This emerges from Porter’s belief that companies should not compete to be the best but to be unique. Thus, the first step to achieving this is by offering to meet customer needs differ from that of rivals by choosing the target customer, identifying the needs, and creating a product or service which addresses both. The value proposition is the element of strategy that looks outward at customers, at the demand side of the business. A value proposition reflects choices about the particular kind of value the company will offer, whether those choices have been made consciously or not. Porter defines the value proposition as the answer to three fundamental questions:

1) Which customers are you going to serve?

2) Which needs are you going to meet?

3) What relative price will provide acceptable value for customers and acceptable profitability for the company?

Tailored Value Chain

A Value Chain is the sequence of activities that a company performs to design, produce, sell, deliver, and support its products. In turn, it is part of a company’s larger Value System i.e. all activities and players involved to deliver its value proposition, including suppliers, distribution channel, etc. A tailored value chain makes a company’s value proposition hard to replicate. If you’re trying to describe a strategy, the value proposition is a natural place to begin. It’s intuitive to think of strategy in terms of the mix of benefits aimed at meeting customers’ needs. But the second test of strategy is often overlooked because it is not intuitive at all. A distinctive value proposition, Porter explains, will not translate into a meaningful strategy unless the best set of activities to deliver it is different from the activities performed by rivals. His logic is simple and compelling: If that were not the case, every competitor could meet those same needs, and there would be nothing unique or valuable about the positioning. Insight into customers’ needs is important, but it’s not enough. The essence of strategy and competitive advantage lies in the activities, in choosing to perform activities differently or to perform different activities from those of rivals.

Michael Porter also developed value chain analysis, a powerful tool for identifying a company’s sources of competitive advantage. Porter recommends focusing on discrete activities rather than broad functions such as marketing or logistics, which he considers too abstract. The objective is to assess each activity’s specific contribution to the company’s ability to capture and sustain competitive advantage, be it through higher prices or lower costs.

A distinctive value chain, tailored to the company’s value proposition, serves the strategic purpose of differentiation as written by Porter,

A company can outperform rivals only if it can establish a difference that it can preserve. It must deliver greater value to customers or create comparable value at a lower cost, or do both. The arithmetic of superior profitability then follows: delivering greater value allows a company to charge higher average unit prices; greater efficiency results in lower average unit costs.

Creating an effective value chain analysis involves the following steps:

Create a Map of the Industry’s Value Chain. Show the sequence of activities that most of the companies in the industry perform, paying careful attention to the activities specific to the industry that create value.

Compare your Company to the Industry. Examine your company’s configuration of activities and see how it compares to others in the industry. Look for points of difference that may reflect a competitive advantage or disadvantage. If a company’s value chain closely resembles that of its peers, then the companies are likely engaged in what Porter calls a “competition to be the best.” This is when rivals pursue similar strategies across the same activities, and it often leads to price wars and destructive, zero-sum competition.

Identify the Drivers of Price or Sources of Differentiation. To create superior value, a company should look for existing or potential ways to perform activities differently or to perform different activities. This can come anywhere along the value chain, starting with product design and ending with post-sales service.

Identify the Drivers of Cost. Estimate as closely as possible the full costs associated with each activity. Look for existing or potential differences between the cost structure of the company and that of competitors. Pinpointing the specific drivers of cost advantage or disadvantage can yield crucial insights. This allows a manager to rethink how, or why, a company performs a particular activity.

In 1985, Porter wrote:

“Competitive advantage cannot be understood by looking at a firm as a whole. It stems from the many discrete activities a firm performs in designing, producing, marketing, delivering, and supporting its product."

Breaking a company’s value chain into its discrete components allows you to think about how the whole business fits together - what should the company build, what should it buy, where should it differentiate, where is it OK to use modularized or commoditized inputs, and how is each component linked to the others? Getting the combination right means sustained profits. Certain places in the value chain are incredibly profitable while others are not. Look for these key control points. Controlling the center of something provides greater flexibility and mobility of choices compared to one’s competitor. In chess, if you don’t control the center squares and let your opponent control them, they will have an easier game than if they have to fight for their control. A piece does not have to physically be on a central square to control the center. In business, controlling the center of a value chain can prove mightily profitable.

