Welcome to Neel’s Newsletter by me, Neel Chhabra. If you aren’t subscribed and are curious about the Craft of Investing and Living Life in a Multidisciplinary way, join this insatiably curious community by subscribing here:

If you think your friends would like to read the newsletter, please share it with them.

This is the first part of the three-part series on Competitive Strategy and Investing Framework.

“If I have seen a little further it is by standing on the Shoulders of Giants,” wrote Isaac Newton. Let’s climb on the shoulders of Giants and hope to see a little further.

In Part I, we will have a helicopter view, before we finally jump down deep in Part II and Part III.

Let’s take off then!

Competitive Strategy and Investing Framework: Value Creation versus Value Capture

Predicting the future is tough and can be wildly off the mark, but being ignorant is dangerous. The only thing we can count on going forward is innovation. Investors need to understand innovation because the value is created through innovation, it’s the shaping mechanism of which companies will win and lose. To capture the value created, an understanding of competitive strategy is essential.

“Creating value is not enough, you also need to capture some of the value you create.”

“A business creates X dollars of value and captures Y% of X. X and Y are independent variables”

Success sows the seeds of competition. That’s why strong businesses aim to be unique, not the best. Trying to outcompete rivals leads to mediocre performance, so companies should avoid competition and seek to create value instead of beating rivals.

As Thiel believed:

“Once you have many people doing something, you have lots of competition and little differentiation. You, generally, never want to be part of a popular trend… So I think trends are often things to avoid. What I prefer over trends is a sense of mission. That you are working on a unique problem that people are not solving elsewhere.”

Peter Thiel:“There are exactly 2 kinds of businesses in this world. Businesses that are perfectly competitive and businesses that are monopolies.”

When you compete to be the best, you imitate. When you compete to be unique, you innovate. In business, multiple winners can thrive and coexist. You don’t have to obliterate your competition. While imitation creates a race to the bottom, innovation promotes healthy competition and economic growth.

Thiel’s book applies René Girard’s ideas ofmimetic theory to business which rests on the assumption that all our cultural behaviors, beginning with the acquisition of language by children are imitative. He sees the world as a theatre of envy, where, like mimes, we imitate other people’s desires. Like Girard himself, he says companies should avoid competition and walk the path of differentiation. He explains that many businesses create a lot of value, but don’t capture a lot of the value they create. As a result, even very big businesses can be unprofitable.

A company, whose desires seek to be like the subject it imitates, through the medium of the object that is possessed by the other company it imitates. Mimetic behavior is deep in our source code. Thiel describes human brains as “gigantic imitation machines.”

“The most mimetic institution of all is a capitalist institution: the stock market”

~ René Girard

René Girard: “Man is the creature who does not know what to desire, and he turns to others to make up his mind. We desire what others desire because we imitate their desires.”

According to Thiel, monopoly is the end state of every successful business. If you want tocreate and capture lasting economic value,don’t compete. The more unique companies are, the more the business ecosystem can flourish.