Competitive advantage is the difference in relative price or relative costs that arises because of differences in the activities being performed. Wherever a company has achieved a competitive advantage, there must be differences in activities. But those differences can take two distinct forms—A company can be better at performing the same configuration of activities, or it can choose a different configuration of activities.

The absence of reasoning in terms of a distinctive value chain in a digital economy could be related to the preference for reasoning in terms of business models—A business model describes the rationale of how an organization creates, delivers, and captures value. But there are problems with the concept. One such problem is the static nature of the common business model’s representation. As it assembles and arranges the puzzle pieces in juxtaposed boxes, the business model canvas lacks a dynamic dimension and as a result, doesn’t do justice to what makes a company thrives. The dominance of the business model as a key structural concept in a digital economy may destroy incentives for strategic thinking: a strategy is designed for the prospective pursuit of Porter’s “right goal”, whereas a business model is discovered in retrospect as the company grows. Porter himself is highly skeptical when it comes to reasoning in terms of business models:

The misguided approach to competition that characterizes business on the Internet has even been embedded in the language used to discuss it. Instead of talking in terms of strategy and competitive advantage, Internet players talk about “business models.” This seemingly innocuous shift in terminology speaks volumes. The definition of a business model is murky at best. Most often, it seems to refer to a loose conception of how a company does business and generates revenue. Yet simply having a business model is an exceedingly low bar to set for building a company. Generating revenue is a far cry from creating economic value, and no business model can be evaluated independently of industry structure. The business model approach to management becomes an invitation for faulty thinking and self-delusion.

“Stacked Architecture”—A concept devised by the Boston Consulting Group’s Philip Evans and Patrick Forth, stresses that in a digital economy marked by the fast pace of technology, business architecture (which sounds like a synonym for value chain) is not a given anymore:

Amazon is now run as four loosely coupled platforms, three of which are profit centers: a community host, supported by an online shop, supported by a logistics system, supported by data services. Unlike many of his rivals, Bezos saw business architecture as a strategic variable, not a given. He did not harness technology to the imperatives of his business model; he adapted his business model to the possibilities — and the imperatives — of technology.

In the hyper-competitive environment, the clearer your business model, the less distinctive your value chain—and the less strategic your positioning. Take Amazon—Amazon is not a retailer. It’s not a conglomerate either. It is a constantly evolving technology company that 1) seals an alliance with its users primarily through an exceptional retail experience(driven by the systematic and regular monitoring of user-generated data), 2) subsidizes this experience’s constant improvement with the net revenue derived from operating a marketplace, and 3) protects its position by being a strong leader on the global cloud computing market as well as by diversifying in markets such as online video streaming. This, taken as a whole, is a strategy more than it is a business model.

Trade-Offs Different from Rivals

This essentially involves deciding on what a company will or will not do, differently from its rivals e.g. budget airlines do not offer free food and beverages onboard, as they are targeting only those customers whose focus is to reach their destination faster (than rail, road, etc), and not food. Trade-offs are a critical milestone on the path to strategic positioning. Trade-offs are the strategic equivalent of a fork in the road. If you take one path, you cannot simultaneously take the other. Whether the fork in the road is about the characteristics of the product itself or the configuration of activities in the value chain, a trade-off means that you can’t have it both ways because the choices are incompatible. Trade-offs are pervasive in competition. They make strategy possible by creating the need for choice.

Trade-offs arise for several reasons. Porter highlights three: First, product features may be incompatible. That is, the product that best meets one set of needs performs poorly in addressing others. Second, there may be trade-offs in activities themselves. In other words, the configuration of activities that best delivers one kind of value cannot equally well deliver another. The third source of trade-offs is inconsistencies in image or reputation. However, trade-offs tend to evolve as technology progresses and techno-economic paradigms shift as a result. Some trade-offs exist in a certain moment and then disappear the next. If the strategy is the art of embracing constraints, it should take into account the fact that the set of constraints evolves as time goes by. For instance, Porter points out that “what were once believed to be real trade-offs—between defects and costs, for example—turned out to be illusions created by poor operational effectiveness.” While certain trade-offs disappear, others rise in importance as the economy becomes more digital. Business executives must learn to understand them to find the right balance in the new techno-economic paradigm.

Fit across the Value Chain

Fit is how well the value chain activities connect to amplify the company’s value proposition and make it even harder to replicate e.g. Domino’s globally is focused on home delivery of pizzas. Accordingly, its outlets are smaller than Pizza Hut which is more designed for dine-in. Even Domino’s pizza is tailored for home delivery so that it does not get soft and soggy during delivery. It’s not enough to have a distinctive value chain. Its various components should also fit tightly together. Another Porter quote here:

Strategy is creating fit among a company’s activities. The success of a strategy depends on doing many things well — not just a few — and integrating among them. If there is no fit among activities, there is no distinctive strategy and little sustainability. Management reverts to the simpler task of overseeing independent functions, and operational effectiveness determines an organization’s relative performance.

A series of choices about a company’s value proposition and its value chain gives rise to competitive advantage. Where those choices involve trade-offs, the strategy becomes more valuable and more difficult to imitate. Michael Porter asks us to think of fit as an amplifier, raising the power of both of those effects. Fit amplifies the competitive advantage of a strategy by lowering costs or raising customer value (and price). Fit also makes a strategy more sustainable by raising barriers to imitation.

Inspired by management consultants who ignore strategy in favor of operational effectiveness and portfolio management, most companies have drawn deep lines between their business units and made those units’ managers accountable for profits and losses.

It’s impossible to tighten the fit among different activities if they are independent, each managed with their own separate P&L. By promoting separate P&L and portfolio management, it appears that generations of management consultants have weakened fit within their clients’ business systems instead of the opposite.

This, by the way, is a lesson that had been learned by Steve Jobs, as explained in a May 2011 article published in Fortune:

Most companies view the P&L as the ultimate proof of a manager’s accountability; Apple turns that dictum on its head by labeling P&L a distraction only the finance chief needs to consider. The result is a command-and-control structure where ideas are shared at the top — if not below. Jobs often contrasts Apple’s approach with its competitors’. Sony, he has said, had too many divisions to create the iPod. Apple instead has functions. “It’s not synergy that makes it work” is how one observer paraphrases Jobs’ explanation of Apple’s approach. “It’s that we’re a unified team.”

It is always difficult to devise the fit that is so critical for the new world of business’s strategic positioning. The reason is the constant temptation to explain a given company’s success through one feature only. As pointed out by Porter, “in competitive companies it can be misleading to explain success by specifying individual strengths, core competencies, or critical resources.”

Tailoring and trade-offs prevent existing rivals from copying a good strategy, either by straddling or repositioning. The more activities rivals have to reconfigure, the more damage they will do to their current positions. Finally, fit explains how competitive advantage can be sustained against new entrants, even the most determined of them. In competing to be the best, imitation is easy, and advantages are temporary. The more a company competes on uniqueness, the less susceptible it is to imitation, and advantages can be sustained over long periods. Great strategies are like complex systems in which all of the parts fit together seamlessly. Each thing you do amplifies the value of the other things you do. That enhances competitive advantage. And it enhances sustainability as well. “Fit”, Porter says, “locks out imitators by creating a chain that is as strong as its strongest link.” Fit implies radical choices as well as painful trade-offs. To achieve fit, one must make extensive use of digital technologies in every part of the company’s value chain. This is not a way to differentiate yourself, as pointed out by Nicholas Carr. Rather, digital technologies are the glue that will make fit easier. So make extensive use of them. Transforming the core business can magnify an incumbent’s strategic advantages over digital newcomers in terms of people, brand, existing customers, and scale. Companies that view tech as a competitive advantage will win over companies that view tech as a “cost”.

Continuity over Time

In business, change is the only constant. Hence, a company’s strategy should enable it to adapt to change and to innovate. Continuity is the enabler. All the other elements of strategy—tailoring, trade-offs, fit—take time to develop. Without continuity, organizations are unlikely to develop a competitive advantage in the first place.