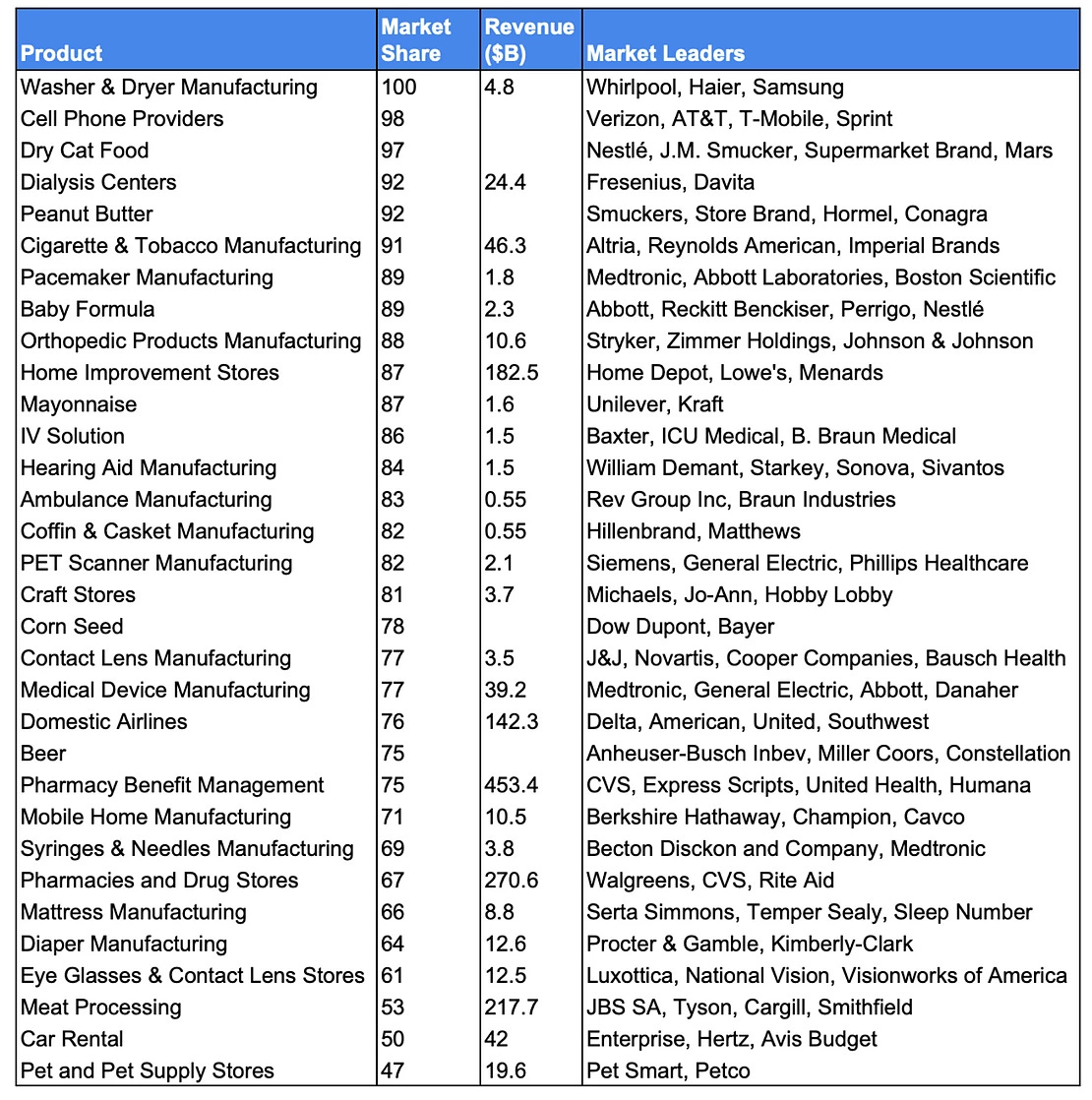

While Big Tech is in Limelight, it turns out that almost all industries are now dominated by monopolies.

Big Tech Monopolies

Almost every industry is now dominated by a few big firms. Consumers generally have a plethora of choices. However, in many cases, every product in a category is made by the same few companies.

The Illusion of Choice

This illusion of choice is across industries. In almost every industry, market share is being concentrated in a small handful of companies.

Concentrated Product Markets

And we are seeing similar phenomena in Indian markets as well. In most sectors, 1-2 companies account for almost 80% of the profits… Paints (Asian Paints, Berger), Small Cars (Maruti Suzuki, Hyundai), Biscuits (Britannia, Parle), Cigarettes (ITC), Adhesives (Pidilite), Cooking Oil (Marico, Adani), Hair Oil (Marico, Bajaj), Baby Milk (Nestle), Glass Lined Reactors (GMM Pfaudler), Aliphatic Amines (Alkyl Amines, Balaji Amines), Telecom (Reliance Jio, Airtel) and more.

In a Darwinian world, the evolution of both demand (i.e. customer behavior, as Rory Sutherland put it, that, the next revolution will be psychological, not technological), as well as the supply of a product or service, can disrupt some monopolies overnight, the way firms like Kodak and Xerox got disrupted.

“Metrics, and especially averages, encourage you to focus on the middle of a market, but innovation happens at the extremes.” - RorySutherland

Winston Churchill: “The empires of the future are the empires of the mind.”