Complacency will kill you. The stronger we are relative to others, the less willing we generally are to change. We see strength as an immediate advantage that we don’t want to compromise. However, it’s not strength that survives, but adaptability. Strength becomes rigidity. Eventually, your competitors will match your strength or find innovative ways to neutralize it. Real success comes from being flexible enough to change, letting go of what worked in the past, and focusing on what you need to thrive in the future. Your competitors are always working to get ahead, and thus you must as well. Your customers’ needs are always changing, and you need to be able to identify and meet these. Considering the actions of your competitors and the desires of your customers are part of the core, daily functions that your business must always perform. To quote Porter again,

The operational agenda is the proper place for constant change, flexibility, and relentless efforts to achieve best practice. In contrast, the strategic agenda is the right place for defining a unique position, making clear trade-offs, and tightening fit. It involves the continual search for ways to reinforce and extend the company’s position. The strategic agenda demands discipline and continuity; its enemies are distraction and compromise.

A strategy isn’t a stir fry; it’s a stew. It takes time for the flavors and textures to develop. Over time, as all of a company’s constituents—internal and external—come to a deeper understanding of what a company can offer them, or what they can offer to it, a whole raft of activities become better tailored to the strategy and better aligned with each other. This aspect of the strategy is very fundamentally about people and their capacity to absorb and process change.

• Continuity reinforces a company’s identity—it builds a company’s brand, its reputation, and its customer relationships. A good strategy, consistently maintained over time through repeated interactions with customers, is what gives power to a brand.

• Continuity helps suppliers, channels, and other outside parties to contribute to a company’s competitive advantage. This is all about alignment and tailoring.

• Continuity fosters improvements in individual activities and fits across activities; it allows an organization to build unique capabilities and skills tailored to its strategy. Continuity increases the odds that people throughout the organization will understand the company’s strategy and how they can contribute to it. The more they “get it,” the more likely they are to make decisions that reinforce and extend the strategy. Managers will be more likely to align activities that had been working at cross-purposes. The point to underscore here is that skill development and alignment rarely happen overnight.

Continuity of strategy does not mean that an organization should standstill. As long as the core value proposition is stable, there can, and should, be enormous innovation in how it’s delivered. A few twists are necessary to upgrade continuity of direction in a more digital economy.

For a long time, the twin disciplines of strategy and management have been founded on the assumption that strategy was distinct from operations. As written by business historian Alfred Chandler,

General management is more than the stewardship of individual functions. Its core is strategy: defining and communicating the company’s unique position, making trade-offs, and forging fit among activities. The leader must provide the discipline to decide which industry changes and customer needs the company will respond to, while avoiding organizational distractions and maintaining the company’s distinctiveness.

That view of strategy as detached from operations has been fiercely attacked from the 1980s onward by the proponents of a rival theory known as “emergence.” Arguing against strategic positioning decided at the top, the emergent strategy school considers that an organization is a community of people that is better able to inspire strategy than management trapped inside what Tom Peters and Robert Waterman, authors of the best-selling book—In Search of Excellence, call the “analytical ivory tower”.

Henry Mintzberg is considered as the father of emergence: “no planning drill, however rich, can capture all the intuitions and nuanced judgments of the experienced manager responding to ever-changing business reality.” Walter Kiechel, III, who extensively wrote about business strategy, helps us understand what’s at stake here:

The emergent school did get one huge point exactly right: You can’t predict the future, no matter how many studies you amass or alternative scenarios you gin up. Critics have used this sad fact to bash the whole idea of strategy. Why should companies go to the trouble if the future isn’t going to turn out the way anyone expected?…

Other thinkers, fascinated by how Linux grew to pose a challenge to the likes of Microsoft, are trying to incorporate network analysis into their calculations. Probably the hottest term in discussions these days is ‘adaptive’ — as in “How can we make sure our strategy continuously, indeed almost automatically, adapts itself to our changing circumstances?”

Continuity of direction (the Porterian way) doesn’t exclude trial-and-error (emergence). Quite the contrary: trial and error in the digital economy create more value under the form of data-documented feedback, with the ivory tower effectively extended throughout the organization and beyond, in constant touch with the company’s ecosystem, and gathering real-time data from every direction.