Therefore, a creative monopolist reinvests the monopoly profits to innovate new products, improve existing products, and figure out better ways of meeting the customer’s demand. Hence, progress usually comes from monopolies, and not from perfect competition.

Joseph Schumpeter, an Austrian political economist, identified innovation as the critical dimension of economic change. He argued that economic change revolves around innovation, entrepreneurial activities, and market power. He sought to prove that innovation-originated market power can provide better results than the invisible hand and price competition. He argued that technological innovation often creates temporary monopolies, allowing abnormal profits that would soon be competed away by rivals and imitators. These temporary monopolies were necessary to provide the incentive for firms to develop new products and processes.

Thomas Russo: "Moats to me mean do they have competitors that have equally compelling propositions. To what extent do they invest behind the moat creating bona fide product differentiation and then telling the consumer about it."

The high cash generation of monopolies enables them to innovate, strengthen, and evolve their competitive advantages. However, spotting the existence of such monopolies is not easy. To quote Thiel again from his book ‘Zero to One’ :

“Anyone that has a monopoly will pretend that they’re in incredible competition…. If the monopolists pretend not to have monopolies & the non-monopolists pretend to have monopolies, the apparent difference is very small”.

Competition is for Losers

All happy companies are different: each one earns a monopoly by solving a unique problem. All failed companies are the same: they failed to escape competition – Peter Thiel

Perfect competition is the default state in Economics 101. In a perfectly competitive market, undifferentiated companies sell homogenous and substitutable products. Firms don’t have market power, so their prices are determined by the iron laws of supply and demand.

High profits attract competition. According to economic theory, if outside entrepreneurs hear about profits, they’ll start a new firm and enter the industry. Increased supply will drive prices down, which will decrease total industry profits. If too many firms enter the market, the entire industry will suffer losses. If companies start to lose money, they’ll go out of business until industry prices rise back to sustainable levels. Most importantly, in a world of perfect competition, no company will make an economic profit in the long run.

“Even when ‘price competition’ is supplemented by ‘quality competition and sales effort’, …it is still competition within a rigid pattern of invariant conditions, methods of production and forms of industrial organization…But in capitalist reality as distinguished from its textbook picture, it is not that kind of competition that counts but the competition from the new commodity, the new technology, the new source of supply, the new type of organization… - competition which commands a decisive cost or quality advantage and which strikes not at the margins of the profits and the outputs of existing firms but at their foundations and their very lives.”

— Joseph Schumpeter

Philip Arthur Fisher:“The company that doesn’t pioneer… doesn’t take chances, and merely goes along with the crowd is liable to prove a rather mediocre investment in this highly competitive age.”

Thiel offers an alternative to perfect competition: monopoly. Without competition, they can produce at the quantity and price combination that maximizes their profits. Successful strategies attract imitators, so the best businesses are challenging to copy. Firms in a competitive industry that sell a commodity product cannot turn a profit. But companies who have a monopoly can set their prices since they offer an in-demand product that cannot be replicated. Monopoly firms are big fish in a small pond and strive to become big fish in a large pond by expanding the pond.

“The critical thing about these monopolies is, it’s not enough to have a monopoly for just a moment.” - Peter Thiel

“Valar Morghulis”: all corporations, that do not innovate and adapt, must die.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage. The products and services that have wide, sustainable moats around them are the ones that deliver rewards to investors.”

“Any company whose earnings are growing consistently or more important, are likely to grow consistently has something unique about it. The competition can read these earnings records too, and fat earnings records are an invitation to come in and sample the cream. So a company that has something unique about it has something the competition cannot latch on to right away. Whatever it is that is unique is a glass wall around those profit margins.”- Adam Smith, The Money Game