Amazon’s strategy has been famously fixed from the beginning, whereas Amazon’s business model is constantly evolving through trials and errors as Jeff Bezos and his troops constantly weigh what he calls “type 2 decisions” (‘two-way doors’). “Type 1 decisions” (‘one-way doors’) are a matter of strategy and shouldn’t be taken lightly. “Type 2 decisions” are a question of the business model—and this must evolve constantly to preserve the company’s strategic positioning in the digital economy.

Continuity gives an organization the time it needs to deepen its understanding of the strategy. Sticking with a strategy, in other words, allows a company to more fully understand the value it creates and to become good at it. Strategies never arrive full-blown and fully formed on Day One. Strategies often emerge through a process of discovery that can take years of trial and error as the company tests its positioning and learns how best to deliver it. At the opposite extreme, Porter warns against thinking that an organization can simply stumble its way into a strategy by encouraging unconnected experimentation in all of its units. The strategy is about the whole, not the parts. There must be a stable core, to begin with, or at least a grounded hypothesis about how the company is going to create and capture value. Often, strategies begin with two or three essential choices. Over time, as the strategy becomes clearer, additional choices complement and extend the original ones.

Porter’s key point is this: rarely, if ever, is it possible to figure out everything that will eventually matter at the very start. Change, then, is inevitable, and the capacity to change is critically important. But the continuity of direction makes effective change more likely. There is no denying that dumb luck has played a role in some extraordinary business successes. But, as Porter likes to ask, would you be eager to invest in someone whose “strategy” is to rely on dumb luck? You may not be able to analyze your way to spectacular success—creativity and serendipity play a role. But armed with an understanding of strategy essentials, you are more likely—far more likely—to make better decisions along the way.

Paradoxically, continuity of strategy improves an organization’s ability to adapt to changes and to innovate. The deliberate and explicit setting of strategy is more important than ever during periods of change and uncertainty. Organizations are complex. They require time to become proficient at delivering their chosen kind of value. In what at first sounds like a paradox, Porter argues that the deliberate and explicit setting of strategy is more important than ever during periods of change and uncertainty. But it’s no paradox at all when you stop to think that strategy offers a clear direction, allowing managers to tune out the many distractions around them. A strategy, with its focus on the spread between customer value and cost, guards against the tendency to follow fads blindly.

Sources of Added Value

There are three broad sources of added value: Production Advantages, Consumer Advantages, and External (e.g., government) factors. Note that there is substantial overlap between this analysis and the industry analysis, but here we focus on the firm.

Production Advantages

Firms with production advantages create value by delivering products that have a larger spread between perceived consumer benefit and cost than their competitors, primarily by outperforming them on the cost side. Production advantages are distilled into two parts: Process and Scale Economies.

Here are some issues to consider when determining whether a firm has a Process Advantage:

Indivisibility. Economies of scale are particularly relevant for businesses with high fixed costs. One important determinant of fixed costs is indivisibility in the production process. Indivisibility means that a company cannot scale its production costs below a minimum level even if the output is low.

Complexity. Simple processes are easy to imitate and are unlikely to be a source of advantage. More complex processes, in contrast, require more know-how or coordination capabilities and can be a source of advantage. Companies that pursue complex, challenging goals face fewer qualified competitors than those that chase easier goals. It also takes longer for copycats to catch up, which helps entrench the top dogs.

Rate of Change in Process Cost. For some industries, production costs decline over time as a result of technological advances. For industries with declining process costs, the incumbent has learning curve advantages, while the challenger has the advantage of potentially lower future costs. So the analysis must focus on the trade-off between learning advantages and future cost advantages.

Protection. The introduction of intellectual property rights into society has been a huge accelerator of societal creativity. Such rights include intangible creations of the human intellect. There are many types of them, and some countries recognize them more than others. The most well-known are copyrights, patents, trademarks, and trade secrets. If individuals and corporations get these rights, they can create defensible economic moats against the competition. And as long as ongoing research and development and capital expenditures can be managed, there is tremendous leverage in this model. Research suggests that products with patent protection generate higher economic returns as a group than any single industry. However, very few, if any, economic moats originating from intellectual property seem to be able to stand the test of time. Either they’re expiring or becoming obsolete due to societal progress and creative destruction. But they can last for very long.