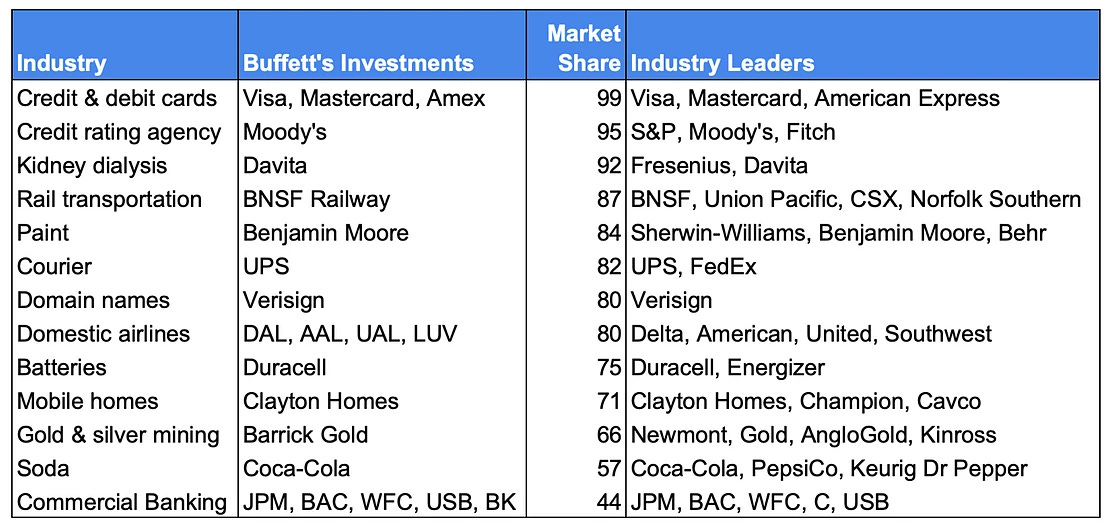

Warren Buffett loves companies with wide moats. And monopoly power confers a very wide moat indeed!

In 2011, Buffett testified before Congress, explaining his reason for investing in Moody’s, Moody’s is one of three credit rating agencies that together control 95% of the market. :

The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price 10 per cent, then you’ve got a terrible business… If you’ve got a good enough business - if you have a monopoly newspaper, if you have a network television station ... your idiot nephew could run it.”

Marc Andreessen: "Raising prices is a great way to flesh out whether you actually do have a moat. If you do have a moat, the customers will still buy, because they have to. The definition of a moat is the ability to charge more."

Charlie Munger talks about some of the investments that he and Buffett have made that passed this test:

There are actually businesses that you will find a few times in a lifetime, where any manager could raise the return enormously just by raising prices — and yet they haven’t done it. So they have huge untapped pricing power that they’re not using. That is the ultimate no-brainer… Disney found that it could raise those prices a lot and the attendance stated right up. So a lot of the great record of Eisner and Wells… came from just raising prices at Disneyland and Disneyworld and through video cassette sales of classic animated movies… At Berkshire, Warren and I raise the prices of See’s Candy a little faster than others might have. And, of course, we invested in Coca-Cola — which had some untapped pricing power.

Rivalry among firms addresses how fiercely companies compete with one another along dimensions such as price, service, new product introductions, promotion, and advertising. In almost all industries, coordination in these areas improves the collective economic profit of the firms. If rivalry is intense, companies compete away the value they create, passing it on to buyers at lower prices or dissipating it at higher costs of competing.

Coordination is difficult if there are lots of competitors. In this case, each firm perceives itself to be a minor player and is more likely to think individualistically. Naturally, the flip side suggests that the existence of fewer firms leads to more opportunities for coordination.

Generally, concentrated industries earn above-average profits and less concentrated industries earn below-average profits.

In addition to Moody’s, Buffett has/had positions in a variety of other extremely concentrated industries. For example, he owns one of two companies that together control 92% of the kidney dialysis market. He also owns Verisign, which handles domain registrations for 80% of all websites (excluding country domains like .us). His investments in Benjamin Moore, Coca-Cola, Duracell, and Clayton Homes, and numerous other investments reflect a similar logic.

Buffett’s Monopoly Companies

The key to this strategy is that it focuses on change and not level. Stocks in concentrated industries trade at higher multiples as the market is smart enough to recognize their monopoly power. Therefore, an investment strategy that simply buys companies in concentrated industries does not outperform. However, the market does seem to be slow to recognize the pricing power conferred by rising industry concentration. And as Mauboussin advocates:

The ability to properly read market expectations and anticipate revisions of these expectations is the springboard for superior returns—long-term returns above an appropriate benchmark. Stock prices express the collective expectations of investors, and changes in these expectations determine your investment success.