Resource Uniqueness. Alcoa’s bauxite contract is a good illustration of access to a unique resource.

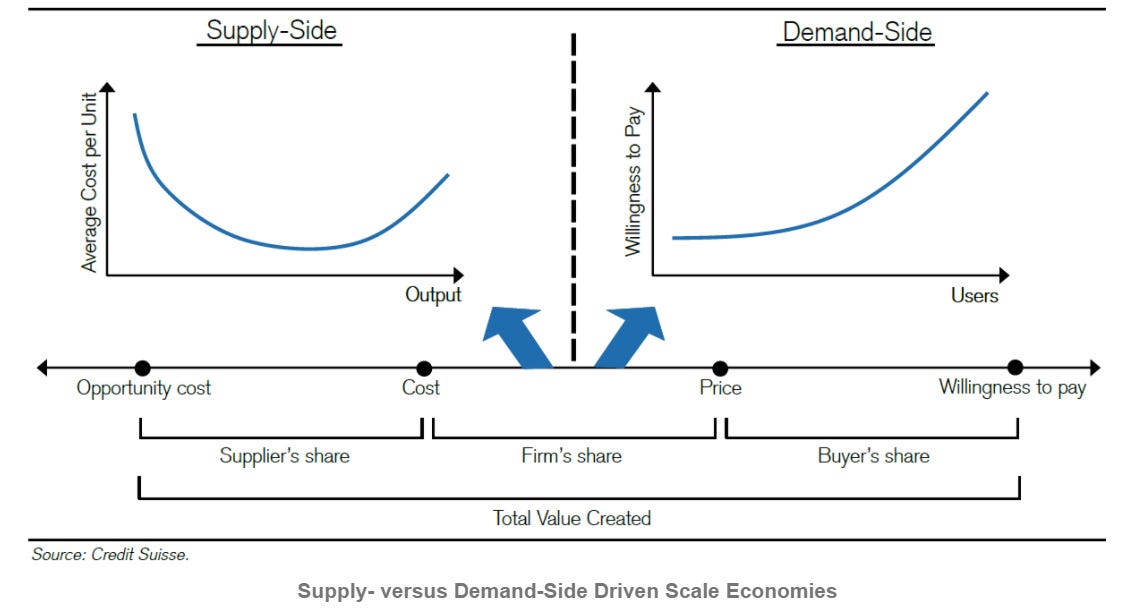

Economies of Scale are the second category of potential production advantage. A firm creates value if it has a positive spread between its sales and costs, including opportunity costs. A firm can create more value by either reducing its costs or increasing the price it receives. Evidence suggests that differences in customer willingness to pay account for more of the profit variability among competitors than disparities in cost levels.

As a manufacturing company increases its output, its marginal and average unit costs decline up to a point. This is classic increasing returns to scale, as the company benefits from positive feedback on the supply side. It is all about lowering costs; the lower the costs of running your business, the higher your profit will be—you don’t need high revenues to make a high profit with a low-cost business—this is one of the reasons why digital businesses are so attractive. However, positive feedback tends to dissipate for manufacturing companies because of bureaucracy, complexity, or input scarcity. This generally happens at a level well before dominance: market shares in the industrial world rarely top 50 percent. Positive feedback on the demand side comes primarily from network effects.

"In terms of which businesses succeed or fail, advantages of scale are ungodly important. The great defect of scale, of course, ... is that the big people don’t always win—is that as you get big, you get the bureaucracy." — Charlie Munger

Dan Rose, an early employee at both Amazon and Facebook, described Jeff Bezos's strategy in the early days of Amazon on this great podcast:

"The huge scaling cost [that Amazon faced] was an asset, not a weakness. And the thing that people got wrong was, as soon as we could leverage that capacity to become cash-flow positive, and not be reliant on markets anymore, it would be off to the races. It what happened it just took 7-8 years to prove out."

Economists distinguish between supply- and demand-side economies of scale. Traditional industrial monopolists enjoyed supply-side scale, in which they leveraged their massive size to squeeze out cost efficiencies. In contrast, the demand-side scale stems from the incremental value consumers derive from greater network effects.