“Perhaps the single greatest error in the investment business is a failure to distinguish between the knowledge of a company’s fundamentals and the expectations implied by the market price.”

Michael Mauboussin: “Success in a probabilistic field requires weighing probabilities and outcomes—that is, an expected value mindset.”

As investors, we look for corporate managers that can allocate resources to generate attractive long-term returns on investment and search for stocks of companies that are mispriced relative to expectations for financial results embedded in the shares. As Munger says, what goes on in a market for common stocks—is the pari-mutuel system at the racetrack—And the wise ones bet heavily when the world offers them the opportunity. They bet big when they have the odds. And the rest of the time, they don’t. It’s just that simple.

“Handicappers know that you don’t make money by picking favorites. You make money by spotting mispriced odds and investing accordingly.” – Michael Mauboussin

Understanding sustainable value creation is of first importance for both business operators and investors. Mauboussin asks us to think of sustainable value creation in two dimensions — how much economic profit a company earns and how long it can earn excess returns.

First is the magnitude of returns in excess of the cost of capital that a company does, or will, generate. Magnitude considers not only the return on investment but also how much a company can invest at a rate above the cost of capital. Growth only creates value when a company generates returns on investment that exceed the cost of capital.

Looking at growth in isolation can be misleading and it’s an invitation to failure, always have a clear sense of whether a company is earning appropriate returns, i.e. returns above the cost of capital. For profitability, growth is a double-edged sword. It mostly requires additional investments, and the prospects of earning more than the cost of capital depend on the position of the firm in its industry.

Terry Smith: “A good company is one that regularly makes a high return in cash terms on capital employed and can reinvest at least part of that cash flow to grow its business and compound the value of your investment. Bad companies do not do this. They make inadequate returns on the capital they employ. You may think you should invest in these poor companies as they are going to improve because the management will change, or they will be taken over, or their results will pick up with the economic or business cycle. But each day you wait for such events, these companies destroy a little bit more value. Good companies do the opposite. With good company, time is on your side.”

The second dimension of sustainable value creation is how long a company can earn returns in excess of the cost of capital. This concept is also known as fade rate, competitive advantage period (CAP), value growth duration, and T.

Understanding sustainable value creation is not enough, we must also have a clear understanding of sustainable competitive advantage, meaning, that the company not only generate, or have an ability to generate, returns above the cost of capital but also must earn an economic return that is higher than the average of its competitors.

"If you have a big enough moat, you don’t need as much management. You know, it gets back to Peter Lynch’s remark that he likes to buy a business that’s so good that an idiot can run it because sooner or later one will. He was saying that what he really likes is a business with a terrific moat where nothing can happen to the moat. And there aren’t very many businesses like that." - Warren Buffett

Sustainable value creation as the result solely of managerial skill is rare. Competitive forces and endogenous variance drive returns toward the cost of capital. We have heard from Warren Buffett that:

“When a management with a reputation for brilliance meets a company with a reputation for bad economics, it’s the reputation of the company that remains intact.”

"When an industry’s underlying economics are crumbling, talented management may slow the rate of decline. Eventually, though, eroding fundamentals will overwhelm managerial brilliance. (As a wise friend told me long ago, ‘If you want to get a reputation as a good businessman, be sure to get into a good business.’)"

But, then as Buffet suggests: “You can’t have a good deal with a bad person." So, always be on the lookout for managers that share attributes of “The residents of Singletonville” as put by William Thorndike in his book The Outsiders.

Each of the Outsiders shared a worldview that “gave them citizenship in a tiny intellectual village.” Thorndike writes each understood that:

• capital allocation is the CEO’s most important job;

• value per share is what counts, not overall size or growth;

• independent thinking is essential to long-term success;

• sometimes the best opportunity is holding your own stock; and

• patience is a virtue with acquisitions, as is occasional boldness.