When you get bigger, a host of advantages accrue to you—More users mean more volume, means you can get cheaper prices from suppliers, means lower prices for customers, means higher conversion rates, makes your advertising more effective than your competition, etc. The numbers all move in your favor, and math is hard to compete with.

Scale Economies Shared—a term coined by Nicholas Sleep, describes a business that shares the benefits of scale with its customers; ‘increased revenues begets scale savings begets lower costs begets lower prices begets increased revenues’. These businesses optimize for longevity - not short-term profitability. Persistent low prices attract customers, leading to increased turnover that drives scale benefits which are then returned to the customer in the form of even lower prices; a virtuous feedback loop. As the business grows, the moat gets wider.

There are very few business models where growth begets growth. Scale economics turns size into an asset. Companies that follow this path are at a huge advantage.

Companies across diverse industries, Ford, Costco, Walmart, Southwest Airlines, Aldi, Amazon, and Geico, have all delivered exponential wealth to their shareholders employing this business model.

“The business model that built the Ford empire a hundred years ago is the same that built Sam Walton’s (Wal-Mart) in the 1970s, Herb Kelleher’s (Southwest Airlines) in the 1990s, or Jeff Bezos’s (Amazon.com) today. And it will build empires in the future, too.”

— Nicholas Sleep

When you’re thinking about cost advantages that stem from scale, remember one thing: The absolute size of a company matters much less than its size relative to rivals. To understand scale advantages, it’s important to remember the difference between fixed and variable costs. Very broadly speaking, the higher the level of fixed costs relative to variable costs, the more consolidated an industry tends to be because the benefits of size are greater.

Beyond fixed costs, Scale Economies emerge from other sources as well. To name a few:

Volume/Area Relationships. These occur when production costs are closely tied to the area, while their utility is tied to volume, resulting in lower per-volume costs with increasing scale.

Distribution Network Density. As the density of a distribution network increases to accommodate more customers per area, delivery costs decline as more economical route structures can be accommodated. One useful way to assess distribution strength is to look at the firm’s operations and revenues on a map. Firms likely have some advantages where assets and revenue are clustered.

Learning Economies. If learning leads to a benefit (reduced cost or improved deliverables) and is positively correlated with production levels, then a scale advantage accrues to the leader. Experience in serving the market results in lower transaction costs and, eventually, higher profit.

Purchasing Economies. A larger-scale buyer can often elicit better pricing for inputs. For example, this has helped Wal-Mart.

The Experience Curve—a concept loomed large in the formative years of the Boston Consulting Group and Bain & Company’s strategy practices. The Experience Curve was based on the empirical observation that many company costs seem to follow a downward trajectory that falls within a specified envelope: for each doubling of units produced (what’s meant formally by “experience”), the deflated cost per unit would be between 70% and 85% of what it had previously been before the doubling (referred to as “Slope”).

The experience curve, which is about reducing costs at scale, was under the stakes of a booming Fordist economy. It revealed supply-side economies of scale as the first positive feedback loop that made it convenient for companies to grow bigger. Yet the same experience curve didn’t lead to the domination of every market by one firm only. One reason is that at a certain point, supply-side economies of scale reach a limit: for every single company, there’s a size beyond which unit costs can’t get any lower; quite the contrary, they start to increase again because of longer distribution routes, higher cost of raw materials, or a higher number of employees generating bureaucratic inertia and stronger collective bargaining power. As Carl Shapiro and Hal R. Varian wrote in their landmark and visionary 1998 book Information Rules: A Strategic Guide to the Network Economy,

Despite its supply-side economies of scale, General Motors never grew to take over the entire automobile market. Why was this market, like many industrial markets of the twentieth century, an oligopoly rather than a monopoly? Because traditional economies of scale based on manufacturing have generally been exhausted at scales well below total market dominance, at least in the large U.S. market. In other words, positive feedback based on supply-side economies of scale ran into natural limits, at which point negative feedback took over. These limits often arose out of the difficulties of managing enormous organizations. Owing to the managerial genius of Alfred Sloan, General Motors was able to push back these limits, but even Sloan could not eliminate negative feedback entirely.