I want to make randomness and optionality defining forces of my life, and capitalize on that to generate superior outcomes. I think we all should. Nassim Taleb describes the objective:

“That which benefits from randomness (increased potential for upside in the presence of fluctuations) is convex. That which is harmed by randomness, concave. Convexity propositions should be embraced – concave ones, avoided like the plague…. ‘optionality’ is what is behind the convexity of research outcomes. An option allows its user to get more upside than downside as he can select among the results what fits him and forget about the rest (he has the option, not the obligation).”

And the thing with good management is that it gives you upside options for free.

Nassim Taleb’s idea of having “Skin in the Game” is a brilliant mental model for finding fanatical “Owner-Operators”. Taleb says, the phrase “Skin in the Game” is often mistaken for one-sided incentives: the promise of a bonus will make someone work harder for you. The central attribute is symmetry: the balancing of incentives and disincentives, people should also be penalized if something for which they are responsible goes wrong and hurts others: he or she who wants a share of the benefits needs to also share some of the risks.

Nassim Taleb: “How much you truly “believe” in something can be manifested only through what you are willing to risk for it.”

Management “must maintain a significant vested interest.” Murray Stahl and Matthew Houk writes,

By virtue of the owner-operator’s significant personal capital being at risk, he or she generally enjoys greater freedom of action and an enhanced ability to focus on building long-term business value (e.g., shareholders’ equity). The owner-operator’s main avenue to personal wealth is derived from the long-term appreciation of common equity shares, not from stock option grants, bonuses or salary increases resulting from meeting short-term financial targets that serve as the incentives for agent-operators.

Compensation structure is fairly essential when analyzing management. If the right structure exists, then a seamless web of deserved trust can be created which lessens problems to what Munger would call Reward and Punishment Super-response Tendency. Munger and Buffett chose to make compensation decisions themselves, whereas they delegate almost all management responsibilities, precisely because of the dangers of misaligned incentives. We must consider not only the direct effects but also the less obvious indirect effects that work through incentives.

Warren Buffet describing how wide a moat must be!

“The most important thing to me is figuring out how big a moat there is around the business. What I love, of course, is a big castle and a big moat with piranhas and crocodiles.” - Warren Buffet

Warren Buffett consistently emphasizes that he wants to buy businesses with prospects for sustainable value creation. He suggests that buying a business is like buying a castle surrounded by a moat and that he wants the moat to be deep and wide to fend off all competition. Economic moats are seldom stable. Because of competition, they are getting a bit wider or narrower every day.

“Frequently, you’ll look at a business having fabulous results. And the question is, “How long can this continue?” Well, there’s only one way to answer that. And that’s to think about why the results are occurring now - and then to figure out what could cause those results to stop occurring.” – Charlie Munger

When you are going to perform an act, remind yourself what kind of things the act may involve. When going to the swimming pool, reflect on what may happen at the pool: some will splash the water, some will push against one another, others will abuse one another, and others will steal. Thusly you have mentally prepared yourself to undertake the act, and you can say to yourself: I now intend to bathe, and am prepared to maintain my will in a virtuous manner, having warned myself of what may occur.

Do this for every act, so that if any hindrance does emerge, you can think: I did not prepare myself only to undertake the act, but also for this hindrance that has occurred, and also to handle this hindrance virtuously & keep my will conformed to nature — and this will be impossible if I become vexed.

When you prepare for the worst, you are in a better place to deal with a disaster if and when it does arise - the Stoic way of inverted thinking. Negative thinking can paradoxically produce positive results by allowing for proactive risk management.

Seneca -“What is quite unlooked for is more crushing in its effect, and unexpectedness adds to the weight of a disaster. The fact that it was unforeseen has never failed to intensify a person’s grief. This is a reason for ensuring that nothing ever takes us by surprise. We should project our thoughts ahead of us at every turn and have in mind every possible eventuality instead of only the usual course of events.”

Albert Ellis rediscovered Stoic’s key insight: Sometimes the best way to navigate an uncertain future is not to focus on the bright side (“best-case scenario”) but rather the somber side (“worst-case scenario”). The ability to manage uncertainty by pondering negative thoughts is not just the key to a more balanced life: it is a sine qua non of successful business, entrepreneurship, and investment. Knowing what you can know and knowing what you can’t are both vital ingredients of deciding well. Good decision-makers are content with the world being an uncertain and unpredictable place. Instead of focusing on being sure, they try to figure out how unsure they are.

Charles Ellis wrote in his book Winning the Loser’s Game— Investing is a game where outcomes in the short term tend to be dominated by luck and high transaction costs. By avoiding mistakes there is a better chance of coming out ahead.

“It is not enough to think problems through forward. You must also think in reverse, much like the rustic who wanted to know where he was going to die so that he’d never go there. Indeed, many problems can’t be solved forward. And that is why the great algebraist Carl Jacobi so often said, ‘Invert, always invert.’ And why the Pythagoreans thought in reverse to prove the square root of two was an irrational number.” - Charlie Munger

So Invert and ask – How could an investor lose money buying cigar butts and how could an investor lose money by buying into a wonderful business?

“The best long-term margin of safety comes not from an investment’s price but from the value of a company’s competitive advantage.” - Thomas Russo

The margin of safety is one of the most important concepts in investing. When you violate this by investing in no margin of safety, investors risk the prospect of the permanent impairment of capital. Always Insist on the margin of safety.

Benjamin Graham: “Confronted with a challenge to distill the secret of sound investment into three words, we venture the motto, MARGIN OF SAFETY.”

Return on capital is defined as theamount of money the business earns on the capital that has been invested in the business. Every investor places a different level of importance on the characteristics they feel are essential, but among all the traits, one of the most common characteristics of quality companies is, a high return on capital.

It's hard for a stock to earn a much better return than the business which underlies it, says Charlie Munger:

"If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return, even if you... buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive-looking price, you'll end up with a fine result."

The higher the return on capital, generally speaking, the better the business. It’s even better when such businesses can re-invest more capital at attractive rates of return. Not many businesses can do this.

The Intrinsic Value Compounding Rate of a business is a function of ROIC and the Reinvestment Rate. It’s the business’s return on capital and the re-investment ratethat drive future earnings, making it the key driver of a stock’s long-term performance.

Intrinsic Value Compounding Rate = ROIC x Reinvestment Rate

Companies having high ROIC can have a moat, but they may not have the opportunities to deploy the capital at the same high rate or preferably at higher rates, known as Legacy Moat. Though there is nothing wrong with such companies, the companies which have opportunities to re-invest the incremental capital at attractive rates, known as Re-Investment Moat are the true compounding machines.

“Size of opportunity is a foundation for continual growth and creating a compounding machine.” - Bharat Shah

I think, in India, returns have not only been about current or emerging moats but to a large extent also on the addressable growth and market opportunities that have been present in industries.

Competitive advantage comes in a variety of ways – cost advantages, network effects, intangibles like brands, regulatory advantages, switching costs, and even things like the culture of a company. But having a competitive advantage is not enough. For huge returns, a large market opportunity is also necessary. Competitive advantage or an economic moat by itself does not lead to wealth creation. Only a growing competitive advantage, deepening and widening the economic moat does.

Companies with deep competitive advantages are less interesting than companies whose advantages are only starting to shape up. Similarly, companies with strong cash flows are less interesting than companies whose cash flows are held back by high-returning reinvestment.

Though, the return on capital is a measure of a superior business, it must be considered in the context of sustainability. Return on capital is a historic measure and so you must form a view as to whether the business is likely to be able to continue to earn those same attractive returns. This requires thinking qualitatively about the business and its competitive position; how is it performing today and how likely is it that it will continue to perform in the future? Always be questioning on the likely changes in business design and the business model, what could be the share not of the market, but the market value a few years down the line, who could be the most important competitors to the company a few years down the road, which business designs could have superior economics and how will value thus migrate away from the company. It means thinking strategically, rather than just quantitatively.

While some industries are better at creating value than others, the industry is not destiny. If an industry is in competitive equilibrium, the death of the business wouldn’t matter to the world: some other undifferentiated competitor will always be ready to take the place. It’s always better to avoid commoditized business unless it has radically improved its low-cost competitive advantage.