Another reason why the experience curve didn’t turn into a decisive competitive advantage has been forcefully pointed out by Michael Porter: even if a firm can continually improve operational effectiveness, “competition based on operational effectiveness alone is mutually destructive, leading to wars of attrition that can be arrested only by limiting competition.” Business strategy according to Michael Porter is the discipline refined to help firms implement what he calls strategic positioning and to escape the war of attrition that careless competitors fell into while pursuing operational effectiveness along the experience curve.

Cost advantages matter most in industries where the price is a big part of the customer’s purchase decision. Thinking about whether a product or service has an easily available substitute will steer you to industries in which cost advantages can create moats. Cheaper processes, better locations, and unique resources can all create cost advantages—but keep a close eye on process-based advantages. What one company can invent, another can copy.

As defined by Porter, “sustainable competitive advantage is about preserving what is distinctive about a company. It means performing different activities from rivals, or performing similar activities in different ways.” In the presence of sustainable competitive advantage, the dividends of improved operational effectiveness, instead of contributing to the war of attrition, can be divided between the consumer (lower price) and the producer (higher margin).

Companies that enjoy economies of scale in their local geographic or product markets should also be aware of the impact of globalization on their industries.

Globalization ties to economies of scale in two important ways—First, companies enjoying economies of scale in their local markets often find it extremely challenging to replicate those advantages in the new product or geographic markets, and second, increasing globalization may undercut the advantages of economies of scale in some industries. This is tied to the idea that an industry leader can more easily maintain dominance in a market of restricted size. In a restricted market, an upstart needs to capture a significant amount of market share to reach economies of scale, a challenge given it must wrestle share from the leader itself. But as the industry undergoes globalization, economies of scale are easier to obtain for new competitors, as they no longer need to capture a significant share of a local market.

If you believe a firm has a production advantage, think carefully about why its costs are lower than those of its competitors. Firms with Production Advantages often have lower gross margins than companies with Consumer Advantages.

Consumer Advantages

Consumer advantage is the second broad source of added value. Firms with consumer advantages create value by delivering products with a spread between perceived consumer benefit and cost that is larger than that of its competitors. They do so primarily by outperforming competitors on the benefit side. If you believe a firm has a consumer advantage, consider why the consumer’s willingness to pay is high and likely to stay high. Consumer advantages generally appear in the form of high gross margins.

Here are some common features of companies with consumer advantages:

Habit and High Horizontal Differentiation

A product is “horizontally differentiated” when some consumers prefer it to compete with other products. This source of advantage is particularly significant if consumers use the product habitually. A product need not be unambiguously better than competing products; it just has to have features that some consumers find attractive. Habit succeeds in holding customers captive when purchases are frequent and virtually automatic. Habit is usually local in the sense that it relates to a single product, not to a company’s portfolio of offerings.

Cigarette smoking is an addiction; buying a particular brand is a habit. Habit leads to customer captivity when frequent purchases of the same brand establish an allegiance that is as difficult to understand as it is to undermine. Cigarette smokers have their brands, though in a pinch they will light up a substitute; such is the pull of the addiction.

Experience Goods

An experience good is a product that consumers can assess only when they’ve tried it. Search goods, in contrast, are products that a consumer can easily assess at the time of purchase. With experience goods, a company can enjoy differentiation based on image, reputation, or credibility. Experience goods are often technologically complex. High search costs are an issue when products or services are complicated, customized, and crucial. Customers are also tied to their existing suppliers when it is costly to locate an acceptable replacement. The more specialized and customized the product or service, the higher the search cost for a replacement.

Switching Costs and Customer Lock-In

Switching costs can be defined as, the value loss expected by a customer that would be incurred from switching to an alternate supplier for additional purchases. Customers must bear costs when they switch from one product to another.

Switching costs are the costs faced by users leaving for a competing network. They include the cost of breaking legal contracts; buying expensive platform-specific durable hardware; learning to use a new system; migrating data from a proprietary format (e.g. ERP systems); rebuilding a positive reputation (e.g. Amazon); rebuilding a subscriber base (e.g. Twitter).