Charlie Munger tells a story and shows how tough it is to capture value in commodity businesses (a long excerpt, but worth it.):

For example, when we were in the textile business, which is a terrible commodity business, we were making low-end textiles — which are a real commodity product. And one day, the people came to Warren and said, “They’ve invented a new loom that we think will do twice as much work as our old ones.”

And Warren said, “Gee, I hope this doesn’t work because if it does, I’m going to close the mill.” And he meant it.

What was he thinking? He was thinking, “It’s a lousy business. We’re earning substandard returns and keeping it open just to be nice to the elderly workers. But we’re not going to put huge amounts of new capital into a lousy business.”

And he knew that the huge productivity increases that would come from a better machine introduced into the production of a commodity product would all go to the benefit of the buyers of the textiles. Nothing was going to stick to our ribs as owners.

That’s such an obvious concept — that there are all kinds of wonderful new inventions that give you nothing as owners except the opportunity to spend a lot more money in a business that’s still going to be lousy. The money still won’t come to you. All of the advantages of great improvements are going to flow through to the customers.

Conversely, if you own the only newspaper in Oshkosh and they were to invent more efficient ways of composing the whole newspaper, then when you got rid of the old technology and got new fancy computers and so forth, all of the savings would come right through to the bottom line.

In all cases, the people who sell the machinery — and, by and large, even the internal bureaucrats urging you to buy the equipment — show you projections with the amount you’ll save at current prices with the new technology. However, they don’t do the second step of the analysis which is to determine how much is going stay home and how much is just going to flow through to the customer. I’ve never seen a single projection incorporating that second step in my life. And I see them all the time. Rather, they always read: “This capital outlay will save you so much money that it will pay for itself in three years.”

So you keep buying things that will pay for themselves in three years. And after 20 years of doing it, somehow you’ve earned a return of only about 4% per annum. That’s the textile business.

And it isn’t that the machines weren’t better. It’s just that the savings didn’t go to you. The cost reductions came through all right. But the benefit of the cost reductions didn’t go to the guy who bought the equipment. It’s such a simple idea. It’s so basic. And yet it’s so often forgotten.

Charlie Munger says, without a moat, there will be all kinds of wonderful new inventions that give you nothing as owners except the opportunity to spend a lot more money in a business that’s still going to be lousy. The money still won’t come to you. All of the advantages of great improvements are going to flow through to the customers.

The airline industry, for example, is terrible. Paper and forestry products tend to be weak industries. Communication equipment is a pretty good industry. Within these industries, though, you have winners and losers. As Michael Mauboussin observes,

The central observation is that even the best industries include companies that destroy value and the worst industries have companies that create value. That some companies buck the economics of their industry provides insight into the potential sources of economic performance. Industry is not destiny.

Finding a company in an industry with high returns or avoiding a company in an industry with low returns is not enough. Finding a good business capable of sustaining high performance requires a thorough understanding of the conditions for the industry and the firm.

Mauboussin in his excellent research paper Measuring The Moat suggests getting “A Lay of the Land”. This includes creating an industry map to understand thecompetitive landscape, constructing profit pools to see how the distribution of economic profits has changed over time, measuring industry stability, and classifying the industry to improve alertness to the main issues and opportunities.

Industry Map details all the players that touch an industry. For airlines (Delta, Southwest), this would include aircraft lessors (such as Air Lease), manufacturers (Boeing, Airbus), parts suppliers (General Electric, B/E Aerospace), travel website aggregators (Expedia, TripAdvisor), Airfreight and logistics (UPS, FedEx), Global distribution systems (Sabre, Travelport) and more.

Industry Map is a useful Mental Model for your decision-making toolkit.

Mauboussin’s industry analysis also shows that industry stability is another factor in determining the durability of a moat. He writes,

“Stable industries are more conducive to sustainable value creation. Unstable industries present substantial competitive challenges and opportunities.”

The beverage industry is stable. Trends there unfold slowly over time. Sodas don’t get disintermediated by the Internet. Smartphones, by contrast, constitute a very unstable market. BlackBerry smartphones went from market leader to also-ran story in a few years. Mauboussin’s research indicates you may be better served in industries less susceptible to sweeping changes in the competitive landscape.

Further, we’re always up against the shortening lifespans of companies. All the more reason for finding an enduring moat is cardinal.